Should I Fix My Home Loan Rate After CommBank’s Latest Move?

Key Takeaways CommBank raised fixed home loan rates in January 2026, anticipating potential RBA rate hikes. Banks typically adjust fixed...

If you’re considering whether it’s worth refinancing your home loan in Australia, you’re not alone. It’s tempting: lower interest rates, smaller repayments, and access to equity for renovations or investments. But the question nearly every savvy homeowner wants answered is, “How much does it cost to refinance in Australia?”

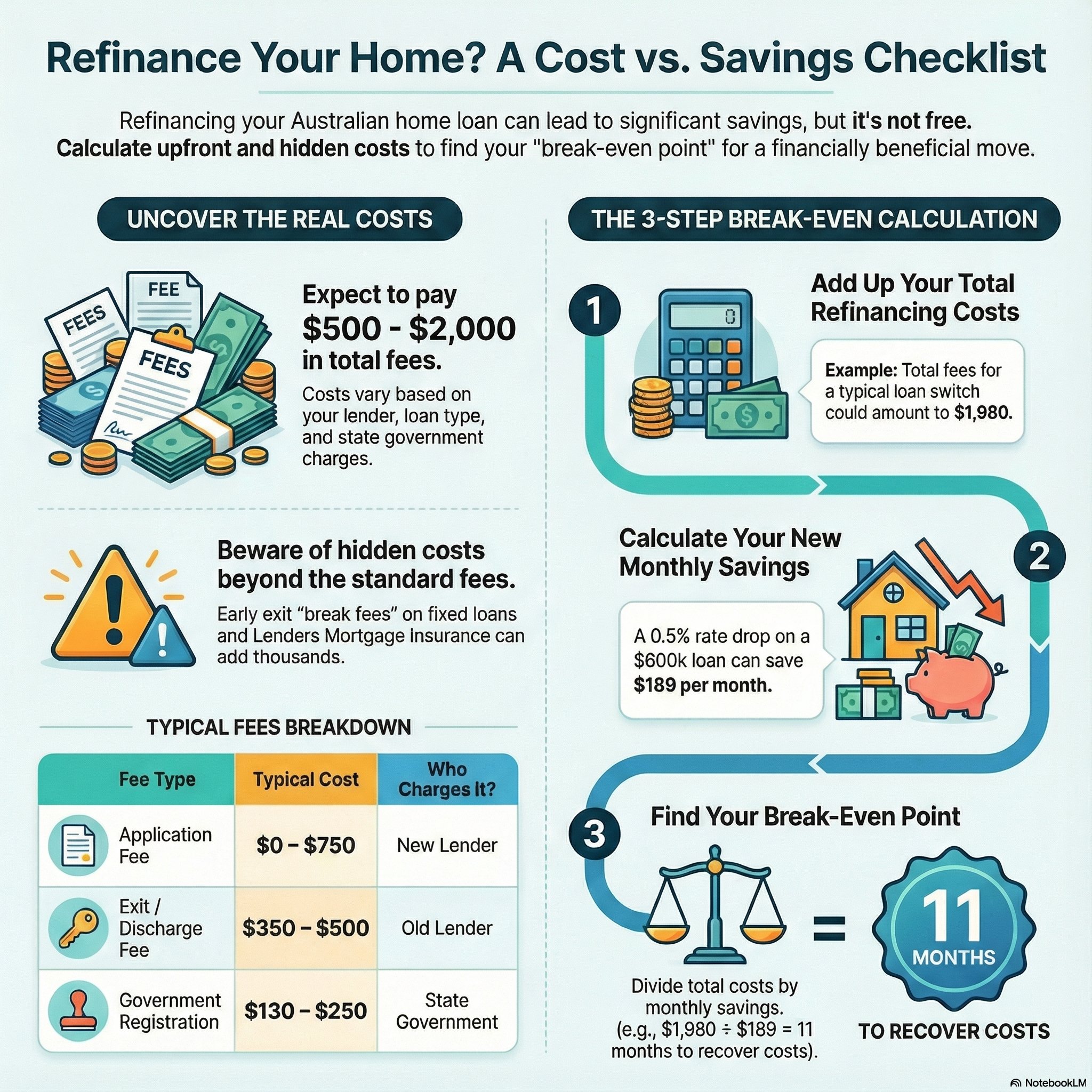

The answer, for most people, is more than you might think—but less than the wrong mortgage for the next few decades. The average cost to refinance a home loan usually falls in the $500–$2,000 range, but what’s really at stake is understanding the blend of both the visible and the hidden costs before you make the decision to switch.

Before you sign a loan offer, there are several upfront costs lenders will clearly outline in their product disclosure statements:

| Cost Type | Typical Range | Who Charges It? | Can It Be Negotiated? |

| Application Fee | $0 – $750 | New lender | Yes, often waived |

| Property Valuation Fee | $50 – $600 | New lender | Sometimes |

| Settlement Fee | $100 – $400 | New lender | Rarely |

| Exit/Discharge Fee | $350 – $500 | Old lender | No |

| Government Registration Fees | $130 – $250 per title | State government | No |

| Title Search Fee | $50 – $100 | Lender/Legal team | No |

| Legal and Admin Fees | $200 – $400+ | Lender/Solicitor | Sometimes |

| Lender’s Mortgage Insurance (LMI) | $2,000+ (if LVR > 80%) | New lender | No |

Source: Money.com.au, Bank Australia, Canstar

Beware the fine print: lenders compete aggressively on rates—less so on transparency about all costs involved.

Let’s address the real concerns holding most people back from refinancing: fear of unexpected costs and uncertainty about whether the savings will be worth it.

Our research consistently shows three main barriers:

This anxiety is well-founded. According to recent case studies, an average homeowner refinancing a $600,000 loan might pay $1,000 in switch fees but can save $189 per month if the rate drops by just 0.5%—breaking even in five months. But not everyone receives this outcome without careful planning.

Let’s bring clarity to the refinancing decision with a step-by-step approach:

Calculate the full expense of switching by adding application, valuation, settlement, discharge, government, title search, legal fees, and possible LMI (if your LVR is above 80%). Don’t forget potential break fees for fixed-rate loans.

| Refinancing Fee | Example Cost |

| Application Fee | $500 |

| Property Valuation Fee | $400 |

| Settlement Fee | $200 |

| Discharge Fee (old lender) | $350 |

| Registration (per title) | $200 |

| Title Search Fee | $80 |

| Legal/Admin | $250 |

| Total Upfront Costs | $1,980 |

If your loan-to-value ratio exceeds 80%, you’ll need to add LMI costs, which can range from $2,000 for smaller loans to $10,000+ for high-value properties.

Determine how much you’ll save in monthly repayments with the new interest rate. For a $600,000 loan with a 27-year remaining term:

| Current Rate | New Rate | Monthly Repayment Difference |

| 6.49% | 5.99% | $189 savings per month |

Divide your total refinancing costs by your monthly savings to determine when you’ll break even:

$1,980 (total costs) ÷ $189 (monthly savings) = 10.5 months

In this example, you’ll recover your refinancing costs in approximately 11 months. If you plan to keep the property longer than this, refinancing makes financial sense.

Consider other advantages beyond interest rate savings, such as:

Emma refinanced her $500,000 loan from 6.49% to 5.99%. Upfront fees totaled $1,200, but her new repayments save her $175/month. She broke even after only 7 months and will pocket more than $6,000 in savings over five years—net of all costs.

Sam chased a headline “low rate” only to discover $900 in annual account and offset fees—eliminating much of his interest rate savings over a 3-year period. Always request a total cost of loan comparison that includes all ongoing fees, not just the interest rate.

Jess attempted to exit her current fixed-rate loan early. The break cost? $4,800—substantially more than her potential interest savings, making refinancing unviable until her fixed term ends.

Many lenders are willing to waive or reduce upfront fees to win your business, especially if:

If you have a fixed-rate loan, wait until your fixed period ends to avoid break fees. If interest rates are falling, consider whether waiting might secure you an even better deal.

Many lenders offer cashback incentives ($2,000-$4,000) for refinancing. These can effectively offset your switching costs, but always check that the ongoing interest rate remains competitive long-term.

A good mortgage broker will:

Refinancing is typically worth considering when:

Refinancing is a powerful tool for home loan holders who want to take control of their financial future—but only if you get crystal clear about all the costs upfront. Most importantly, don’t get seduced by a headline rate—dig into every fee, demand transparency, and model your break-even carefully.

Above all, get expert guidance tailored to your situation. You deserve to refinance with the confidence that you’re building wealth—not just giving it to the bank in sneaky fees.

Book a mortgage review call today – get an exact cost breakdown, bespoke savings analysis, and peace of mind that you’re not leaving money on the table.

Is it still worth refinancing with the current interest rates?

Yes, if your new repayments plus fees result in a lower total cost within your planned timeframe. Calculate your break-even point first—ideally within 2 years—to determine if refinancing makes financial sense for your situation.

What happens if my property value has decreased since I bought it?

If your property value has fallen, your loan-to-value ratio (LVR) will increase, potentially requiring you to pay Lender’s Mortgage Insurance again. In some cases, this could make refinancing financially unviable until property values recover or you pay down more of your loan.

Can I negotiate refinancing fees with lenders?

Absolutely. Always ask which fees they’re willing to waive or reduce. Application fees, valuation fees, and even some legal fees are often negotiable, especially if you have a strong credit profile or are borrowing a significant amount.

Will refinancing affect my credit score?

Yes, but usually only temporarily. Each loan application places an inquiry on your credit file, which can slightly lower your score. However, making regular repayments on your new loan will help rebuild your score over time.

Key Takeaways CommBank raised fixed home loan rates in January 2026, anticipating potential RBA rate hikes. Banks typically adjust fixed...

Key Takeaways Strategic planning, robust financing, and clear investment goals are crucial for building a profitable investment property...