Is Investor Activity Set to Fall?

Australia's property investors are facing a double headwind in 2026 - and the latest lending data confirms the retreat has already begun....

The 2021 Australian property boom was not a mystery. But most of the commentary at the time got it wrong – chalking it up to pandemic psychology, stimulus cheques, and Australians having nowhere to spend their money but on houses. The real story is more precise, more data-driven, and far more useful if you want to understand whether the next property boom in Australia is already forming beneath your feet.

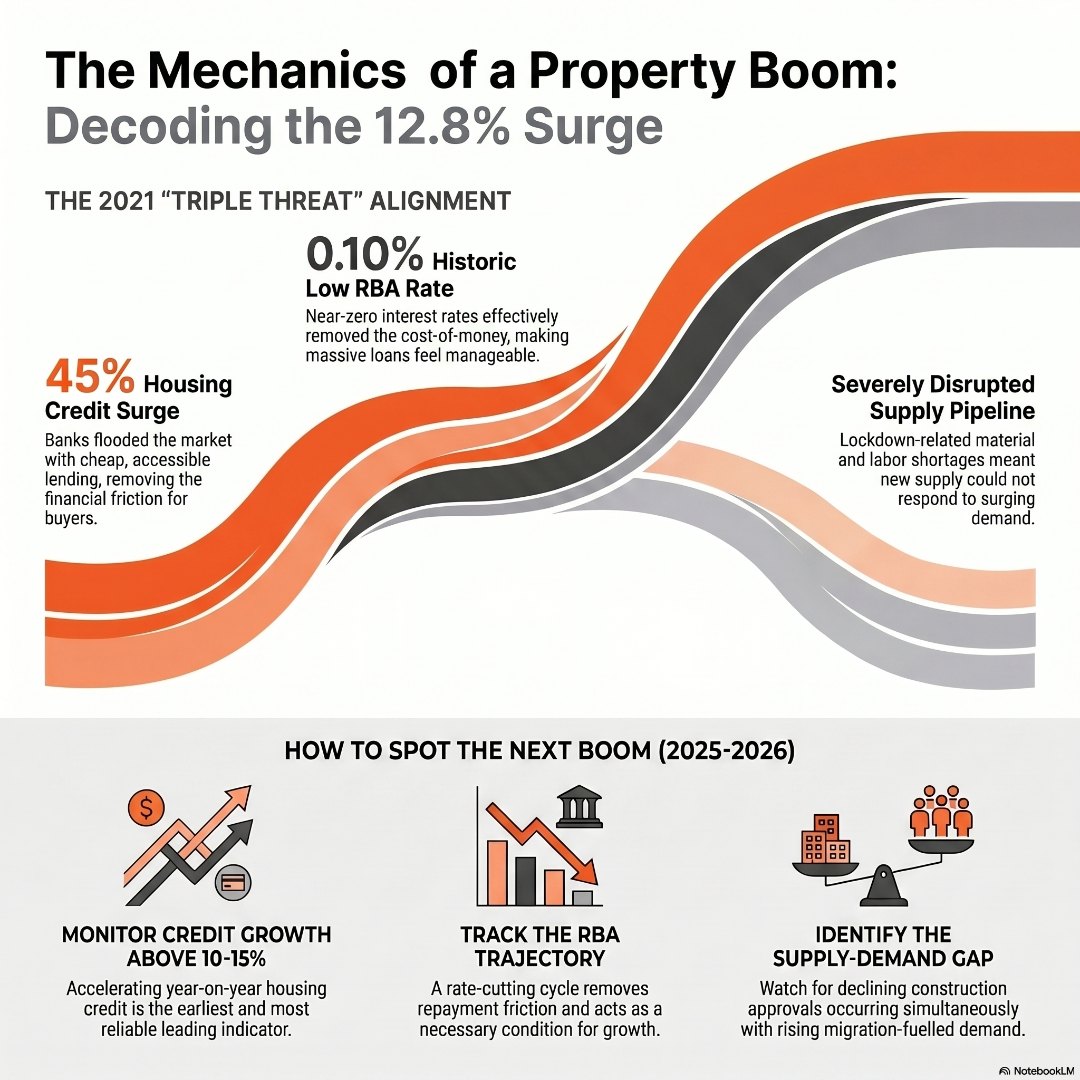

National dwelling values surged 12.8% across Australia in a single calendar year – the largest single-year deviation above the long-run average ever recorded across a dataset of more than 7,200 suburban markets going back to 2003. That is not a blip. That is a structural event. And it was caused by three specific forces aligning simultaneously in a way that had never happened before.

The honest answer requires putting three numbers on the table.

First, housing credit surged by 45% year-on-year. Banks flooded the market with cheap, accessible lending. Borrowers who might have hesitated were suddenly pre-approved, well-funded, and competing hard for the same limited stock. The cost of money had almost entirely evaporated from the decision.

Second, the RBA cash rate sat at a historic low of 0.10%. That is not just low – it effectively removed all cost-of-money friction for buyers. Variable rates were sub-2%. Fixed rates were being offered at under 2% for two and three-year terms. For investors and owner-occupiers alike, the repayment on a $700,000 loan had never felt more manageable.

Third – and this is the piece most commentators missed – the residential construction pipeline had been severely disrupted during COVID-19 lockdowns. Builders were delayed. Material costs spiked. Labour shortages meant projects ran months behind schedule. New supply simply could not respond to the explosion in demand.

When credit, rates, and supply all move in the same direction at the same time – cheap credit up, interest rates down, new supply constrained – prices do not just rise. They spike. The data model that tracked these three variables predicted the 2021 national result to within 0.05 percentage points across the full dataset. That is not luck. It is mechanics.

Understanding how interest rates affect property investment strategies is one of the most important frameworks any property investor in Australia can develop – because rates are rarely the whole story, but they are almost always part of it.

The dominant narrative in 2021 was emotional. FOMO. Pandemic savings. Lifestyle shifts from apartments to houses. Australians discovering the appeal of regional living.

All of those things were real. None of them were the cause.

FOMO is a symptom of a rising market, not the driver of one. When credit is loose, rates are near zero, and supply cannot keep up with demand, prices rise whether buyers feel anxious about missing out or not. Emotional explanations make for compelling headlines, but they do not help you predict what comes next.

The investor who understands the Australian property market cycle in data terms – not sentiment terms – is the one positioned to act strategically rather than reactively. The question is not “are people excited about property right now?” It is “which of the three structural drivers are currently aligned?”

You can get a useful grounding in what drives property prices in Australia before applying this lens to current conditions.

The honest answer is: not easily – at least not in the same form.

That precise three-way alignment of cheap credit, near-zero rates, and constrained construction was a genuinely rare confluence. The RBA is unlikely to return to 0.10% in the near term. The lending environment, while accommodating, is not producing the 45% year-on-year credit growth we saw in 2021. And while construction is still challenged, it is not experiencing the same level of acute lockdown-era disruption.

But here is the more instructive point: you do not need all three drivers aligned to produce significant above-average growth. Even partial overlap – two of the three forces moving in the same direction – can produce meaningful price pressure across specific markets.

In 2025-2026, two of those drivers are active simultaneously. Migration-fuelled demand has placed sustained pressure on the rental market and is now flowing through to purchase intent. Residual credit momentum, supported by recent RBA rate reductions, is re-engaging borrowers who sat on the sidelines during the 2022-2023 rate-hiking cycle. Supply remains structurally short across most capital cities and many regional centres.

This does not mean we are on the verge of another 12.8% national surge. What it does mean is that certain markets – particularly those where demand concentration meets supply shortfall – are already generating conditions worth paying attention to.

For context on where we currently sit in the cycle, the property market cycle buyer’s guide breaks down the four phases and how each one informs smart buying decisions.

Understanding the conditions that cause a boom is only half the equation. The other half is knowing how to act strategically when those conditions are forming.

The framework is straightforward once you know what to look for.

Watch credit growth first. When year-on-year housing credit growth starts accelerating beyond 10-15%, the lending conditions for a boom are forming. This is the earliest and most reliable leading indicator.

Watch the RBA cash rate trajectory second. Not just the current rate – the direction. A rate-cutting cycle that removes repayment friction from the market is a necessary, though not sufficient, condition for above-average price growth.

Watch construction approvals and completions third. When new dwelling approvals decline at the same time demand is rising, the supply constraint that turns growth into a spike is beginning to form. Right now, why the RBA rate cut has not yet triggered a property boom is one of the most relevant live questions in the Australian market – and the answer lies in exactly these dynamics.

None of this requires a crystal ball. It requires a disciplined framework and access to current data.

If you are sitting on the fence waiting for certainty, this is worth considering: the 2021 boom did not announce itself. It formed quietly, driven by data signals that most buyers were not watching. By the time it became obvious, the best entry points had already passed.

I have seen the cost of waiting up close, and it stays with you. I first met her in 2005 – a smart, capable woman who was convinced she was being sensible. Property prices in her target area were moving fast, and she wanted to wait until things “settled down.” We spoke again a few years later. Still waiting. Then again after the GFC. Still watching. By the time I last caught up with her, she had sat out multiple growth cycles and could only afford to buy in suburbs she had never once considered her goal. The market had not crashed and handed her the entry point she was holding out for. It had simply moved on without her. What struck me was that she was not reckless or careless – she was actually doing the opposite. She was being cautious, measured, patient. But patience without a framework for reading the data is not strategy. It is just waiting with a story attached. The investors I have seen benefit most from booms, partial or full, are rarely the ones who timed it perfectly. They are the ones who understood which signals mattered, acted when two or three of those signals aligned, and did not let the noise of the broader market talk them out of a well-researched position.

The strategic investor in 2025-2026 is not asking “when will the boom happen?” They are asking “which of the three drivers are currently active, and where are they overlapping in specific suburban markets?”

That question requires real data – not forecast headlines, not vendor marketing, not market sentiment surveys. It requires suburb-level analysis of rental vacancy, population flows, credit conditions, and construction pipelines.

If you want that kind of edge, the Investors Choice Mortgages Hub is built for exactly this kind of decision-making – combining real data, smart calculators, and the kind of old-fashioned personalised broker support that actually picks up the phone when you call. Because when two or three of those market drivers align, the window to act is shorter than most people expect. Book a mortgage review call today and make sure you are positioned before the broader market catches up.

What actually caused Australian house prices to surge so dramatically in 2021?

Three market drivers aligned simultaneously for the first time ever recorded across a large dataset of Australian suburban markets: housing credit surged 45% year-on-year, the RBA cash rate hit a historic low of 0.10%, and the residential construction pipeline was severely disrupted during COVID-19 lockdowns. The combination of abundant cheap credit, near-zero borrowing costs, and constrained new supply created a supply-demand imbalance that drove prices up 12.8% nationally in a single year.

Is the next property boom in Australia going to be as big as 2021?

Almost certainly not in the same way. The precise three-way alignment of 2021 was a rare confluence of conditions that required an extraordinary policy environment and a once-in-a-generation supply disruption. However, partial alignment of two of the three major drivers – such as migration-driven demand alongside rate reductions and tight supply – can still produce significant above-average growth in specific markets, which is what current data suggests for parts of Australia in 2025-2026.

How do interest rates affect property prices in Australia?

Interest rates directly affect how much borrowers can afford to repay, which in turn influences how much they are willing and able to pay for property. When rates fall, borrowing capacity increases, more buyers enter the market, and competition for limited stock pushes prices higher. However, rates alone do not cause a boom – they need to align with strong demand and constrained supply to produce the kind of price acceleration seen in 2021.

How can I tell if Australia is heading into another property boom?

Watch three leading indicators: year-on-year growth in housing credit (above-average credit growth signals loose lending conditions), the direction of the RBA cash rate (a cutting cycle removes repayment friction), and new dwelling construction approvals and completions (declining approvals during rising demand creates a supply constraint). When two or more of these indicators align in the same direction, above-average price growth tends to follow in the markets where demand is most concentrated.

All market data and research referenced in these articles is sourced from HTAG Analytics’ April 2026 research report: “A Forced Autoregressive Model of Australian Residential Property Price Dynamics: Credit, Migration, Monetary Policy, and Supply Interactions 2003–2026” by Alex Fedoseev and Dr. Matija Djolic, HTAG Analytics.

Investors Choice Mortgages acknowledges HTAG Analytics as an industry-leading source of Australian property market intelligence.

Australia's property investors are facing a double headwind in 2026 - and the latest lending data confirms the retreat has already begun....

Australia's 2026 Federal Budget has delivered the most significant tax reform for property investors in more than 25 years, reshaping the rules...