Should I Fix My Home Loan Rate After CommBank’s Latest Move?

Key Takeaways CommBank raised fixed home loan rates in January 2026, anticipating potential RBA rate hikes. Banks typically adjust fixed...

Thinking about building your investment property portfolio, but not sure if a fixed or variable rate loan is the smartest move? The answer to that crucial question could shape your future wealth for better or worse. Choosing between fixed and variable rates for investment properties is pivotal for anyone seeking long-term financial security, stable cash flow, and investment success. In this article, we’ll break down everything smart investors need to know (without the jargon), so you can confidently make the right move, sleep well at night, and keep building your plan for an early retirement. If you’re serious about your next step, book a mortgage review call today to ensure your loan is truly working for you.

If you’re aiming for financial freedom, early retirement, or passive income to support your family, the game isn’t just about buying property it’s about buying smart, structuring smart, and managing risk. Many property investors lose thousands (sometimes hundreds of thousands) simply from being in the wrong loan at the wrong time.

Imagine working for 20 years, nearly paying off your family home, and finally feeling ready to build your legacy. The right loan choice on an investment property might mean an extra annual family holiday, earlier retirement, or simply being able to help your kids get started. The wrong loan? It could mean anxiety, cash flow shocks, unwanted fees, or enforced sales at the worst possible time.

The mortgage market is constantly shifting. RBA decisions, APRA interventions, and international factors can quickly upend what seemed like a safe bet just months ago. Having a set-and-forget loan might work for homeowners, but property investors, especially those aiming for a small, high-performing portfolio, need their loan to work for them not against them. That starts with understanding exactly how fixed and variable rates perform for investment purposes.

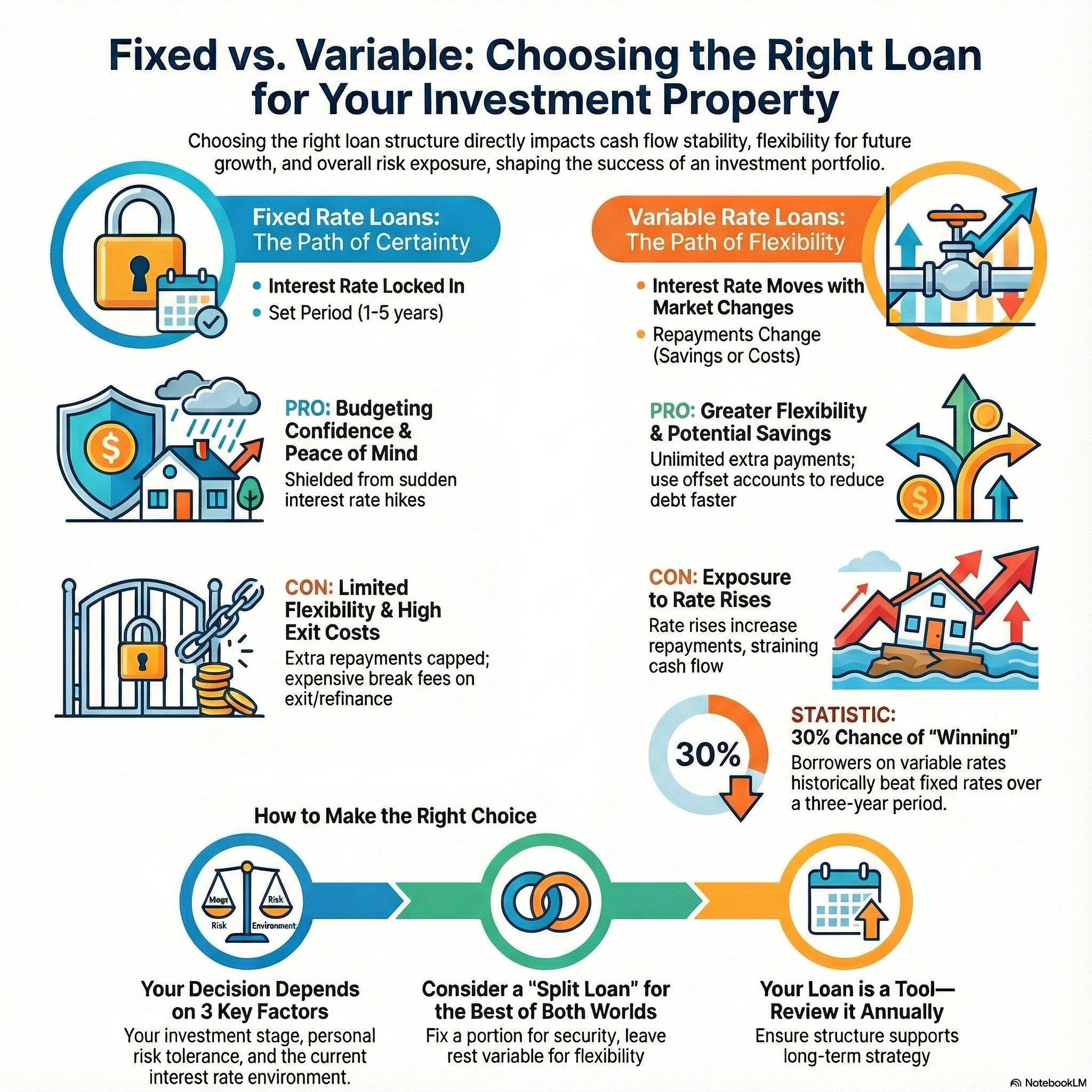

Fixed-rate loans are exactly what they sound like: the interest rate (and therefore your repayments) are “locked in” for a certain period, usually 1-5 years. This delivers rock-solid certainty in your monthly outgoings something many investors love, especially if:

For example, during the rapid recent rate increases, many fixed-rate investors enjoyed a window of “immunity” while their variable-rate peers watched repayments climb. But as the market “reverted,” those investors faced possible higher rates (fixed period ending into a new, higher rate), plus missed out on loan features that could have helped them optimise or renovate.

Variable rates move up and down according to the lender (and RBA) changes sometimes in line with overall economic moves, sometimes not. For property investors, variable loans offer:

When rates rise, so do your repayments sometimes sharply. In the wake of sustained RBA hikes, some investors saw their cash flow evaporate virtually overnight, in turn affecting their lifestyle and portfolio plans.

Statistically, Australian borrowers on variable rates have a three in ten chance (or 30%) of “beating” the fixed rates over any given three-year period. That’s not a guarantee it simply reflects that sometimes the market moves in your favour, and sometimes it doesn’t.

There’s no single answer, and anyone who says otherwise is oversimplifying. Your choice depends on three critical factors:

Most investors especially those working towards a small, high-performing property portfolio for lifestyle and legacy play a blend. It’s common to “split” your mortgage: fixing a portion for security, with the rest variable for flexibility.

Let’s take “Rita,” a 45-year-old nurse with a nearly paid-off home who dreams of a secure, passive income, early retirement, and helping her children into their own homes. After years of being cautious, she finally takes action, but she’s paralysed by the avalanche of mortgage rate debates online.

Rita locks in a 3-year fixed rate “for safety.” Eighteen months later, market rates fall. She wants to renovate one of her investment properties for higher rent (as we teach in the Trid3nt Strategy®), but her loan won’t let her pay extra or redraw without big penalties. Worse, her lender’s break costs make refinancing impossible. Her passive income and flexibility are on hold just because her loan didn’t match her plan.

Her friends, who went variable, paid extra on their mortgages, refinanced into better products, and were able to use their equity for smart renovations they’re moving forward, not treading water.

So how do seasoned investors bypass the fear of getting it “wrong”?

If you haven’t reviewed your loan in the last year, or you’re uncertain if your current structure matches your goals, it may be time for a rethink. The path to financial freedom and early retirement while wanting to leave a legacy for your children starts with clarity and confidence.

Choosing your rate type isn’t just about the headline or even who’s “winning” in a moment of market volatility. It’s about:

Plenty of investors learn the hard way that “saving” on a cheap rate means nothing if you pay thousands to exit early, or miss an opportunity to grow your portfolio through renovation or acquisition.

For many investors, splitting your loan allocating some to fixed, some to variable offers the best of both worlds. You lock in a baseline of certainty, while keeping the agility to seize opportunities or accelerate repayments when possible.

A strategic split is something every investor should at least discuss with their mortgage broker as part of an annual review.

It’s not about chasing trends or copying the latest financial commentator. Your investment property loan should be as unique as your goals, lifestyle, and risk tolerance. The single biggest mistake is inaction getting stuck wondering and missing the compounding growth (and peace of mind) that a properly structured loan can provide.

Book a mortgage review call today with a property investment loan expert who actually understands strategy, long-term planning, and how to fit a loan to your vision.

Is fixing the interest rate on my investment property always better than staying variable?

No, it depends on your goals, cash flow, borrowing strategy, and the economic outlook. Fixing protects against rate rises but limits flexibility. The best option varies based on market conditions and your investment timeline. If you’re building a portfolio quickly, variable rates may offer more flexibility, while fixed rates provide certainty for those focused on stable cash flow.

Can I pay extra on a fixed-rate loan?

Most fixed-rate loans have strict limits on extra repayments, and break fees can apply. Variable loans typically offer greater freedom. Some lenders allow a small amount of extra repayments (often $10,000 per year) on fixed loans, but this varies significantly between financial institutions and specific products.

What if I want certainty but might need to access equity?

Consider a split loan to capture the best of both some fixed for certainty, some variable for flexibility and redraw. This hybrid approach allows you to lock in rates for a portion of your loan while maintaining access to features like offset accounts and redraw facilities on the variable portion, giving you the security of fixed repayments with the flexibility to access funds if needed.

How often should I review my investment property loan structure?

At minimum, review your loan annually or when significant market changes occur. Interest rate movements, changes in your financial situation, or shifts in your investment strategy are all triggers for a loan review. Regular assessment ensures your mortgage continues to align with your evolving investment goals and the current economic environment.

Taking your next step should feel exciting, not stressful. Ensure your home loan is supporting your investment journey and if you’re unsure, don’t wait until rates move again or circumstances change against you. Book a mortgage review call today and let experienced experts help you unlock the next chapter in your financial future.

Key Takeaways CommBank raised fixed home loan rates in January 2026, anticipating potential RBA rate hikes. Banks typically adjust fixed...

Key Takeaways Strategic planning, robust financing, and clear investment goals are crucial for building a profitable investment property...