What Hidden Costs Do You Still Pay When Using a Government Scheme?

Government schemes like the First Home Guarantee and the First Home Owner Grant are genuinely game-changing for eligible buyers. But here is the...

Government schemes like the First Home Guarantee and the First Home Owner Grant are genuinely game-changing for eligible buyers. But here is the truth that catches too many first home buyers off guard: the hidden costs of buying a home do not disappear just because a government scheme is helping you through the door. Understanding what those costs are, and planning for them before you commit, is the difference between a smooth settlement and a very stressful one.

Think about what the First Home Guarantee actually does. It allows eligible buyers to purchase with a 5% deposit without paying Lenders Mortgage Insurance, potentially saving between $15,000 and $35,000. That is genuinely significant. The First Home Owner Grant in various states adds a cash injection on top. These benefits are real, and they matter enormously.

But a scheme is a targeted tool. It is designed to solve a specific problem – usually the deposit gap or LMI – not to cover the full cost of acquiring a property. The moment you understand that distinction, you can plan properly.

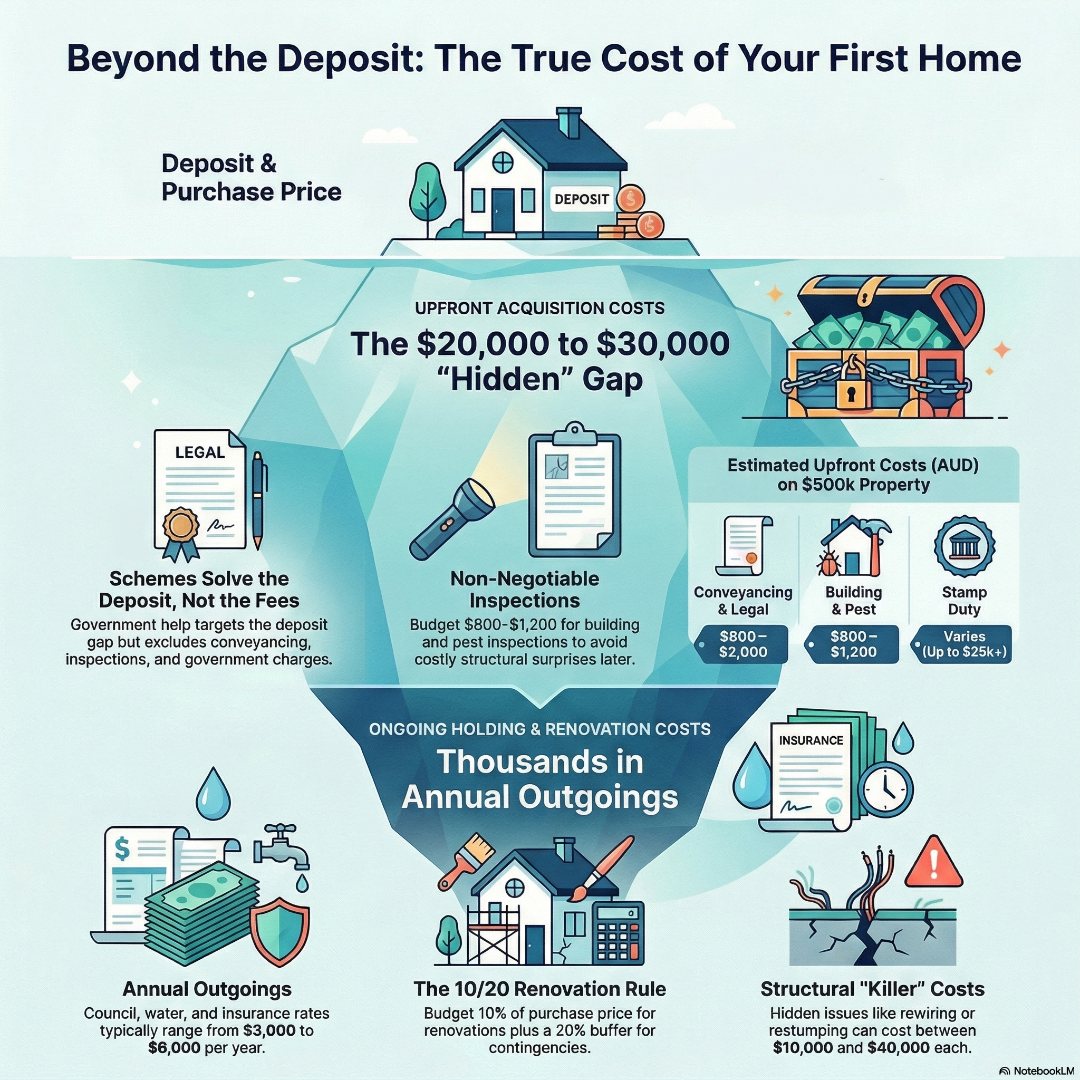

The hidden costs that trip people up are the ones that sit outside the purchase price entirely. They are the fees, charges, and obligations that appear in the weeks before and after settlement. For a lot of first home buyers, they arrive as a complete surprise.

The costs associated with buying a property are not hidden in a deceptive sense. They are listed in contracts, explained by conveyancers, and documented in lender paperwork. But because first home buyers are so focused on the deposit and the loan approval, these costs often get overlooked entirely.

When I bought my first investment property, I had $45,000 to my name – and $25,000 of it went straight to stamp duty on settlement day. I was left with $20,000, a property that needed work, and the very clear realisation that the purchase price was only one number in a much longer equation. There was no government scheme cushioning that blow back then – no First Home Guarantee, no LMI exemption. What saved me was not having extra cash in reserve. It was having done the maths beforehand and knowing exactly where I stood. That experience is the reason I now tell every single first home buyer I work with: get a complete picture of your acquisition costs before you fall in love with a price point. The deposit gets you to the starting line. It is everything else that determines whether you cross it comfortably.

On a $500,000 property, the following acquisition costs could add up to between $20,000 and $30,000:

That is a significant amount of money to find on top of your deposit. None of it is covered by the government scheme you are using.

If you are curious about how property price caps under current schemes affect your purchasing power and which costs may still apply in your state, this breakdown of how property price caps influence your borrowing power is worth reading before you set your budget.

Once the keys are in your hand, a new category of costs begins. These are the ongoing expenses of owning a property, and they do not wait for you to feel financially settled. Many first home buyers focus all their energy on the upfront costs and are genuinely caught off guard when the bills start arriving in the first month.

Add these up across a year and you are looking at several thousand dollars in recurring outgoings that have nothing to do with your mortgage repayment. For a first home buyer already stretching to service a loan, these costs deserve a line in the budget from day one.

Reviewing the 7 common mistakes first home buyers make in Australia is a useful reminder that overlooking holding costs ranks consistently among the most expensive errors buyers make.

A lot of first home buyers choose a property precisely because it needs work. Buy it cheaper, renovate it smarter, build equity faster. It is a legitimate strategy – but only when the renovation budget is realistic.

The general rule is to allow roughly 10% of the purchase price for a renovation. On a $600,000 property, that is $60,000. But here is where buyers get caught badly.

Cosmetic renovations – painting, flooring, new kitchen benchtops, bathroom fixtures – add value and are relatively predictable in cost. The real danger lies in what cannot be seen from a standard inspection.

Structural surprises include:

These are what experienced property professionals call the “killers.” They cost a fortune to fix and typically do not add the same value back to the property. A solid building and pest inspection before purchase is your first line of defence. But even a thorough inspection has limits – invasive structural investigation is not part of a standard report.

If you are buying with renovation intentions, you need a contingency on top of your renovation budget. A minimum 20% buffer over your estimated renovation cost is sensible. If your renovation budget is $50,000, hold $60,000 to $65,000 in reserve.

There is also an often-overlooked carrying cost during a renovation period. You are paying mortgage interest while the property may be uninhabitable or still being worked on. If your renovation takes six months, that is six months of loan repayments with no rental income and potentially no resident. Budget for it explicitly.

The most practical framework for planning around hidden costs is to work backwards from your total available funds rather than forwards from your purchase price ambition. This simple approach removes guesswork and gives you a clear, honest picture of where you stand.

Here is how it works:

If this calculation leaves you with very little room, you have two choices: adjust your purchase price target downward, or delay your purchase until your savings position is stronger. Neither option is a failure. Both are smarter than stretching into a purchase that leaves you financially vulnerable within months of settling.

Understanding your borrowing capacity is a closely related step. Your capacity to borrow and your ability to comfortably service a loan while meeting all your other costs are different numbers. A good borrowing capacity assessment helps you see both clearly.

Most first home buyers approach a mortgage broker when they are ready to apply for a loan. The buyers who have the smoothest experience approach one much earlier – before they have settled on a purchase price, before they have started inspecting properties, and certainly before they have fallen in love with a particular place.

A broker’s role is not simply to find you a loan. It is to map your complete financial picture, identify all the costs you need to account for, and show you exactly where you stand before you commit to anything. That conversation – done early – turns the hidden costs of buying into visible, planned line items in a budget that makes sense.

It also means that when you do use a government scheme, you understand precisely what it covers and what it does not. The scheme gets you through the door. A well-structured financial plan keeps you comfortable once you are inside.

The process of getting your finances set up properly before you buy is one of the most valuable steps a first home buyer can take. Getting your finances set up early is a step that costs nothing and saves thousands.

The hidden costs of buying your first home are not traps – they are simply the full picture that too few buyers see before they commit. Government schemes like the First Home Guarantee are powerful tools that genuinely change what is possible for first home buyers in Australia. But they work best when you enter the process with eyes wide open.

Understanding acquisition costs, planning for holding costs, budgeting realistically for renovation, and working backwards from your actual financial position – these are not complicated steps. They just require the right guidance at the right time.

That is exactly what a mortgage review call is designed to do. Book your mortgage review call today and walk away with a clear, complete picture of what your first home purchase will actually cost – so you can buy with confidence, not regret.

What hidden costs do first home buyers still pay when using the First Home Guarantee?

The First Home Guarantee removes the need to pay Lenders Mortgage Insurance when buying with a 5% deposit, but it does not cover acquisition costs like stamp duty, conveyancing fees, building and pest inspections, loan establishment fees, or council rate adjustments at settlement. On a $500,000 property, these costs can total $20,000 to $30,000. Budget for them separately before you decide on your purchase price.

Does the First Home Owner Grant cover stamp duty and legal fees?

No. The First Home Owner Grant is a cash payment designed to assist with the overall cost of buying or building a first home. It does not specifically cover stamp duty or legal fees. Some states provide separate stamp duty exemptions or concessions for first home buyers, but eligibility depends on the property type and price. Check your state government’s revenue office for current thresholds.

How much should I budget for hidden costs when buying my first home in Australia?

A commonly used guide is to budget an additional 5% of the purchase price to cover all upfront costs beyond your deposit. On a $600,000 property, that is $30,000. If you plan to renovate, add at least 10% of the purchase price as a renovation budget, plus a 20% contingency on top of that figure for unexpected structural issues.

What are the ongoing costs of owning a home that first home buyers often forget?

Ongoing costs that are frequently underestimated include council rates ($1,200 to $2,500 per year), water rates ($700 to $1,200 per year), building and contents insurance ($1,000 to $2,500 per year), general maintenance and repairs ($1,500 to $3,000 per year), and strata fees if applicable. These costs begin from settlement day and need to be factored into your monthly cash flow, not just your upfront budget.

Is it worth using a mortgage broker when applying for a government scheme like the First Home Guarantee?

Yes – and ideally before you start inspecting properties. A mortgage broker can map your total financial position, calculate all costs you need to cover, identify which participating lenders are best suited to your situation, and help you structure a loan that works for the long term. Getting this guidance early means you enter the market with a clear and realistic plan rather than discovering budget shortfalls after you have committed to a purchase.

Government schemes like the First Home Guarantee and the First Home Owner Grant are genuinely game-changing for eligible buyers. But here is the...

Disclaimer: These are generated via AI – please note that you need to do your own due diligence and read the report yourself to make your own...