How Much Mortgage Can I Afford Based on My Salary?

Most people searching this question already have a number in their head. Maybe a friend mentioned what their bank approved them for, or they...

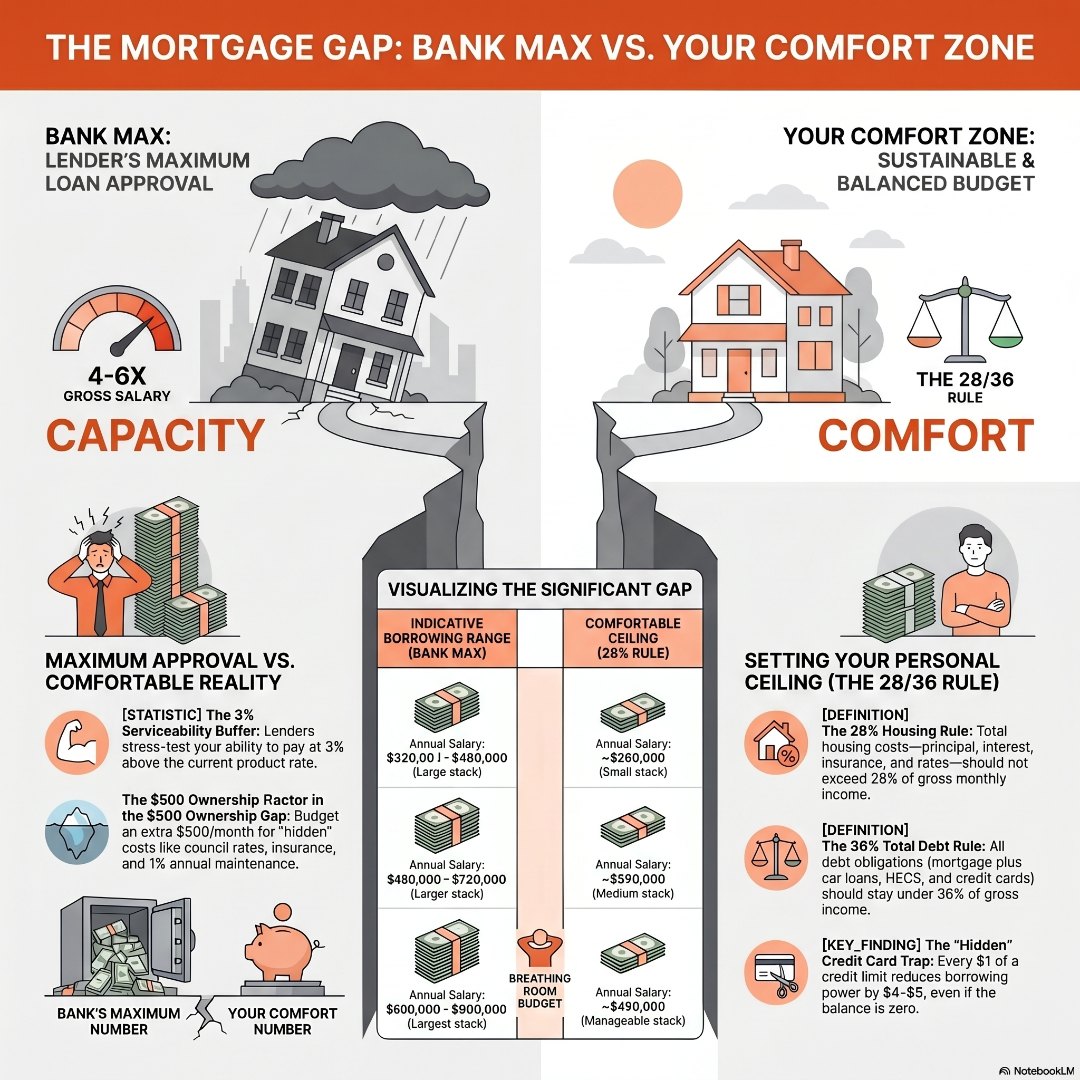

When you submit a home loan application, the first thing a lender does is run a serviceability assessment. This is a calculation to determine whether you can meet repayments comfortably – not just right now, but if rates were to increase. Under current APRA guidelines, Australian lenders must stress-test your loan at a rate approximately 3% above the product rate at the time of application.

In practical terms: if you are offered a loan at 6%, the lender checks whether you could still manage repayments at 9%. That built-in buffer is there to protect both you and the lender from future rate shocks.

Beyond the stress test, lenders assess your gross income, existing debts, number of dependants, living expenses, and employment stability. Two people earning the same salary but carrying very different debt loads will receive very different borrowing limits.

As a rough starting point, most Australian lenders will consider approving between 4 and 6 times your gross annual salary – though this figure has tightened in recent years as living costs and lending criteria evolved. On a $100,000 salary with minimal debts, you might be approved for somewhere between $400,000 and $550,000. On a $150,000 salary, that figure may sit between $600,000 and $800,000. These are indicative ranges only. Your actual approval will depend on the full picture.

The 28/36 rule is a time-tested financial guideline used to help borrowers set a sensible personal borrowing ceiling – independent of what the bank approves.

Here is how it works:

A practical example:

| Annual Salary | Gross Monthly Income | 28% Housing Cap | 36% Total Debt Cap |

| $80,000 | $6,667 | $1,867/mth | $2,400/mth |

| $100,000 | $8,333 | $2,333/mth | $3,000/mth |

| $120,000 | $10,000 | $2,800/mth | $3,600/mth |

| $150,000 | $12,500 | $3,500/mth | $4,500/mth |

To translate that monthly repayment figure into a borrowing amount, a rough guide at a 6% interest rate on a 30-year principal and interest loan: every $1,000 per month in repayment capacity equates to approximately $167,000 in borrowing power.

So if your 28% housing cap lands at $2,333 per month, your comfortable borrowing ceiling is roughly $390,000 – regardless of whether the bank would approve you for more.

Your debt-to-income ratio (DTI) is one of the most influential numbers in your application. Lenders calculate it by dividing your total annual debt obligations by your gross annual income.

As a general guide, most Australian lenders prefer a DTI of 6 or below. APRA has been progressively encouraging lenders to apply more caution to borrowers with a DTI above this threshold.

Here is where many applicants get a nasty surprise: credit card limits are assessed even if you never use them. A $20,000 credit card limit sitting at zero balance is still counted as if you could draw on it in full. For every $1 of credit limit, your borrowing capacity is reduced by approximately $4 to $5. That one unused credit card could be silently costing you $80,000 to $100,000 in borrowing power.

Other common DTI killers include:

Understanding your borrowing capacity strategy before you apply is one of the most valuable steps you can take.

This is the piece that most online calculators skip entirely – and it matters enormously.

Imagine Jess, 29, earning $95,000 a year as a teacher. Her bank pre-approves her for $520,000. The repayments on that loan at 6% would be around $3,118 per month. That is 39% of her gross monthly income – above the 28% housing benchmark and well above her take-home comfort zone once tax, superannuation, and living costs are deducted.

Now factor in what the calculator does not include:

The lender stress-tested Jess at 9% to confirm she could technically service the loan. What they did not test is whether she could still take a holiday, replace her car, cover an emergency, or sleep through the night without financial anxiety.

I have seen this play out in real life more times than I can count. After running a mortgage broking business for over seventeen years, one of the sharpest lessons I have witnessed is how quickly a bank’s number can change – and what happens to buyers who built their entire plan around it. I had clients who held a $700,000 pre-approval, did everything right, took their time finding the right property, and came back a few months later ready to buy. New lending rules had come into effect. Their approval was cut to $400,000 overnight. Not because their income had changed. Not because they had taken on more debt. Simply because the regulatory environment had shifted. That gap – $300,000 – was not a number on a spreadsheet. It was the property they had mentally moved into. The suburb they had chosen for the school. The life they had already started planning. What protected the clients who came through that period in the best shape was not luck. It was that they had structured their borrowing below the maximum from the start, kept a buffer, and had not stretched their life around a figure that turned out to be temporary. That is the conversation worth having before you start shopping – not just what the bank will give you, but what you can confidently carry when the rules shift, the rates move, or life simply does what life does.

This is the trap that leads to being “house poor” – you own the property, but the mortgage consumes so much income that the rest of your life is squeezed. For a deeper look at how rate movements flow through to your actual repayments, our guide on stress-testing your mortgage is worth reading before you commit to any borrowing figure.

| Borrowing at Maximum Approval | Borrowing Within Comfortable Limits | |

| Property access | Broader price range and growth corridors | Narrower range; patience required |

| Rate rise resilience | Little buffer; risk of stress | Built-in buffer; manageable impact |

| Life flexibility | Income changes become crises | Financial decisions made from strength |

| Cash flow | Tight; minimal savings capacity | Room to build a mortgage savings buffer |

| LMI risk | Higher if borrowing above 80% LVR | Reduced or eliminated |

| Peace of mind | Often compromised | Maintained throughout the loan term |

The table below provides indicative borrowing ranges for different income levels in Australia, assuming minimal existing debt, a 20% deposit, and current lending conditions. These are general estimates, not guarantees.

| Annual Salary | Indicative Borrowing Range | Comfortable Ceiling (28% Rule) |

| $60,000 | $240,000 – $360,000 | ~$195,000 |

| $80,000 | $320,000 – $480,000 | ~$260,000 |

| $100,000 | $400,000 – $600,000 | ~$325,000 |

| $120,000 | $480,000 – $720,000 | ~$390,000 |

| $150,000 | $600,000 – $900,000 | ~$490,000 |

| $200,000 | $800,000 – $1,200,000 | ~$650,000 |

Based on 6% interest rate, 30-year P&I loan, minimal existing debt. Individual outcomes will vary.

The gap between the indicative borrowing range and the comfortable ceiling is where most financial stress is born. If you have existing debts or dependants, your comfortable borrowing ceiling will be lower still. This is why a personalised conversation with a mortgage broker – who looks at your complete financial picture, not just your salary – is far more useful than any generic online calculator.

Getting clarity on your true borrowing position before you start house hunting puts you in control and prevents the heartbreak of falling in love with a property you cannot sustainably afford.

Here is a practical pre-application checklist:

The common mistake first home buyers make is going straight to their existing bank. A broker is not just about finding a lower rate. They look at your goals, your timeline, and your complete financial profile to structure a loan that serves you now and into the future. Our article on the 7 most common mistakes first home buyers make goes deeper on this, including why so many buyers get finance sorted far too late in the process.

The bank’s number is the ceiling. Your number – the one that lets you sleep at night, cover the unexpected, and still enjoy your life – is almost always lower. The most important question is not “what will the lender approve?” It is “what can I confidently carry for 30 years while rates move, life happens, and goals change?”

That question deserves a real answer from a real expert who knows your full situation.

Ready to find your genuine number – not just the maximum one? Head to the ICM Hub, where you will find the Mortgage Stress Test tool, borrowing and mortgage calculators, and a full suite of resources to help you borrow with confidence. Explore the tools, run your own scenarios, and when you are ready, book a conversation with the team who can map the complete picture for you.

How much mortgage can I afford based on my salary in Australia?

As a general starting point, most Australian lenders will consider approving 4 to 6 times your gross annual income, depending on your debts, expenses, and deposit size. However, a more useful personal benchmark is the 28% rule: your total housing costs should not exceed 28% of your gross monthly income. On an $80,000 salary, that translates to a comfortable repayment ceiling of around $1,867 per month, or a loan of approximately $260,000 to $310,000 depending on the rate.

What percentage of my income should go to my mortgage repayments?

The widely used guideline is that mortgage repayments should not exceed 28% of your gross monthly income. This is sometimes extended to 30% of pre-tax income as the threshold for mortgage stress. At or above 30%, households begin to feel sustained financial pressure, especially when rates rise or income fluctuates. The safest approach is to stay well below this threshold to maintain a meaningful buffer.

What is the 28/36 rule for a mortgage, and how does it work in Australia?

The 28/36 rule is a personal budgeting guideline where total housing costs sit at or below 28% of gross monthly income, and all debt repayments combined stay at or below 36%. It is not a rule lenders formally apply, but it is a practical tool for setting your own borrowing ceiling. If your debt obligations already consume a significant portion of that 36% figure, your safe mortgage amount is correspondingly lower.

Does my debt-to-income ratio affect how much mortgage I can get approved for?

Yes, significantly. Lenders calculate your total annual debt obligations relative to your gross income, and most prefer a debt-to-income ratio of 6 or below. Existing credit card limits, personal loans, car finance, and HECS/HELP repayments all reduce your assessable borrowing capacity. Reducing credit card limits before applying – even if you carry no balance – can increase your borrowing power by $80,000 to $100,000 in some cases.

Most people searching this question already have a number in their head. Maybe a friend mentioned what their bank approved them for, or they...

Using your home as a bank is not inherently risky - but the risks of using home equity are real, and they are almost entirely determined by how...