What Do the 2026 Budget Tax Changes Mean for Your Property Investment Strategy in Australia?

Australia's 2026 Federal Budget has delivered the most significant tax reform for property investors in more than 25 years, reshaping the rules...

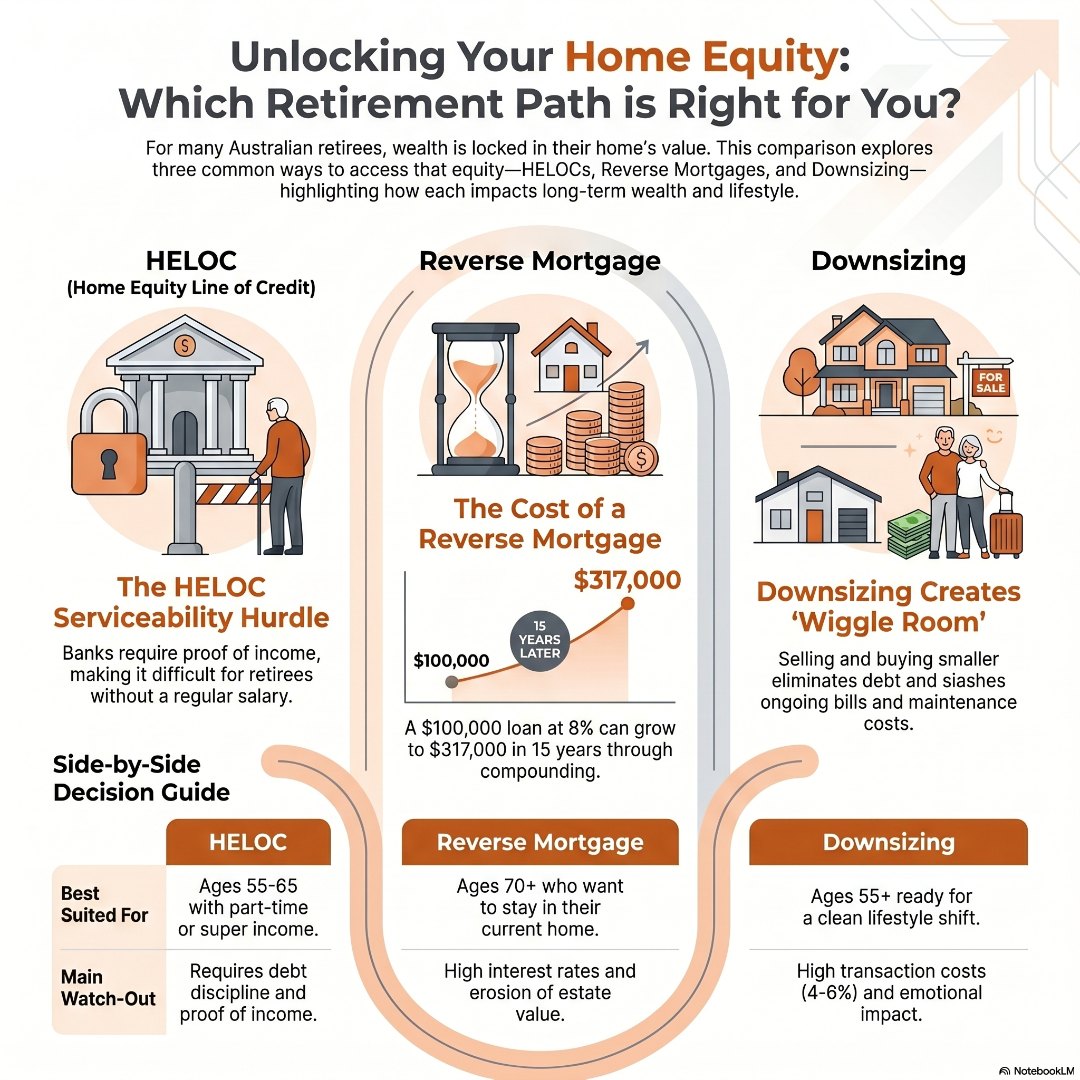

If you have spent decades paying down your home and watching its value climb, you are sitting on one of the most powerful financial assets in Australia. But when retirement approaches and cash flow tightens, that wealth can feel frustratingly locked away. The question most homeowners reach eventually is this: how do I actually access it? The three most common answers are a HELOC (home equity line of credit), a reverse mortgage, or simply downsizing. Each is a completely different beast, and choosing the wrong one can cost you tens of thousands of dollars – or worse, your home. Understanding the honest differences between a HELOC vs reverse mortgage and downsizing is the first step toward making the right call for your situation.

A home equity line of credit (HELOC) is a revolving credit facility secured against the equity in your property. You are approved for a maximum limit and only pay interest on what you actually draw down. If rates drop, you can refinance. On paper, it is one of the most flexible tools available.

The catch? Banks still need to verify your ability to service the debt. If you are fully retired and relying on superannuation or the Age Pension, proving sufficient income to satisfy standard lender serviceability requirements can be very difficult. This is the single biggest hurdle for a HELOC for retirees with no income – and it stops many applicants before they even get started.

For retirees who do qualify, a HELOC can work well for specific, purposeful spending – a planned renovation to make the home more liveable in older age, or bridging finance while transitioning between assets. What it does not suit is ongoing general living expenses. It is easy to keep drawing down without a clear repayment plan, and before long the debt level creates real financial stress.

A reverse mortgage is designed specifically for older Australians – typically those over 60 – who want to unlock the equity in their home without selling and without making regular repayments during their lifetime. Instead, the interest compounds and the loan balance grows over time. When you eventually sell, move into aged care, or pass away, the lender is repaid from the proceeds of the property.

The appeal is real. You stay in your home, receive either a lump sum or ongoing payments, and there is no monthly repayment obligation. For someone in their mid-70s whose health makes downsizing impractical, a reverse mortgage can be genuinely valuable.

But understanding the cost of a reverse mortgage vs a HELOC is essential before signing anything. Reverse mortgages typically carry higher interest rates than standard home loans – often 1% to 2% above a regular variable rate. Because interest compounds without repayment, the loan balance grows significantly over time. A $100,000 drawdown at 8% compounding interest left untouched for 15 years can grow to over $317,000. That is money that comes directly out of your estate.

Fees are also higher. Establishment costs, ongoing management fees, and valuation charges all add up. Under Australian law, a “no negative equity guarantee” means you can never owe more than your home is worth – but you can certainly owe a large portion of it.

Downsizing – selling your current home and buying something smaller or less expensive – is what often gets dismissed as the “emotional” option. People resist it because they have a connection to the family home, the suburb, the neighbours. That is entirely understandable. But financially, it is frequently the most decisive move available and one of the strongest alternatives to a reverse mortgage for equity-rich homeowners.

When you downsize from a $1.2 million home to a $750,000 apartment or unit, you are not just pocketing $450,000 (less transaction costs and stamp duty). You are also eliminating or dramatically reducing your ongoing mortgage, cutting council rates, slashing utility bills, and removing the maintenance overhead that older, larger homes inevitably carry.

That freed capital can be invested to generate income, top up superannuation under the downsizer contribution rules (currently available to Australians aged 55 and over), or kept in a high-interest offset account as a liquid retirement buffer. You can learn more about how to build a retirement income strategy around property in our guide on how to build a successful 3-property retirement plan.

The main drawback is transaction cost. In most states, selling and buying again carries stamp duty, agent commissions, conveyancing fees, and moving costs. Budget for 4% to 6% of the total transaction value. And if you love your home and location, the emotional cost is real.

I know this tension personally. When my parents were ready to make their move, my sister and I visited thirty – yes, thirty – retirement villages before we found the right one. It was not a simple property decision. It was a life decision. What made it easier was that we had already done the financial work: the property was sold at the right time, and after costs, what remained gave my dad what he proudly called his “wiggle room.” That phrase has stayed with me. Because that is exactly what downsizing delivers when it is executed well – not just freed capital on a spreadsheet, but genuine breathing room. The peace of mind that comes from knowing the money is there, accessible, not locked in a loan structure that compounds quietly in the background while you sleep. My dad did not call it an investment return or an equity release event. He called it wiggle room. And for a man who had worked hard all his life, that was everything.

| Option | Best suited to | Watch out for | Who this suits best |

| HELOC | Retirees with proven income, short-term specific purpose | Income requirements, debt discipline | Retirees aged 55-65 with part-time or super income and a clear spending plan |

| Reverse Mortgage | Older Australians (60+), fixed assets, health limits mobility | Compounding interest, estate impact | Homeowners aged 70+ who want to stay put and have limited other assets |

| Downsizing | Equity-rich homeowners ready for a lifestyle shift | Transaction costs, emotional adjustment | Homeowners aged 55+ with a flexible lifestyle and strong equity position |

None of these options exists in a vacuum. The best choice depends on variables unique to you – your age, your health, whether you have a partner, your income sources in retirement, what you plan to do with the cash, and how much equity you want to preserve for your estate.

For example, if you are 62, mortgage-free, and need $80,000 to renovate and age in place, a reverse mortgage may be entirely reasonable. If you are 58 with a part-time consulting income and a specific investment plan, a HELOC could be structured to work. If you are 65, the kids have grown, and you no longer need the extra space, downsizing may deliver the cleanest outcome by a wide margin.

This is why the decision warrants a conversation with someone who can see your complete picture – not just the loan side, but your retirement income, super balance, aged care considerations, and estate goals. Our guide on opening opportunities with your home equity explains how lenders assess your usable equity and the structures available to release it.

It is also worth understanding that interest rate movements affect these strategies very differently. A rising rate environment makes the compounding cost of a reverse mortgage significantly more damaging, while a HELOC becomes harder to service. Downsizing remains largely rate-neutral. For more context on how rate changes affect borrowing decisions, read our article on how RBA rate changes directly impact your mortgage.

There is no single right answer to the HELOC vs reverse mortgage or downsizing question. What there is, however, is a right answer for your situation – and getting to it requires an honest assessment of your numbers, your goals, and your timeline.

If you want to stay in your home and have limited income, a reverse mortgage may be your most practical option – but go in with eyes open about the compounding interest. If you have verifiable income and a disciplined plan, a HELOC offers genuine flexibility. If you are ready to make a lifestyle change and want to eliminate financial complexity in retirement, downsizing is often the cleanest path forward.

The worst outcome is drifting into a decision because it seemed easier at the time. These are significant, sometimes irreversible choices that deserve proper analysis.

Book a mortgage review call today and let us walk you through all three scenarios against your real numbers. Whether you are considering borrowing against your equity or thinking about a move, getting the strategy right from the start can save you hundreds of thousands of dollars over the long term.

Should I downsize or get a reverse mortgage to fund my retirement?

The answer depends on how attached you are to staying in your current home and how important it is to preserve equity for your estate. Downsizing delivers clean, debt-free capital and reduces ongoing costs, making it the stronger long-term option for many retirees. A reverse mortgage is better suited to those who want to stay put but need cash flow – provided they understand the compounding interest will reduce what remains for beneficiaries over time.

Can I get a HELOC in retirement if I have no regular income?

This is the most common stumbling block for retirees considering a HELOC. Most lenders require proof of income to satisfy serviceability requirements. Super drawdowns and some government pension payments can sometimes count, but it varies by lender. A mortgage broker who specialises in retirement lending can assess your specific income sources against current lender policies to find out what is actually available to you.

How much does a reverse mortgage really cost compared to a HELOC?

A reverse mortgage typically carries an interest rate 1% to 2% above standard variable rates, with compounding interest growing the debt each year without repayments. A HELOC is usually cheaper in interest rate terms but requires ongoing repayments. The real cost difference shows over time – a $100,000 reverse mortgage at 8% over 15 years grows to over $317,000, while a HELOC on the same amount may cost around $8,000 per year in interest with the principal remaining unchanged if you choose to service interest only.

Is downsizing in retirement tax-free in Australia?

Your principal place of residence is exempt from capital gains tax (CGT) in Australia, so selling your home and downsizing does not trigger a CGT event. You also have the opportunity to make a “downsizer contribution” of up to $300,000 per person ($600,000 for a couple) into superannuation from the proceeds if you are aged 55 or over and meet the eligibility criteria – a significant tax-advantaged benefit that many retirees underutilise.

Australia's 2026 Federal Budget has delivered the most significant tax reform for property investors in more than 25 years, reshaping the rules...

Regional property markets are outperforming capital cities across Australia right now, with dwelling values rising 3.3% over the three months to...