Why Are Interest Rates Rising – and Who Will It Hit Hardest?

If you have a variable rate mortgage right now, you already feel it. Each time the Reserve Bank of Australia moves the cash rate, your...

If you have a variable rate mortgage right now, you already feel it. Each time the Reserve Bank of Australia moves the cash rate, your repayments shift. But the more pressing question many Australians are asking is not just what already happened. It is why are interest rates rising again, and is this the new normal?

The honest answer is that nobody – not economists, not bank analysts, not the media commentators confidently appearing on the 6 o’clock news – can predict the next move with certainty. What we can do is understand the forces driving rate decisions, identify who carries the heaviest burden when rates climb, and make smarter choices in the meantime.

I did not arrive at this work through textbooks. My father was a careful, hardworking man who invested his savings with a company called Estate Mortgage in the late 1980s. When interest rates soared – and they soared fast – Estate Mortgage collapsed. He lost everything. I watched it happen and I believe, with everything I have, that the grief and stress of that loss contributed to his death. That experience did not paralyse me. It lit a fire. It became the reason I spent 20 years as a mortgage broker, the reason I built Investors Choice, and the reason I have spent the better part of two decades sitting across the table from everyday Australians helping them understand their numbers before rates move – not after. So when I talk about stress-testing your repayments, reviewing your loan structure, or acting sooner rather than later on your portfolio, I am not repeating something I read in a financial journal. I am telling you what I wish someone had told my father. The consequences of being unprepared are not abstract. They are personal. And they are preventable.

To understand the mechanics, you need to understand what the RBA is actually trying to do.

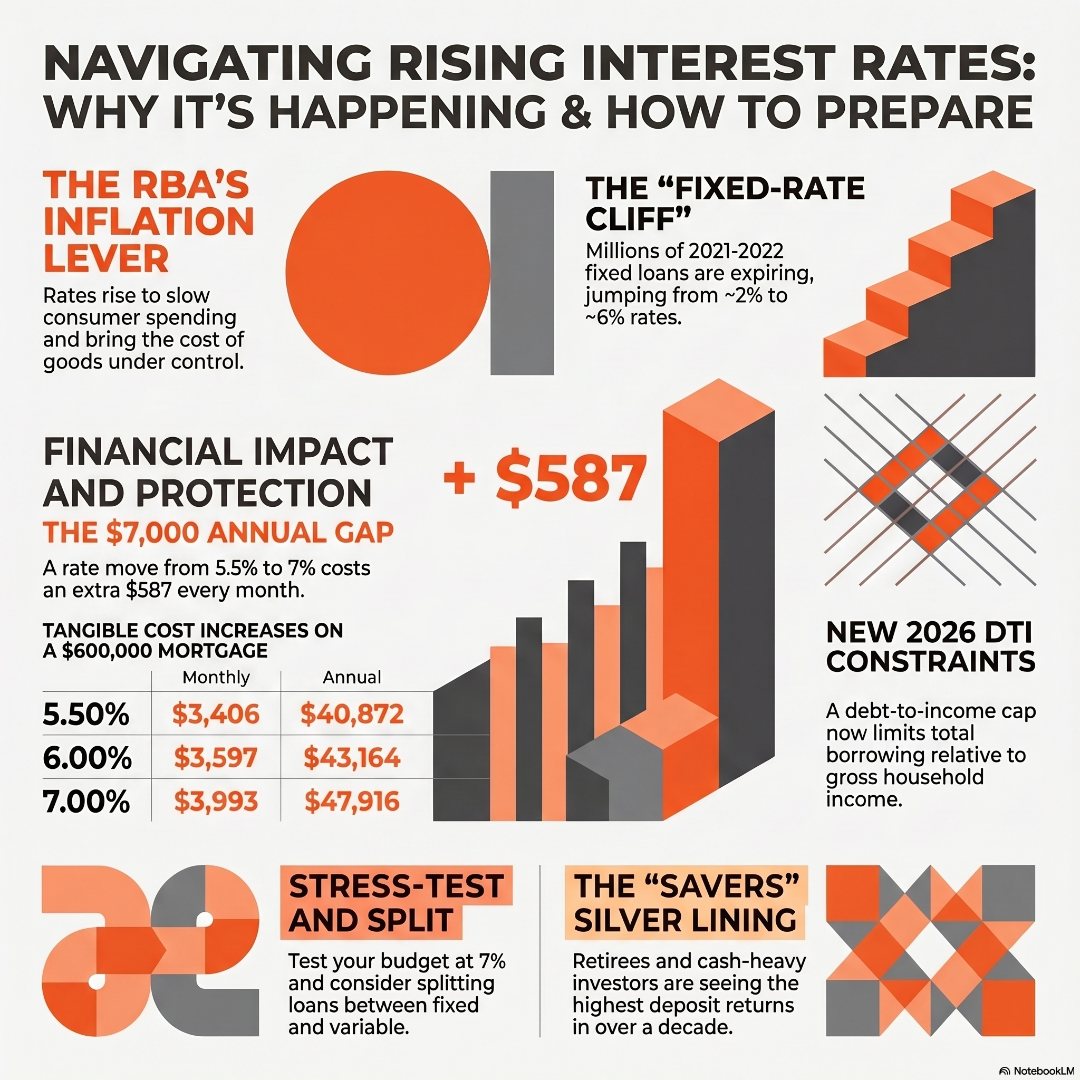

When inflation runs hot – meaning the cost of everyday goods and services rises faster than wages can absorb – the RBA lifts the cash rate. Higher rates make borrowing more expensive, which slows consumer spending, cools the economy, and over time, brings prices back to a sustainable level. It is a blunt instrument, but it is the primary lever available.

Australia has experienced prolonged inflation pressures driven by a combination of global supply disruptions, a tight labour market, strong government stimulus during the pandemic era, and elevated domestic demand. Even as some of those pressures ease, the RBA has remained cautious. Cutting rates too early risks reigniting inflation. Holding them steady or lifting further signals the board believes the job is not yet done.

The catch? There is usually a 12 to 18 month lag between a rate change and its full effect on the economy. That means decisions made today are responding to economic data from months ago. The RBA is, to some extent, steering by looking in the rear-view mirror.

For a deeper look at the relationship between rate rises and inflation, read our article on why interest rates rise during inflation. To understand exactly how the RBA cash rate flows through to your home loan, read our breakdown of how RBA rate changes directly impact your mortgage.

Not all borrowers are equal when rates rise. Three groups carry a disproportionate share of the burden.

If you are on a variable rate loan, every RBA hike hits your repayments almost immediately. With variable rates for owner-occupiers currently sitting around 5.5% and investors tracking closer to 5.7%, a household with a $600,000 loan paying principal and interest is already spending roughly $3,600 per month. An additional 50 basis point rise pushes that closer to $3,750. That is $150 more every month – real money out of a real budget.

Property investors currently represent around 40.6% of total new loan commitments in Australia – close to record territory. Many of these investors are relying on rental income and capital growth to justify their borrowing position. When rates rise, the gap between rental income and loan repayments narrows. A portfolio that was cash flow neutral at 5% can quickly become negatively geared beyond what tax benefits can offset at 6% or higher.

If you are an investor questioning your exposure, our guide on what happens if interest rates rise on your investment loans walks through the real numbers.

Millions of Australian households locked in fixed rates in 2021 and 2022 when the cash rate was sitting at emergency lows – some as low as 1.9% for a two-year term. Those fixed periods are expiring. When they revert to current variable rates, the repayment shock can be significant. A household that fixed at 2.2% on a $700,000 loan and now rolls to 5.7% faces a monthly repayment increase of over $1,200. That is the fixed-rate cliff, and it is real.

Here is a scenario that brings the numbers to life.

$600,000 loan, 30-year principal and interest term:

| Rate | Monthly Repayment | Annual Repayment |

| 5.50% | $3,406 | $40,872 |

| 6.00% | $3,597 | $43,164 |

| 6.50% | $3,793 | $45,516 |

| 7.00% | $3,993 | $47,916 |

The difference between 5.5% and 7% is almost $7,000 per year. That is not an abstract statistic. That is a family holiday, a year of groceries, or three months of private school fees. For many households already stretched by the cost of living, it is genuinely unmanageable without structural changes.

This is precisely why stress-testing your repayments at 6%, 6.5%, and 7% is not pessimism. It is preparation.

Rising rates are not the only headwind for borrowers. In February 2026, a new regulatory requirement introduced a debt-to-income (DTI) cap across Australian lenders.

In practical terms, this cap limits how much total debt a lender can approve relative to your gross income – including all existing loans. For investors looking to expand their portfolio, this is a significant constraint. It may mean that even if you can comfortably service additional debt on paper, the DTI cap prevents the lender from approving your application. The window to build a larger portfolio before that cap tightens further is narrowing.

If your borrowing capacity is under pressure, these strategies to improve your borrowing capacity for property investment are worth reviewing now rather than later.

It would be misleading to frame rising rates as purely bad news. For one group, higher rates are genuinely welcome: savers.

High-yield savings accounts, term deposits, and other cash-based instruments are paying returns that have not been seen in over a decade. In 2021, a term deposit might have returned 0.5% per year. Today, competitive options are offering 4.5% to 5% on 12-month deposits with major institutions.

For retirees living off cash savings, or for investors sitting on equity while they wait for the right opportunity, higher rates represent genuine income. The trade-off, of course, is that the same elevated rates are compressing asset values and borrowing capacity elsewhere.

The broader point: where you sit on the borrower-versus-saver spectrum determines whether rising rates help or hurt you.

Here is a practical decision framework, whether you are protecting your home loan or managing an investment portfolio.

Step 1: Stress-test your position. Ask your broker to run your repayments at 6%, 6.5%, and 7%. If the numbers are uncomfortable, you need a plan before rates move – not after.

Step 2: Consider a split loan. Fixing your entire loan is a bet on rate direction that rarely pays off cleanly. Splitting – say, 60% fixed and 40% variable – gives you repayment certainty on part of your loan while keeping an offset account active on the variable portion. You reduce risk without surrendering flexibility.

Step 3: Build a cash flow buffer. If you own investment properties, your buffer between rental income and loan repayments should be wide enough to absorb at least a 1% rate rise without pushing you into crisis. If it is not, refinancing or restructuring before you are forced to is far better than scrambling under pressure.

Step 4: Act sooner rather than later on portfolio expansion. With the DTI cap in place, if you have plans to add properties, the conditions for doing so are becoming more restrictive. Acting with good advice now beats waiting for certainty that may never come.

Our guide on how interest rates affect property investment strategies explores this decision framework in detail.

Rising rates create real pressure. For variable rate borrowers, investors running lean cash flow, and households facing the fixed-rate rollover, the impact of rising interest rates on consumers is not theoretical – it is monthly. But the households and investors who will come through this period in the strongest position are those who act before they have to, not after.

Stress-test your loan. Review your structure. Understand your DTI position. And if you are not sure where you stand, a conversation with an experienced mortgage broker is the most valuable hour you can spend right now.

Book a mortgage review call today and find out exactly where your loan stands – and what to do about it.

Why are interest rates still rising in 2026?

The RBA raises rates to slow inflation by making borrowing more expensive and reducing consumer spending. Even as some inflation pressures ease, the board remains cautious about cutting too early – doing so risks reigniting price growth before it is sustainably under control. Interest rate predictions for 2026 remain mixed, which is why understanding your own position matters more than waiting for certainty.

How much more will my mortgage cost if interest rates keep rising?

On a $600,000 loan over 30 years, each 0.5% increase adds approximately $190 per month in repayments. Moving from 5.5% to 7% would cost an additional $587 per month, or nearly $7,000 per year. This is why stress-testing how rising interest rates affect your mortgage is an essential step to take right now, not when rates have already moved.

Who benefits from rising interest rates in Australia?

Savers benefit most directly – particularly retirees and investors holding cash or term deposits – as returns on savings accounts and fixed-term deposits have risen to levels not seen since before 2010. Those without significant debt, or with assets that generate income rather than require borrowing, are also relatively insulated from the impact of rising interest rates on consumers.

What is a debt-to-income cap and how does it affect my borrowing capacity?

A debt-to-income (DTI) cap limits how much total debt a lender can approve relative to your gross income, including all existing loans. Australia’s DTI cap, introduced in 2026, constrains how much investors and upgraders can borrow regardless of their capacity to service the loan. In practical terms, a combined household income of $120,000 limits total borrowing to around $1.44 million across all debts. If your portfolio plans run up against this cap, reviewing your borrowing structure now with an experienced broker is the smartest move you can make.

If you have a variable rate mortgage right now, you already feel it. Each time the Reserve Bank of Australia moves the cash rate, your...

Consolidating credit card and personal debt into your home loan can genuinely reduce your monthly repayments - sometimes by hundreds of dollars -...