How the RBA Impacts Variable Mortgage Rates

Key Takeaways The RBA cash rate directly controls how banks price variable mortgage rates through a three-step transmission process When...

Every month, millions of Australian homeowners hold their breath as the Reserve Bank of Australia (RBA) announces its cash rate decision. But most don’t fully understand the intricate chain reaction that unfolds the moment RBA Governor Michelle Bullock steps up to the podium. The truth is, when the RBA moves the cash rate, your variable mortgage rate doesn’t just mysteriously adjust – there’s a precise, three-step process that determines exactly how much more (or less) you’ll pay on your home loan.

If you’re one of the 60% of Australian borrowers on a variable rate mortgage, understanding how the RBA impacts variable mortgage rates isn’t just academic curiosity – it’s essential financial literacy that could save you thousands of dollars over the life of your loan.

The Reserve Bank of Australia wields enormous influence over the Australian economy through one primary mechanism: the cash rate. This isn’t just any interest rate – it’s the rate that determines how much banks pay to borrow money from each other overnight. Think of it as the foundation upon which all other interest rates in the Australian economy are built.

When the RBA sets the cash rate at, say, 3.60%, they’re not just picking a number out of thin air. They’re establishing the baseline cost of money throughout the entire financial system. This rate becomes the reference point for everything from your home loan to your savings account interest, business loans, and even the rates banks offer on term deposits.

The cash rate serves a dual purpose in monetary policy. When the RBA wants to stimulate economic activity, they lower the cash rate, making money cheaper to borrow and encouraging spending and investment. Conversely, when inflation threatens to spiral out of control, they raise the cash rate to cool down economic activity by making borrowing more expensive.

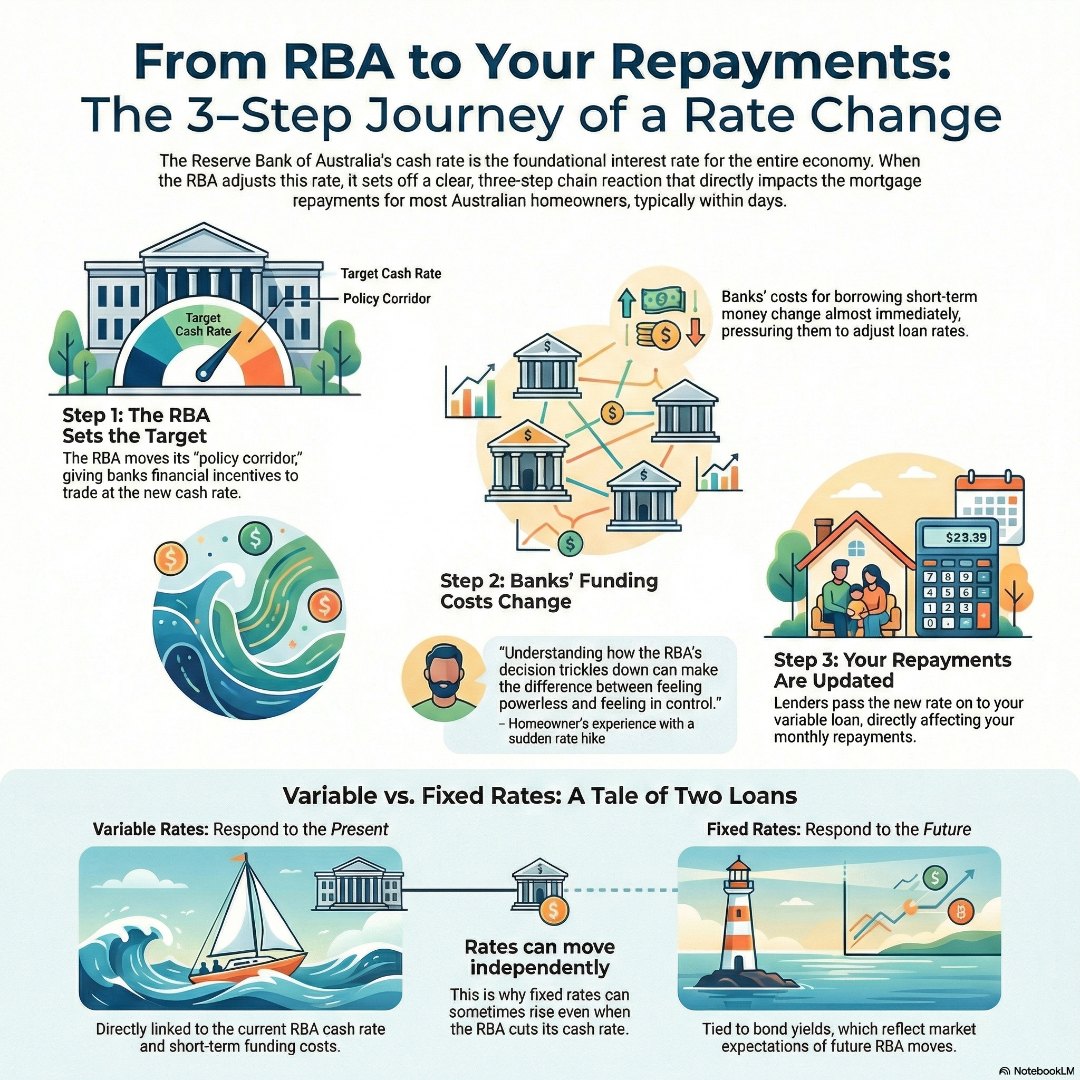

The journey from an RBA announcement to a change in your mortgage repayments follows a predictable three-step transmission process that most borrowers never fully understand.

When the RBA decides to change the cash rate, they don’t just announce a new number and hope banks comply. They actively move what’s called the “policy corridor” – a system that gives banks financial incentives to lend and borrow at the new target rate.

Here’s how it works: The RBA operates a corridor system where they pay banks a deposit rate of cash rate minus 0.10% when banks park money with them overnight, and they lend to banks at cash rate plus 0.25% when banks need emergency funding. This 35 basis point corridor effectively anchors overnight funding costs throughout the banking system.

For example, when the cash rate is 3.60%, the RBA pays banks 3.50% on deposits and charges 3.85% on loans. This corridor ensures that banks have every incentive to trade with each other at rates close to the 3.60% target, rather than paying the premium to borrow from the RBA or accepting the lower rate on deposits.

Once the RBA moves the policy corridor, banks immediately face different costs for their short-term funding. Because variable home loans are typically priced off the cash rate, banks must quickly reprice these loans to maintain their profit margins.

Banks don’t just lend out deposits from savers – they actively borrow money from various sources, including other banks, wholesale markets, and international funding sources. When the cash rate changes, the cost of this short-term funding moves almost immediately. Banks that don’t adjust their variable rates quickly find their margins squeezed if rates rise, or they miss opportunities to remain competitive if rates fall.

This explains why variable rates tend to move in the same direction as the cash rate, and why the changes often occur within days of an RBA decision. Banks are essentially protecting their business model by maintaining consistent spreads between their funding costs and lending rates.

The final step in the transmission process is where borrowers feel the direct impact on their cash flow. When your lender passes on an RBA rate rise in full, your variable rate increases by approximately the same amount. However, the pass-through isn’t always symmetrical.

During rate rise cycles, most lenders pass on increases quickly and in full to protect their margins. But when rates are falling, some lenders are slower to pass on cuts, or they may not pass them on in full. This asymmetric behaviour reflects competitive dynamics, risk management considerations, and each bank’s unique funding mix.

The speed and extent of pass-through can vary significantly between lenders. Some banks pride themselves on quick pass-through of both rises and cuts, using this as a competitive advantage. Others may be more strategic, timing their moves to coincide with marketing campaigns or to differentiate their offerings in the market.

One of the most important distinctions for borrowers to understand is why variable and fixed rates behave so differently in response to RBA movements.

Variable rates are directly linked to the cash rate because they reflect the current cost of short-term funding for banks. When you have a variable rate mortgage, you’re essentially agreeing to pay a margin above the bank’s current funding costs, which fluctuate with the cash rate.

Fixed rates, however, operate in a completely different universe. They’re more closely tied to bond yields and longer-term funding costs, which reflect market expectations about future interest rates rather than current RBA policy. This is why fixed rates can sometimes rise even when the cash rate is falling, or why they might fall ahead of RBA cuts.

Government bonds with terms matching typical fixed rate periods (1-5 years) are the primary drivers of fixed rate pricing. These bond yields incorporate market expectations about future cash rate moves, inflation expectations, and risk premiums for lending over longer periods.

This fundamental difference means that fixed and variable rates can move independently of each other, sometimes in opposite directions. Understanding this relationship helps borrowers make more informed decisions about which rate type suits their circumstances and risk tolerance.

The abstract world of monetary policy becomes very real when it hits your household budget. A 0.25% increase in the cash rate on a $500,000 mortgage translates to approximately $65 more per month in repayments. Over a full year, that’s $780 – money that could have gone toward family holidays, emergency savings, or paying down the principal faster.

But the impact extends beyond the immediate mathematical calculation. Variable rate borrowers experience the psychological stress of uncertainty – never quite knowing when the next rate move might occur or how it will affect their financial position. This uncertainty can influence major life decisions, from whether to upgrade homes to how much to save for children’s education.

I’ll never forget the night the RBA made an unexpected rate hike—my phone pinged with a bank email before I’d even finished dinner. “Effective immediately, your variable mortgage rate has increased.” Instant anxiety hit. My husband and I sat at our kitchen counter, calculators out, trying to work out what that $70 monthly increase meant for groceries, holidays, and the kids’ sports fees. It wasn’t just the number—there was this gnawing uncertainty about what next month might bring. That scramble forced us to look ahead, not just react; we booked a sit-down with a mortgage specialist and built a buffer into our repayments, so the next change didn’t feel like the rug being pulled out from under us. That moment taught me: understanding how the RBA’s decision trickles down can make the difference between feeling powerless, and feeling in control. Every homeowner deserves that clarity—because life is stressful enough without being blindsided by your biggest financial commitment.

The speed at which variable rates adjust means borrowers get immediate feedback on RBA decisions. Unlike fixed rate borrowers who are insulated from short-term moves, variable rate borrowers become acutely aware of economic conditions and monetary policy decisions. This can be both a blessing and a curse – they benefit quickly from rate cuts but also feel the pinch immediately when rates rise.

Smart borrowers use this knowledge to their advantage. They build buffers into their budgets to handle rate rises, and they take advantage of offset accounts and redraw facilities to minimise interest costs when they have spare cash. Understanding the RBA transmission mechanism helps them anticipate changes and plan accordingly.

While media coverage focuses heavily on RBA announcements and headline rate movements, experienced borrowers know that the full picture is far more nuanced. The spread between the cash rate and your actual mortgage rate can vary significantly between lenders and can change over time based on competition, regulatory requirements, and funding conditions.

Some lenders consistently maintain smaller spreads to the cash rate, making them attractive during rising rate environments. Others may offer additional features like offset accounts, redraw facilities, or flexible repayment options that provide value beyond the headline rate.

The track record of how lenders pass on rate cuts versus rate rises is particularly important. Some banks have a history of quickly implementing rate rises but being slower to pass on cuts. Others pride themselves on symmetric pass-through in both directions. This behaviour pattern can significantly impact your long-term borrowing costs.

Product features often matter more than small differences in headline rates. An offset account that reduces your interest calculations daily might save you more money than a slightly lower rate from a lender without this facility. Fee structures, customer service quality, and the lender’s digital capabilities all contribute to the total cost and experience of your mortgage.

Understanding how the RBA impacts variable mortgage rates enables borrowers to make more strategic decisions about their mortgages. Rate cycles are a normal part of economic management, and borrowers who understand these patterns can position themselves advantageously.

During low rate environments, savvy borrowers continue making repayments as if rates were higher, building buffers for future increases while paying down principal faster. This strategy provides both a financial cushion and psychological peace of mind when rates eventually rise.

The timing of rate changes also matters for major financial decisions. Borrowers planning to upgrade homes, refinance, or access equity need to consider not just current rates but likely future movements based on economic conditions and RBA commentary.

Some borrowers choose to split their loans between fixed and variable portions, gaining some protection from rate rises while maintaining flexibility to benefit from cuts. This strategy requires understanding both the RBA transmission mechanism for variable rates and the bond market drivers of fixed rates.

Regular mortgage health checks become particularly important for variable rate borrowers. As your circumstances change and rate cycles evolve, what made sense when you first borrowed may no longer be optimal. The key is staying engaged with your mortgage rather than setting and forgetting.

The relationship between RBA decisions and variable mortgage rates continues to evolve as the financial system adapts to new technologies, regulatory changes, and global economic conditions. Digital banking is accelerating the speed of rate pass-through, with some lenders now updating variable rates within hours of RBA announcements.

Increased competition from non-bank lenders and fintech companies is also influencing how traditional banks respond to RBA moves. These new players often have different funding structures and may pass on rate changes differently than traditional banks.

Regulatory changes requiring banks to hold more capital and comply with stricter lending standards can influence the spreads banks charge above the cash rate. Understanding these broader trends helps borrowers anticipate not just when rates might move, but how the competitive landscape might evolve.

The rise of artificial intelligence and automated lending decisions is also changing how quickly and precisely lenders can adjust their rates in response to RBA moves. This technological evolution may lead to more frequent small adjustments rather than the quarterly or monthly reviews that were common in the past.

Knowledge of how the RBA impacts variable mortgage rates empowers borrowers to take a more active role in managing their mortgage costs. Rather than being passive recipients of rate changes, informed borrowers can anticipate, prepare for, and respond strategically to RBA decisions.

This understanding should inform your choice of lender, loan structure, and ongoing mortgage management. It should also influence how you budget for your mortgage repayments and plan for major financial goals.

The key is viewing your mortgage not as a static obligation but as a dynamic financial tool that requires ongoing attention and optimisation. By understanding the RBA transmission mechanism, you can make more informed decisions about when to refinance, how to structure your loan, and how to manage your broader financial position.

Remember that while variable rates offer the potential to benefit from rate cuts quickly, they also expose you to the risk of rapid increases. Your mortgage strategy should reflect your personal risk tolerance, financial circumstances, and long-term goals.

Ready to take control of your mortgage strategy and ensure you’re getting the best possible deal as RBA rates change? Book a mortgage review call today to discover how our 5 Steps to Financial Freedom framework can help you navigate interest rate cycles with confidence and optimise your mortgage for both current conditions and future rate movements.

How quickly do variable mortgage rates change after an RBA announcement?

Variable mortgage rates typically change within 1-5 business days of an RBA cash rate announcement. Some digital lenders now adjust rates within hours, while traditional banks may take a few days to process the changes through their systems.

Do all banks pass on RBA rate changes by exactly the same amount?

No, banks are not required to pass on rate changes in full or at the same pace. Some may pass on increases faster than decreases, others may absorb small changes, and competitive pressures can lead to different responses between lenders.

Why do fixed rates sometimes move before the RBA changes the cash rate?

Fixed rates are primarily influenced by government bond yields and market expectations about future cash rate moves, not current RBA policy. When markets anticipate RBA changes, bond yields adjust first, causing fixed rates to move ahead of actual cash rate announcements.

Should I switch from variable to fixed rates when the RBA starts raising rates?

This depends on your personal circumstances, risk tolerance, and market expectations. Fixed rates may have already priced in expected RBA rises, so timing is crucial. Consider consulting with a mortgage professional to evaluate your specific situation and explore strategies like loan splitting.

Key Takeaways The RBA cash rate directly controls how banks price variable mortgage rates through a three-step transmission process When...

Key Takeaways Regional properties in Australia typically offer higher rental yields (around 5-7%) compared to metropolitan areas (3-4%),...