What Are the True Costs of Consolidating Debt Into Your Home Loan?

Consolidating credit card and personal debt into your home loan can genuinely reduce your monthly repayments - sometimes by hundreds of dollars -...

In today’s unpredictable property landscape, one question keeps investors awake at night: should you prioritise steady rental income or chase capital growth when markets swing wildly? The answer isn’t as black and white as choosing one over the other. Is cash flow more important than appreciation in volatile markets? For most investors, cash flow becomes your financial lifeline during uncertainty, but it doesn’t replace the wealth-building power of capital growth – they work together as your safety net and growth engine.

In volatile markets, cash flow provides the resilience to weather storms while appreciation builds the equity that transforms your financial future. The key lies in tilting your strategy toward sustainable income without abandoning long-term growth potential, ensuring your portfolio survives short-term turbulence and thrives in the recovery.

When property markets turn choppy, your monthly rental income transforms from a nice-to-have into an absolute necessity. Rita, a 45-year-old professional from Melbourne, learned this lesson during the recent market volatility when her investment property’s value stagnated for 18 months. “Thank goodness the rent kept coming,” she reflects. “Without that $450 weekly income, I would have been forced to sell at the worst possible time.”

Strong cash flow improves your borrowing capacity, reduces financial stress, and most importantly, helps you hold properties through complete market cycles. When banks tighten lending criteria during uncertain times, properties with solid rental yields become your ticket to accessing finance for future purchases.

I’ve stood in those exact shoes, and I’ll never forget the anxiety of 2009, staring at my spreadsheet and wondering if I’d made the biggest mistake of my life. My investment property in Ipswich was stuck in neutral – the market had cooled, buyers weren’t biting, and for nearly two years, open homes meant polite smiles but no offers. The temptation to cash out at a loss was real; it felt smarter to cut my losses than risk a further drop. But what quietly saved me wasn’t a crystal ball – it was the boring predictability of rent coming in every single month. By doubling down on tenant relationships and freshening up the place with cost-effective touch-ups, I managed to keep vacancies low and cash flow steady. It wasn’t glamorous, but that cash flow was my shield during those turbulent years. Fast forward just a few years, and the very property everyone called “dead weight” had appreciated by over $150,000 simply because I could afford to wait. That experience etched in me a permanent lesson: cash flow isn’t just about the extra dollars in your pocket; it’s about having the nerves and the options to stick to your long-term strategy when everyone else is panicking.

Multiple income streams provide even greater protection. Properties near universities might combine student accommodation with short-term holiday letting during breaks. Commercial-residential hybrids offer both retail and residential rental income. This diversification means if one income stream falters, others can compensate.

While cash flow keeps you afloat monthly, capital appreciation creates the equity that changes your family’s trajectory forever. Over the past decade, even moderate Sydney suburbs have delivered $200,000-$400,000 in capital growth – money that funds deposits for additional properties, major renovations, or debt reduction strategies.

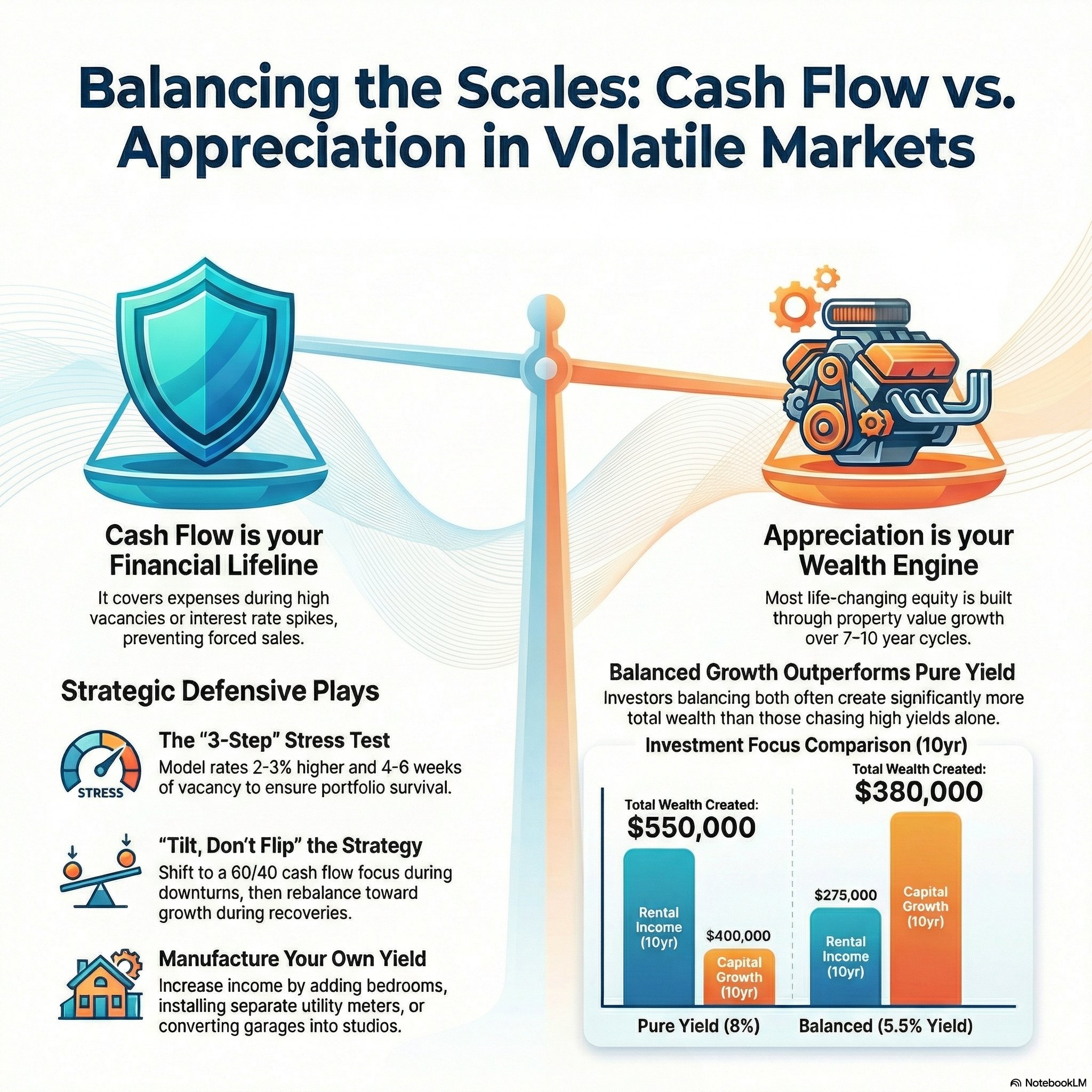

Consider two investors who started with identical $500,000 properties in 2014:

Sarah focused purely on yield (8% rental return): After 10 years, she collected $400,000 in rent but her property appreciated just $150,000 due to its poor location.

Michael balanced cash flow with growth potential (5.5% yield): His property generated $275,000 in rent but gained $380,000 in value, creating $230,000 more wealth overall.

Capital growth doesn’t just happen by accident. It’s driven by infrastructure development, population growth, employment hubs, and supply-demand imbalances. Even during volatile periods, properties in fundamentally strong locations continue building equity, just at varying speeds.

Volatile markets demand a “tilt, don’t flip” approach to your investment strategy. You’re not abandoning growth potential – you’re weighting your portfolio toward resilient income generation while maintaining exposure to appreciation opportunities.

Target properties with manufacturing yield potential:

Focus on vacancy-resistant locations:

Stress test every investment conservatively:

The most successful property investors don’t choose between cash flow and growth – they find assets delivering both. This means identifying properties in genuinely strong locations that also generate reasonable rental yields, even if not the highest available.

Avoid the yield trap where ultra-high rental returns signal weak demand, poor locations, or limited appreciation prospects. A 9% yield in a declining mining town offers less long-term value than a 4.5% yield in a growing suburban hub.

The borrowing capacity strategies that work in volatile markets focus on building portfolios that service themselves while positioning for long-term appreciation.

Understanding where we sit in the property cycle helps determine your cash flow versus growth weighting. During uncertain periods like 2026, when inflation concerns meet economic volatility, defensive positioning makes sense.

Early cycle/Recovery phase: Weight toward cash flow (60/40 split)

Growth phase: Rebalance toward appreciation (40/60 split)

Peak/Decline phase: Return to defensive positioning

Successful volatile-market investing requires a personalised approach based on your financial position, risk tolerance, and investment timeline. The investment property financing strategies that work best combine conservative cash flow projections with realistic growth expectations.

For newer investors: Start with neutral to positive cash flow properties in established rental markets. Build confidence and experience before pursuing higher-risk, higher-reward opportunities.

For experienced portfolios: Use existing equity to acquire defensive cash flow properties that provide income stability while maintaining some growth-oriented assets for wealth building.

For pre-retirement planning: Weight heavily toward cash flow generation (70/30 split) while maintaining enough growth exposure to protect against inflation over time.

Monitor your portfolio’s performance across both metrics quarterly. If rental yields strengthen significantly while growth stalls, consider rebalancing toward appreciation-focused opportunities.

The most sophisticated investors understand that cash flow and capital growth aren’t competing priorities – they’re complementary wealth-building tools that enhance each other’s effectiveness.

Strong rental yields provide the financial stability to hold properties through complete growth cycles. Properties held for 10+ years typically deliver their most substantial capital gains, but only if you can afford to keep them throughout various market conditions.

Meanwhile, capital appreciation creates the equity necessary to acquire additional cash flow generating properties. This compounding effect – where growth enables income, and income enables more growth assets – represents the pathway to true financial independence.

Consider establishing relationships with mortgage brokers who understand this integration approach. The 5 Steps to Financial Freedom framework recognises that sustainable wealth building requires both cash flow management and strategic growth positioning.

Understanding your borrowing capacity for both current and future acquisitions helps optimise this balance. Properties with solid fundamentals often deliver 4-6% rental yields while maintaining strong appreciation potential – the sweet spot for building resilient, growing portfolios.

The key lies in patient, strategic selection rather than rushing into either high-yield or high-growth opportunities without proper due diligence. Quality assets in fundamentally sound locations deliver both income and appreciation over time, just not necessarily simultaneously or in equal measures.

Ready to create a property strategy that thrives regardless of market conditions? Understanding how cash flow and capital growth work together is just the first step toward building lasting wealth through property investment.

Book a mortgage review call today to discover how the right financing structure can position your portfolio for both income stability and long-term appreciation, ensuring you’re prepared for whatever the market brings.

Should I prioritise cash flow over capital gains during a market downturn?

During downturns, weight your strategy 60-70% toward cash flow while maintaining some growth exposure. Strong rental income helps you hold properties until appreciation returns, typically within 3-7 years of market cycles. This balanced approach provides immediate financial stability while positioning you for future capital growth when the market recovers.

What rental yield should I target in volatile markets?

Aim for 4-6% gross yields in capital cities or 6-8% in regional centres, but prioritise vacancy-resistant locations over maximum returns. Properties yielding above 8-9% often signal underlying demand or location issues. Focus on sustainable yields in areas with strong economic fundamentals rather than chasing the highest possible returns, which may come with higher risk.

How do I stress test my property investments for market volatility?

Model interest rates 2-3% above current levels, budget 4-6 weeks annual vacancy, and allocate 1-2% of property value for maintenance. If the investment still cash flows positively, it can likely weather market storms. Create multiple scenarios including worst-case conditions to ensure you can maintain the property even if several negative factors occur simultaneously.

Can I manufacture higher rental yields without compromising growth potential?

Yes, through strategic improvements like adding bedrooms, installing separate metering, enhancing amenities, or creating multiple income streams. Focus on changes that increase both rental return and property value. Consider cosmetic renovations, functional improvements, and configuration changes that appeal to your target tenant demographic while also enhancing the property’s market value.

When should I rebalance from cash flow focus back to growth opportunities?

Monitor market sentiment, vacancy rates, and price growth indicators. When rental demand stabilises and early price recovery signals emerge, gradually increase your growth allocation while maintaining defensive positions. Look for sustained improvements in market fundamentals rather than reacting to short-term fluctuations, and adjust your strategy incrementally rather than making dramatic portfolio shifts.

Consolidating credit card and personal debt into your home loan can genuinely reduce your monthly repayments - sometimes by hundreds of dollars -...

Government schemes like the First Home Guarantee and the First Home Owner Grant are genuinely game-changing for eligible buyers. But here is the...