If you’ve been watching the news, refreshing property listings, and waiting for the RBA rate cut property market surge to kick in – you’re not alone. Rates have dropped. Repayments are easing. And yet the boom you were expecting hasn’t quite arrived. The market feels strangely quiet. House prices haven’t exploded. Your suburb looks basically the same as it did three months ago.

So what’s actually going on?

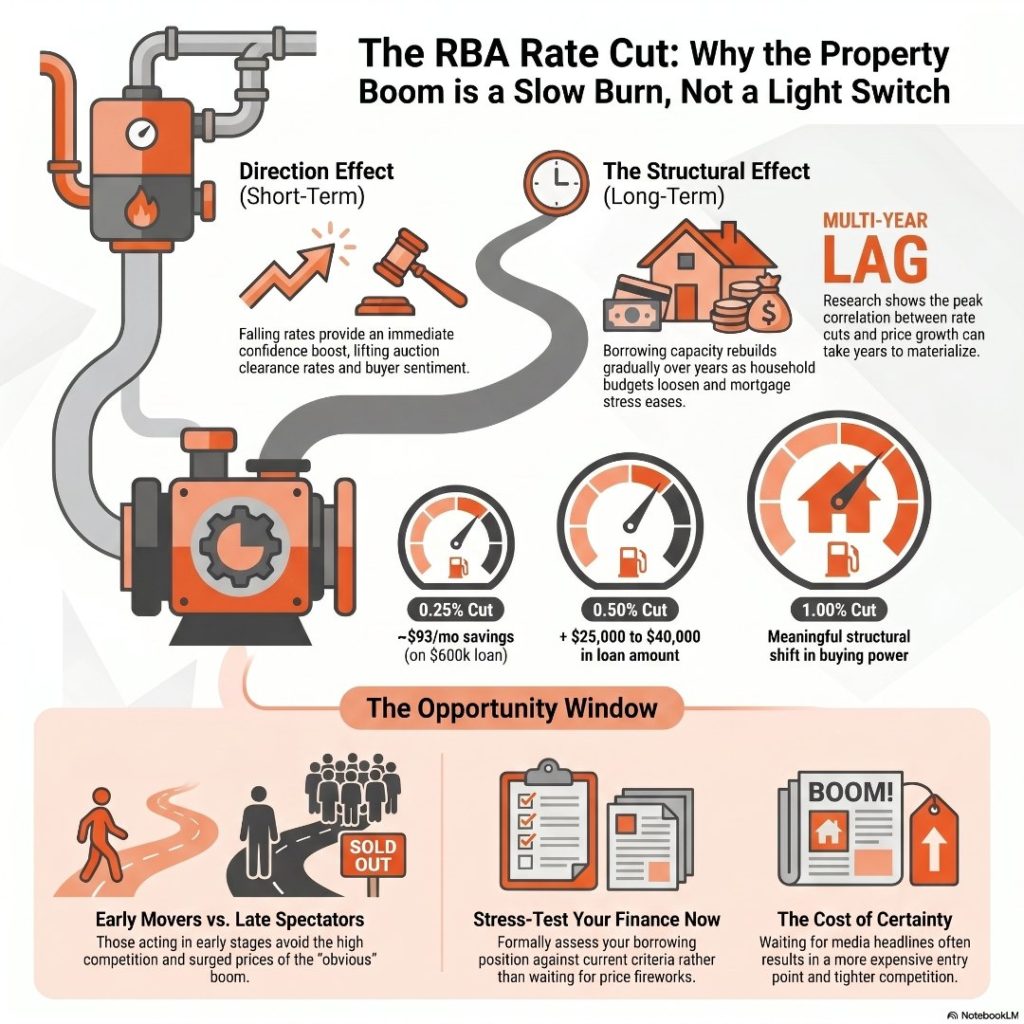

The short answer is that rate cuts do matter – enormously. But the relationship between monetary policy and property prices in Australia is not a light switch. It’s more like a slow-burning engine that takes time to reach full speed. Research analysing more than two decades of national market data suggests the full effect of monetary policy on Australian property prices can take up to five years to completely play out. The peak correlation between the cash rate and property price growth doesn’t appear in the months after a cut – it appears years later.

That’s not pessimism. That’s one of the most important things any buyer or investor can understand right now.

Key Takeaways

- The full impact of an RBA rate cut on Australian property prices can take years to materialise, not weeks.

- There are two separate effects of monetary policy – a short-term confidence boost and a much deeper structural shift in borrowing capacity and mortgage stress.

- The 2022-2023 rate hiking cycle is still unwinding through the market even as cuts begin.

- Buyers who act in the early stages of a rate-cut cycle consistently outperform those who wait for obvious price signals.

- Now is the time to stress-test your borrowing capacity and get your finance strategy ready – not to sit back and watch.

Do Rate Cuts Actually Increase House Prices in Australia?

Most people assume that when the RBA cuts rates, banks immediately lower mortgage repayments, buyers flood back into the market, demand surges, and prices follow. And to some degree, that does happen. But that’s only part of the story – and it’s the smallest part.

There are two distinct effects at work whenever the RBA moves the cash rate.

The first is the direction effect. When rates start falling, confidence lifts. Buyers who had been sitting on the fence start re-entering the market. Auction clearance rates tick up. Some early momentum builds. This is the visible, near-term signal that gets reported in the media.

The second is the structural effect. This is where the real power lies, and it works on a far longer timeline. As rates fall, borrowing capacity slowly rebuilds across hundreds of thousands of Australian households. Mortgage stress eases. Household budgets loosen. Over time, this unlocks genuine additional demand that wasn’t there before.

This structural shift doesn’t happen in a month or even a year. It unfolds gradually, as fixed-rate borrowers roll off onto lower variable rates, as confidence in job security improves, and as the cumulative weight of reduced repayments frees up disposable income. Understanding your own borrowing capacity and how it shifts with rate changes is the first step to positioning yourself ahead of that structural shift.

The Shadow of the 2022-2023 Rate Hiking Cycle Is Still Playing Out

Here’s something that often gets missed in the current conversation: the damage done by the most aggressive rate-hiking cycle Australia has seen in a generation hasn’t finished working its way through the system.

Between 2022 and 2023, the RBA lifted the cash rate from a historic low of 0.10% to 4.35% in just over a year. Thirteen consecutive rate rises. For a country where household debt is among the highest in the developed world, that was a significant structural shock. Hundreds of thousands of borrowers saw their monthly repayments jump by $1,000 or more.

That pain doesn’t simply reverse when rates start falling. Households that stretched their finances during the low-rate era are still rebuilding their buffers. Consumer confidence – particularly around big-ticket decisions like property – takes time to recover.

This is precisely why you might look at your suburb right now and see modest listings, cautious buyers, and prices that feel like they’re treading water. The hiking cycle is still doing its work in the background, even as cuts begin. The two forces are running simultaneously.

For a clear explanation of how the cash rate directly affects your repayments, read our guide on how RBA rate changes directly impact your mortgage.

Should I Buy Property Now or Wait for the Boom After an RBA Rate Cut?

Here is the question that matters most. And the honest answer is: waiting for certainty is one of the costlier decisions you can make in property.

History is consistent on this. Buyers who move in the early stages of a rate-cut cycle – before the demand surge is obvious, before the headlines start screaming about booming prices – consistently outperform those who wait until the market has already run.

I think about a woman I first spoke with around 2005. She was watching the Sydney market closely and convinced herself prices were moving too fast – that a correction was surely coming, and she would buy then. So she waited. I crossed paths with her again years later, and she was still waiting. She had watched an entire growth cycle pass her by. When I dug back through my emails once, I found a similar situation: someone who had written to me wanting to get into the market, then written again two years later with the exact same concerns, still on the sidelines. By the time she finally moved, the gap between what she could have paid and what she now had to pay had grown by tens of thousands of dollars. Those two stories have stayed with me across every market cycle I have watched since – because the pattern is always the same. The people who wait for certainty do not get certainty. They get a more expensive entry point, tighter competition, and the quiet, uncomfortable realisation that the window they were saving themselves for had already closed.

The preparation window in a rate-cut cycle works exactly the same way. Think about what “waiting for the boom” actually means in practice. It means waiting until:

- Borrowing capacity has already expanded for everyone, pushing up competition

- Vendor confidence has returned and price expectations have risen

- The media is running weekly stories about surging property values

- Every buyer who was sitting on the sidelines is now competing with you

By the time a post-rate-cut boom is obvious, you’re buying into it – not ahead of it. The preparation window closes quietly, without announcement.

This doesn’t mean charging in without a strategy. It means getting finance-ready, understanding your actual borrowing position, and acting decisively when the right property appears. Learning how to stress-test your mortgage position in the current environment is the most valuable step you can take right now.

Will a Rate Cut Increase My Borrowing Capacity in Australia?

Yes – but gradually. When the cash rate falls, banks reassess the serviceability buffers they apply to loan applications. In simple terms, a lower cash rate means a lower baseline rate, which means lenders calculate your ability to service a loan from a lower starting point.

On a practical level, a 0.50% reduction in rates can increase a typical borrower’s maximum loan amount by roughly $25,000 to $40,000 – depending on income and existing commitments. A full 1% reduction could shift the number meaningfully higher. Across a full cutting cycle, the cumulative effect on borrowing capacity is substantial.

But here’s the timing issue: APRA’s serviceability buffer requirements mean banks add a minimum 3% buffer on top of the current product rate when assessing new applications. Even as rates fall, the full benefit to borrowing capacity takes months to flow through. This is another reason the Australian property market forecast doesn’t show an immediate explosion – the structural uplift in buying power builds gradually, not all at once.

What to Do Right Now

Given everything above, here is a practical framework:

- Know your current borrowing position. Not what it was twelve months ago. Get it formally assessed against current bank criteria and the most recent rate movements.

- Understand what rate cuts will do to your specific loan. A $600,000 variable mortgage saves roughly $93 per month for every 0.25% rate reduction. A $900,000 mortgage saves around $140 per month. Across a full cutting cycle, that relief compounds – and can be redirected into an offset account or deposit savings.

- Don’t wait for price fireworks to start looking. The research and suburb selection work you do now – while competition is still modest – is far more likely to deliver a quality outcome than rushed decisions made when buyer urgency is high.

- Stress-test your position for what comes next. Rates may fall further, or they may stabilise. Build your strategy to work across a range of scenarios.

Conclusion

The RBA rate cut property market story isn’t over – it’s just getting started. The absence of an immediate boom isn’t a failure of monetary policy. It reflects how deeply and slowly economic forces move through a complex, high-debt economy like Australia’s.

The multi-year lag between rate changes and their full property market impact is not a reason to be passive. It’s a window of opportunity for prepared buyers and investors to move decisively while competition is still subdued, prices are still rational, and the full wave of demand hasn’t yet built.

Rate cuts are your green light to prepare – not to spectate. Get your borrowing capacity assessed, stress-test your strategy, and position yourself ahead of the structural shift that’s already underway.

The Investors Choice Mortgages Hub gives you access to tools and broker expertise to stress-test your position right now. The Mortgage Stress Test, Fix or Float Assessor, and Portfolio Profiler tools are built precisely for market conditions like these.

Frequently Asked Questions

Why hasn’t the RBA rate cut made house prices go up immediately?

The relationship between rate cuts and property prices involves two effects – a short-term confidence boost, and a deeper structural shift in borrowing capacity and mortgage stress that takes years to fully play out. Research across more than two decades of Australian data suggests the peak correlation between the cash rate and property price growth occurs with a multi-year lag, not in the months following a cut. The market doesn’t ignore rate cuts – it absorbs them slowly.

Do RBA rate cuts always cause a property boom in Australia?

Not always, and not immediately. Rate cuts are one of several factors that influence the property market, alongside housing supply, consumer confidence, lending conditions, wage growth, and population dynamics. Historically, sustained rate-cut cycles have preceded property price growth, but the timing varies significantly. The first few months of a cutting cycle often look underwhelming compared to what follows.

Will a rate cut increase my borrowing capacity in Australia?

Yes, but gradually. As the cash rate falls, the baseline assessment rate used by lenders also falls over time. A 0.25% rate reduction can increase a typical borrower’s maximum loan amount by $25,000 to $40,000 depending on income and existing debt. However, APRA’s 3% serviceability buffer requirement means the full benefit flows through to new loan assessments over months, not overnight.

Should I buy property now or wait for the market to rise after an RBA rate cut?

Buyers who act in the early stages of a rate-cut cycle – before prices have already risen – consistently achieve better outcomes than those who wait for clear market signals. By the time a post-rate-cut boom is obvious, prices have typically already moved. If your finance is ready and your strategy is sound, acting now while competition is still modest is likely to deliver a better result than waiting for certainty.

All market data and research referenced in these articles is sourced from HTAG Analytics’ April 2026 research report: “A Forced Autoregressive Model of Australian Residential Property Price Dynamics: Credit, Migration, Monetary Policy, and Supply Interactions 2003–2026” by Alex Fedoseev and Dr. Matija Djolic, HTAG Analytics.

Investors Choice Mortgages acknowledges HTAG Analytics as an industry-leading source of Australian property market intelligence.