What Do the 2026 Budget Tax Changes Mean for Your Property Investment Strategy in Australia?

Australia's 2026 Federal Budget has delivered the most significant tax reform for property investors in more than 25 years, reshaping the rules...

Consolidating credit card and personal debt into your home loan can genuinely reduce your monthly repayments – sometimes by hundreds of dollars – but most people are never shown the full picture of what that decision costs over the life of a 25 or 30-year mortgage. For households already feeling the pressure of rising living costs, higher fuel and energy bills, and persistent rate uncertainty, rolling short-term high-interest debt into a secured home loan feels like an obvious fix. Whether it actually is depends entirely on the numbers you run before you sign – not after.

Picture the scene. You open your banking app on a Tuesday morning and there it is again – the credit card minimum, the personal loan instalment, and the mortgage repayment, all jostling for space. You have done everything right. You bought a home. You have built up equity. But somewhere along the way, a few thousand dollars of credit card debt became ten thousand, a personal loan topped up the car, and now four separate creditors are quietly draining your cash flow every single month.

In an environment where grocery bills have climbed, energy costs have spiked, and any talk of interest rate movements sends a ripple of anxiety through the household budget, the idea of rolling all that debt into your home loan and making one lower repayment sounds like the relief you have been waiting for. And here is the thing – it can be. But only if you understand what you are actually agreeing to.

I grew up in a household where debt was treated with deep suspicion. My family’s message was simple: pay it off as fast as you can, and do not borrow more than you have to. That instinct is not wrong – but it is incomplete. What I have learned over nearly two decades as a mortgage broker is that the question is rarely “should I have this debt?” It is “do I understand exactly what this debt is costing me, and am I making a deliberate choice about it?” There is a meaningful difference between debt that quietly erodes your wealth and debt you have structured to work in your favour. The families who get ahead are the ones who learn to tell those two apart – and who run the numbers rather than react to the feeling.

When you consolidate credit card and personal debt into your mortgage, the immediate effect is almost always positive. Your monthly cash flow improves. The mental load of tracking multiple repayments disappears. Your household budget finally has breathing room.

But here is the maths that most people are never shown.

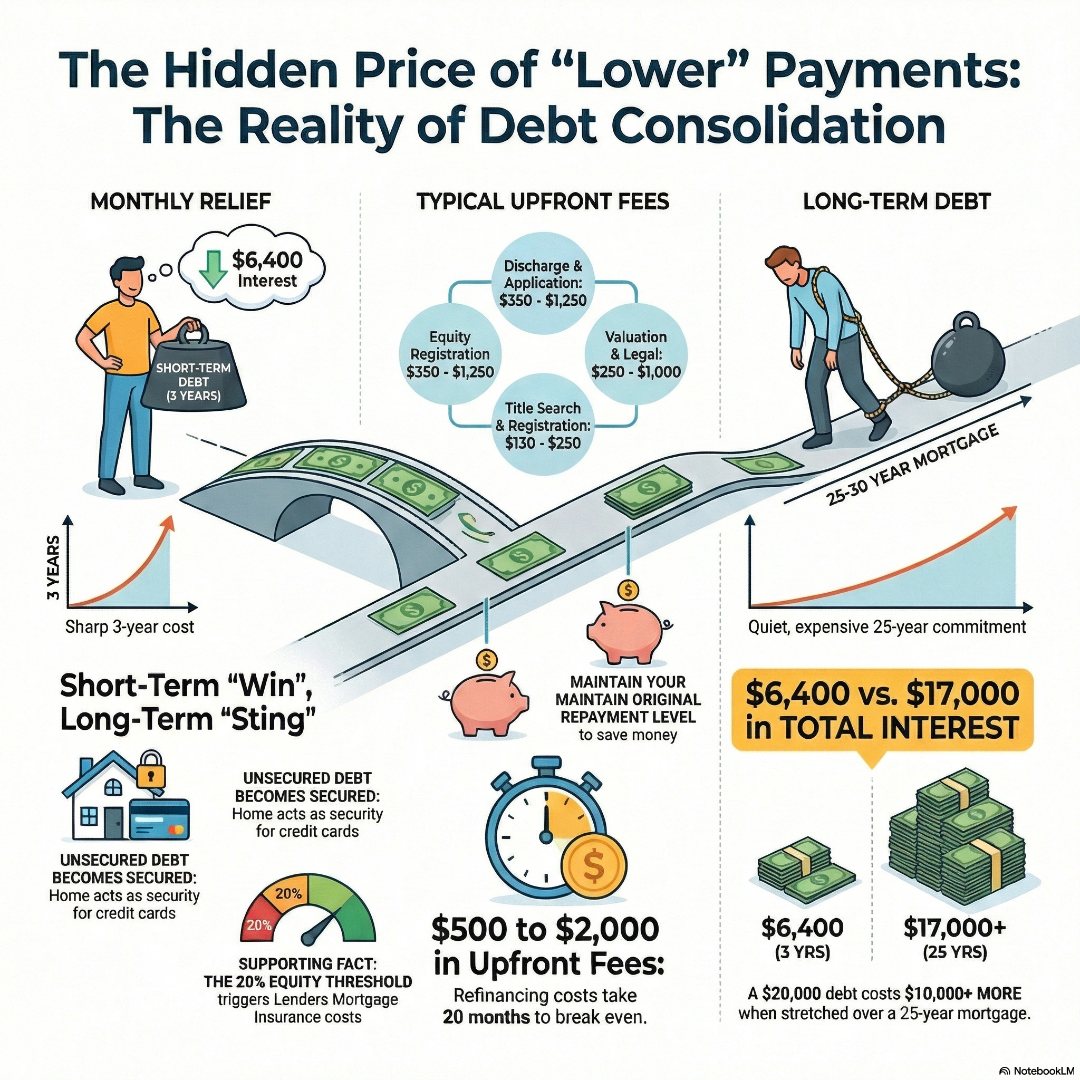

Suppose you carry $20,000 in credit card debt at 19.99% interest. If you paid that balance off over three years, the total interest would be approximately $6,400. That stings – but it is finite, and it ends in three years.

Now consider rolling that same $20,000 into your home loan at 6%, with 25 years remaining on your mortgage. The total interest on that portion alone climbs to roughly $17,000. You have traded a painful short-term cost for a longer, quieter one – and it has cost you more than double.

The lower monthly repayment felt like winning. The full-term interest bill tells a very different story. This is the core tension at the heart of every consolidation decision. The interest rate comparison only answers half the question. The loan term answers the other half – and it is the half that catches people out.

Before you can even begin to enjoy the benefits of consolidation, you need to clear the starting costs. Refinancing to consolidate debt is not free, and the upfront fees need to factor into your decision.

Here is what a typical refinance in Australia costs:

| Fee Item | Typical Range |

| Discharge fee (existing lender) | $350 – $500 |

| Application fee (new lender) | $0 – $750 |

| Property valuation fee | $50 – $600 |

| Legal and settlement fees | $200 – $400 |

| Title search and registration | $130 – $250 |

Total upfront costs commonly land between $500 and $2,000. If you are saving $100 per month on consolidated repayments, you are looking at 5 to 20 months before you break even – before you are genuinely ahead. For a full breakdown of what refinancing actually costs in Australia, including scenarios where Lenders Mortgage Insurance is triggered, see our complete guide to refinancing costs in Australia.

If your loan-to-value ratio exceeds 80% after adding the consolidated debt, Lenders Mortgage Insurance could add thousands more to your upfront bill – which can wipe out the interest savings entirely in the early years.

Debt consolidation done strategically can genuinely build wealth rather than quietly erode it. The key is that you commit to maintaining your repayment level – not simply enjoying the lower minimum.

Here is the approach that works. When you consolidate and your minimum repayment drops, you do not pocket that difference. You continue repaying at the same level you were before consolidation. The lower interest rate then does real work – paying down principal faster and shortening your effective loan term.

This strategy works best for homeowners who:

For property investors, strategic consolidation can serve a second purpose. High-interest consumer debts reduce your assessed borrowing capacity when lenders review your serviceability. Cleaning those up can open the door to your next investment. For more on this, read our guide on strategies to improve your borrowing capacity for property investment.

There is one shift in this strategy that deserves very clear attention. Before consolidation, your credit card debt and personal loans are unsecured. If your financial situation deteriorates, those creditors have limited ability to take your home. Once you roll those balances into your mortgage, your home is now the security for debts that previously carried no such risk.

This is not a reason to avoid consolidation. It is a reason to go in with a defined plan – and to make sure the strategy is built around your long-term position, not just this month’s cash flow relief.

The smartest thing you can do before making any consolidation decision is model the real numbers – not the monthly repayment comparison, but the full interest bill across the life of your loan.

Most comparison tools show you rate versus rate. What you need to see is total interest across your loan term, the break-even point for your refinancing costs, and what happens to that figure if you maintain your current repayment level versus dropping to the new minimum.

For a deeper look at whether refinancing to consolidate actually saves money on interest – with real examples and the maths fully worked through – see does refinancing to consolidate debt actually save you money on interest?

Consolidation is likely the right move if you:

Think carefully before proceeding if you:

Understanding how consolidating debt by refinancing actually works – step by step – will also help you map your specific situation against the mechanics before you speak to a lender.

Consolidating credit card and personal debt into your home loan is a powerful strategy when it is built around a clear understanding of the true cost – not just the monthly payment relief. The lower rate is real. The cash flow improvement is real. But the long-term interest bill, the upfront refinancing fees, and the shift in risk profile are equally real, and they need to be part of your calculation from the start.

The homeowners who benefit most from this strategy are the ones who run the full numbers before they commit – and who go in with a repayment plan that uses the lower rate to their advantage rather than simply extending their debt over another decade.

Try the Debt Consolidation Calculator in the ICM Hub – giving our clients an unfair advantage – and discover what the true cost of debt consolidation really is before you make any decisions.

What are the true costs of consolidating credit card debt into my home loan?

The true cost has two components. The first is upfront: refinancing fees typically between $500 and $2,000, plus potential Lenders Mortgage Insurance if your equity drops below 20% of your property value. Most lenders in Australia require your loan-to-value ratio to remain at 80% or below after the consolidation, so your property value needs to be high enough that your existing mortgage plus the additional consolidated debts does not exceed that threshold. The second cost is ongoing: by stretching short-term high-interest debt over a 25 or 30-year mortgage, you can pay significantly more total interest even at a lower rate. For example, $20,000 of credit card debt cleared in three years might cost $6,400 in interest. The same balance folded into a 25-year mortgage at 6% costs closer to $17,000. Running a full debt consolidation calculator before committing is essential.

Is it worth consolidating personal debt into my home loan during a period of rising interest rates and cost of living pressure?

It can be, but the environment matters. If your home loan rate is still materially lower than your credit card and personal loan rates – which it almost certainly is – the interest rate case for consolidation remains valid. The risk in a high-rate environment is that your home loan rate is higher than it was, reducing the interest rate gap. The more important variable is loan term: consolidating into a long mortgage term at even a lower rate can cost more in total interest than paying down shorter debts aggressively. Model both scenarios with real numbers before deciding.

Does consolidating debt into my mortgage hurt my borrowing capacity for future property investment?

Not necessarily – in fact, the opposite is often true. High-interest consumer debts with high monthly commitments reduce your assessed serviceability when lenders review your application for an investment loan. By consolidating those debts at a lower rate and lower monthly commitment, you can improve the income-to-debt ratio lenders use to calculate how much you can borrow. This is why for property investors, debt consolidation is often a strategic step toward the next purchase, not just a cash flow fix.

What hidden fees should I look out for when consolidating debt by refinancing?

The fees most people overlook are break costs on any existing fixed-rate loans (which can run into thousands of dollars), Lenders Mortgage Insurance if the consolidated loan pushes your LVR above 80%, and ongoing account or package fees on the new loan that can quietly erode your interest savings over time. Always request a full cost-of-loan comparison, not just the interest rate, and calculate your specific break-even point before proceeding.

Australia's 2026 Federal Budget has delivered the most significant tax reform for property investors in more than 25 years, reshaping the rules...

Regional property markets are outperforming capital cities across Australia right now, with dwelling values rising 3.3% over the three months to...