How to Reduce Risk During Market Volatility

Market volatility is inevitable in property investing, but it doesn't have to derail your wealth-building plans. Most successful...

Market volatility is inevitable in property investing, but it doesn’t have to derail your wealth-building plans. Most successful property investors reduce risk during market volatility by building financial buffers, avoiding over-gearing, and maintaining a strategic long-term perspective. However, the specific approach depends on your financial position, investment goals, and risk tolerance. When implemented correctly, these strategies can turn volatile periods into opportunities for smart investors to accelerate their wealth creation.

Rita had been dreaming about property investment for years. At 45, with her mortgage nearly paid off and her kids finally independent, she felt ready to secure her family’s financial future. But when the market started showing major signs of volatility – including interest rate speculation, economic uncertainty, and conflicting expert commentary in the news – she hesitated.

Like many aspiring investors, Rita’s instinct was to “wait it out.” She thought, “Maybe next year will be better.” This is a classic mistake: letting fear override strategy. Market volatility is not the enemy. It’s a natural part of the investment cycle, and those who are best prepared will benefit in the long run. Successful property investors see volatility as a chance to build wealth by staying disciplined and prepared.

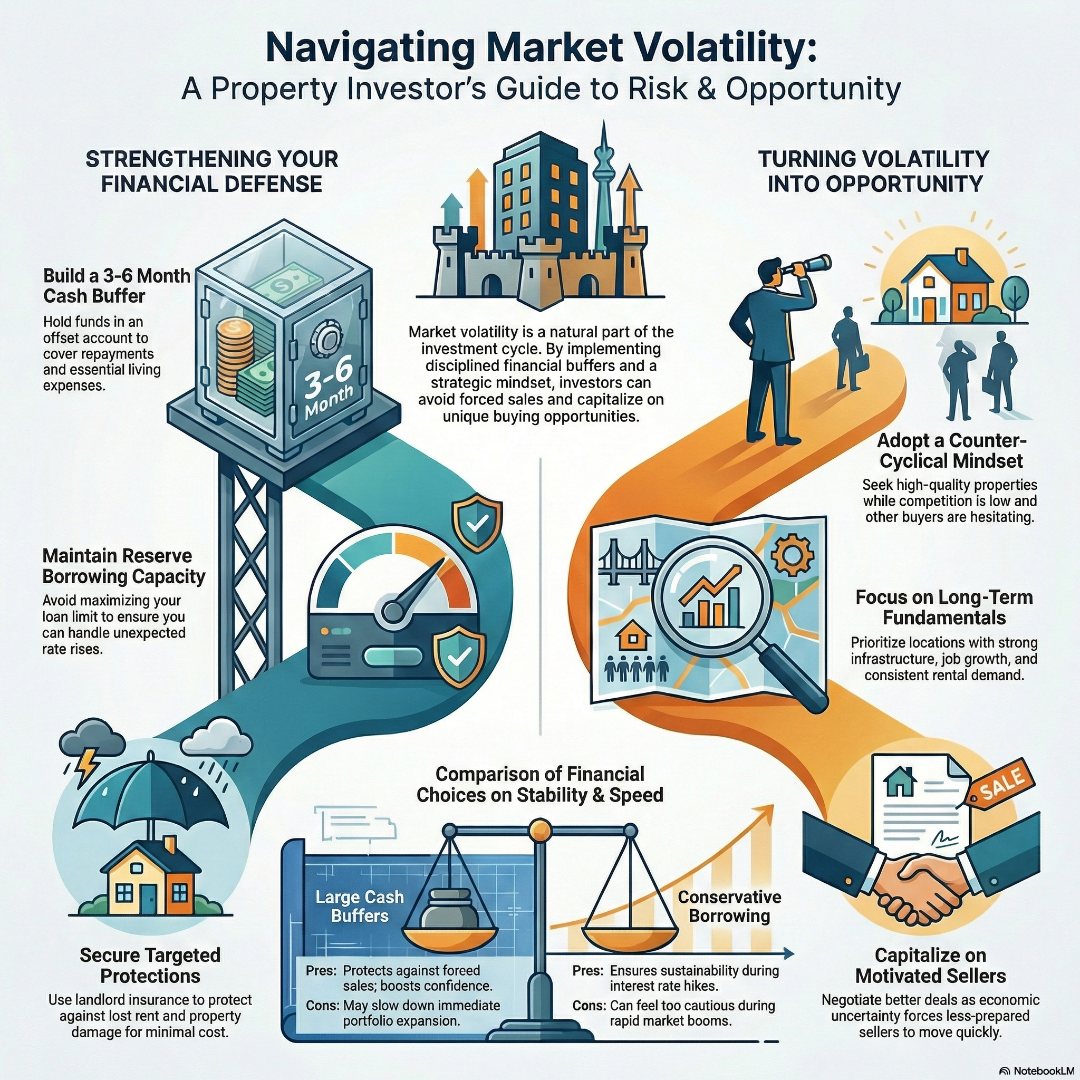

Risk reduction in volatile markets begins with a solid rule: never put yourself in a position where you could be forced to sell at the worst possible time.

Your financial buffer should cover three to six months of loan repayments and essential living expenses. Rather than letting this emergency fund sit idle, smart investors keep it in a mortgage offset account. This reduces interest, keeps funds readily available, and can make all the difference during uncertain times.

Imagine a spike in interest rates or a stretch of vacancy – your buffer allows you to make considered decisions rather than react out of panic. Without one, even minor setbacks could spiral into major financial stress.

Jane Slack-Smith, a twice-awarded Australian Mortgage Broker of the Year, has seen this approach work time and again for clients. Those with buffers stay secure and strong, while those without risk forced sales just when values dip the most.

Many investors think maximising your borrowing power is key. In reality, sustainable investing is about borrowing only what you can comfortably manage – not the maximum you could access.

If your finances are stretched thin, even small disruptions (like a vacancy or rate rise) can quickly cause major problems. Maintaining a reserve capacity between your actual and potential borrowings makes you far more resilient. This might mean buying one property instead of two, but it puts you in a strong position to take advantage of new opportunities, even if the market takes a turn.

It might sound counter-intuitive, but market downturns can be prime times to make bold moves – if you’re prepared. Most people step back during volatility, but those with solid buffers and conservative borrowing can actually ramp up when the opportunities are best.

This counter-cyclical approach is how savvy investors acquire high-quality properties at fair prices while others hesitate.

Every investor faces their own set of risks. Rather than stress about general market conditions, pinpoint what could actually threaten your personal situation and then put protection in place.

Common investor risks and solutions:

This analytical approach to risk isn’t just something I’ve picked up over the years – it’s baked into how I think. Before entering the finance world, I was a mining engineer. I actually insisted on doing my university thesis on safety and risk assessment in mining, despite being told it wasn’t the “usual” path. That experience taught me to weigh up the likelihood and the consequence of every potential hazard. I’ve brought that same rigour to property investing. Whether it’s selecting the right landlord insurance or calculating a precise cash buffer, I treat my portfolio with the same discipline I used in the mines. It’s about looking at what could go wrong and having a plan to neutralise it before it happens.

The bottom line? Be specific about your risks and proactive with your planning.

During periods of volatility, your mindset sets you apart. Media outlets thrive on uncertainty and negative headlines. Successful investors cut through the noise, focus on the facts, and see volatility as uncovering bargains that weren’t previously available.

Products that seemed overpriced months ago may now be fairly valued. Motivated sellers become more flexible. Less competition means serious buyers can negotiate better deals.

This approach isn’t about ignoring risks – it’s about being ready to act rationally, armed with the right buffers and strategies.

Perfectly timing the market is nearly impossible, but understanding broader cycles and positioning yourself is a genuine advantage in uncertain conditions.

When the market is volatile, stick to these fundamentals:

Surprisingly, periods of heightened volatility can fast-track your wealth creation, provided you’re positioned smartly.

Success in property investment is less about picking perfect timing and more about how you prepare for and respond to uncertainty. Don’t wait for flawless conditions – take control of what you can.

Start with a detailed review of your finances. Are your cash buffers strong enough? Is your gearing comfortable for your risk tolerance? Have you pinpointed and protected your biggest risks?

If you’re well prepared, now might be the right time to consider investing where others are hesitant. History shows many of the best investment gains begin during darker economic times.

Every seasoned investor has weathered ups and downs. Preparation, patience, and a focus on long-term results are your greatest assets.

Whether you’re just starting or wish to fortify your portfolio’s resilience, our team can give personal advice built on decades of property expertise.

Book a mortgage review call today to discuss risk reduction, opportunity spotting, and strategic growth in volatile markets.

How much cash buffer should I keep during volatile property markets?

You should aim for a buffer covering 3-6 months of loan repayments and essential living expenses, held in an offset account. Adjust the buffer based on income stability, property numbers, and your risk comfort.

Is now a good time to start property investing if the market is volatile?

Yes, volatility often creates strong opportunities for strategic investors. Focus on having strong buffers, borrowing conservatively, and selecting properties in appealing locations. Avoiding the market could mean missing valuable investments.

Does landlord insurance truly add value in uncertain markets?

Absolutely. For under $500 a year (and tax deductible), landlord insurance protects against lost rent due to tenant damage – a smart safeguard during unpredictable periods.

What’s a sign that I am over-geared for tough market conditions?

If a moderate vacancy or small interest hike would cause serious financial strain, you might be over-geared. Leaving borrowing capacity unused can help you handle these situations smoothly.

Market volatility is inevitable in property investing, but it doesn't have to derail your wealth-building plans. Most successful...

Economic uncertainty creates a unique paradox: while most investors freeze in fear, educated investors often find their greatest opportunities....