Is Investor Activity Set to Fall?

Australia's property investors are facing a double headwind in 2026 - and the latest lending data confirms the retreat has already begun....

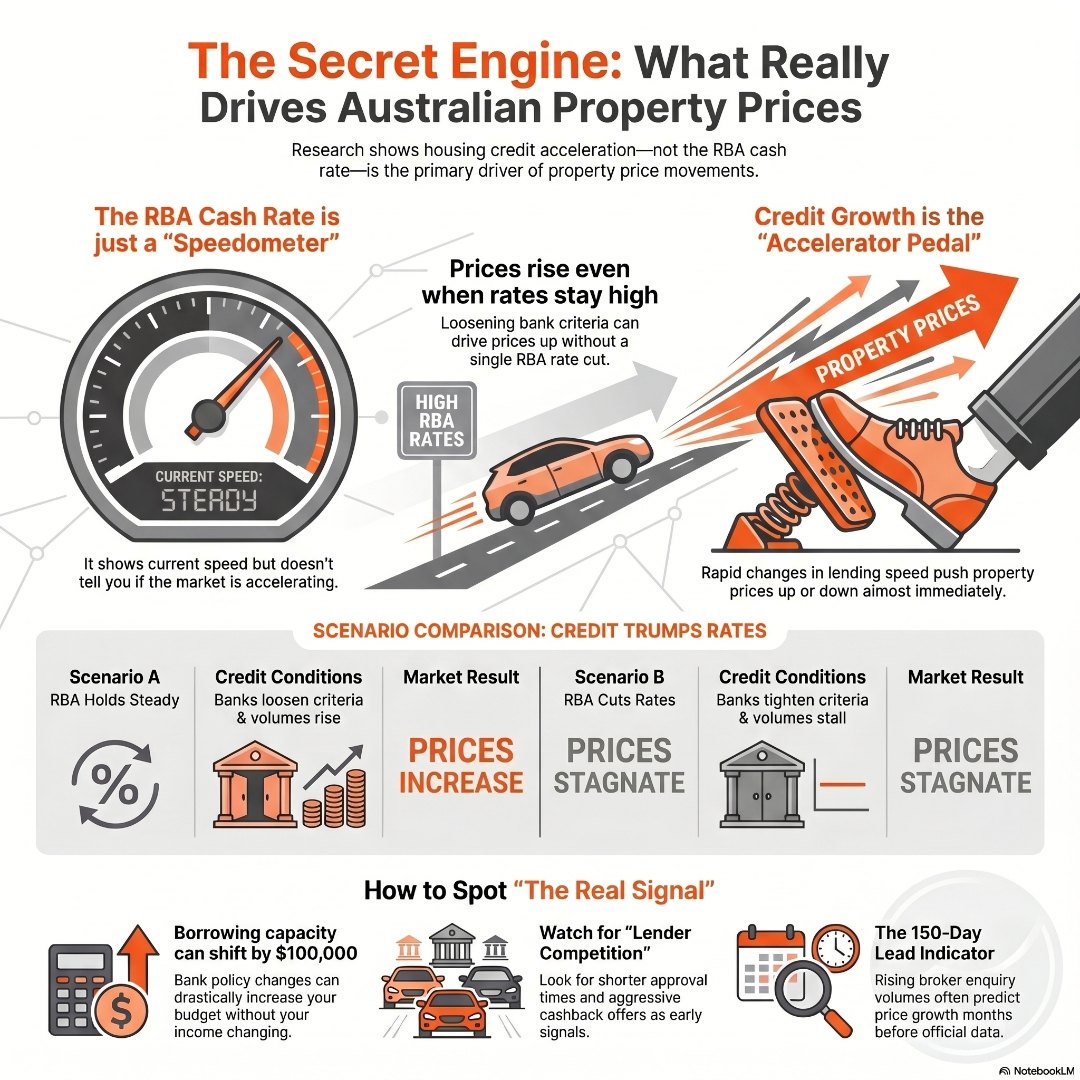

Every six weeks or so, a national ritual plays out. Australians gather around their phones and televisions waiting for the RBA board decision. Financial commentators fill the airwaves. Mortgage holders brace. Property investors hold their breath.

It is completely understandable. The RBA cash rate is the most visible lever in the system. It affects variable mortgage repayments directly, it is announced publicly, and it generates enormous media coverage. Understanding how RBA rate changes directly impact your mortgage is genuinely important for every borrower.

But here is the problem. Watching the RBA as your primary market timing signal is a bit like watching a car’s speedometer while ignoring whether the driver is pressing the accelerator or the brake. The speed reading matters – but it is the change in pressure that actually moves you in your seat.

Property investors who rely solely on RBA announcements to time their decisions are missing the more powerful signal entirely.

Research modelling over 7,200 Australian suburban markets across more than two decades points to a consistent and striking finding: housing credit growth is the single dominant driver of national property price movements.

But the key insight is not how much lending is happening. It is how fast that lending is growing.

Think of it like a car accelerating. It is not the speed that pushes you back in your seat – it is the sudden change in speed. When banks start loosening their credit conditions and loan volumes begin climbing quickly, property prices respond almost immediately. When that credit growth plateaus or contracts, the market feels it just as swiftly.

This is why you can have periods where interest rates are still relatively low but prices are flat. The credit acceleration has already normalised. The engine is still running, but nobody is pressing the accelerator harder.

Conversely, this is also why prices can rise even when the RBA has not moved the cash rate at all. If banks are actively competing for business, reducing friction in their lending processes, easing their serviceability buffers, or increasing the volume of approvals, they are effectively pumping fuel into the market regardless of what the RBA has done.

To bring this to life, consider two different property market scenarios that most Australians have lived through.

Scenario A – Lending loosens without a rate cut: The RBA holds rates steady for six months. But during that same period, three major banks drop their interest rate floors for investor loans. Approval times shorten. Competition among lenders intensifies. Brokers start reporting that applications which would have been declined three months ago are now sailing through. Monthly mortgage volumes tick up 8%, then 12%, then 15% year-on-year.

Scenario B – A rate cut without credit acceleration: The RBA cuts the cash rate by 0.25%. Mortgage holders cheer. But lending criteria tighten simultaneously. Banks lift serviceability buffers. Fewer applicants qualify. Approval volumes stagnate.

In Scenario A, prices respond upward – even without an RBA cut. In Scenario B, a rate cut fails to stimulate the market because credit acceleration never actually occurred.

This explains a phenomenon that confuses many buyers: why do prices sometimes keep rising even when interest rates are high? The answer lies in bank lending conditions, not just the headline rate. And it explains why trying to time the market based solely on RBA announcements consistently leads to frustration.

Most people understand the basic relationship. Lower rates mean cheaper borrowing, which means more buyers can enter the market, which drives prices up. And broadly speaking, that is true.

But the relationship between interest rates and house prices in Australia is far from a simple straight line. It is shaped by credit availability, lender appetite, borrower serviceability, and – critically – the rate of change, not the absolute level.

Consider what happened in the post-2020 period. Interest rates were historically low. But prices did not simply drift upward in a slow, steady climb. They exploded. Why? Because credit was not just cheap – it was accelerating rapidly. Banks were loosening criteria, approval volumes were surging, and borrowing capacity was expanding faster than most people realised.

Then, as the rate-hiking cycle began from 2022, prices fell sharply – not just because rates were higher, but because credit decelerated almost overnight. Lending volumes dropped, approval rates tightened, and borrowing capacity contracted. The acceleration had reversed.

Understanding this mechanism is what separates sophisticated investors from those who are always waiting for the “right time” that never quite arrives. For a deeper look at how the property cycle behaves across different market conditions, our guide on timing the market and the property cycle provides useful context for putting credit signals in perspective.

If housing credit acceleration is the key signal, then the most important question for any buyer or investor is not “What will the RBA do next month?” It is “What are banks doing right now with their lending criteria – and what does that mean for my borrowing capacity?”

When banks are actively competing for your business, the practical signs show up quickly:

On the flip side, when credit is contracting, even a borrower with a stable income and a clean credit history can find themselves assessed differently than six months prior. Lender policy changes, credit card limits assessed against you, and changes to how rental income is counted can all reduce your effective borrowing power significantly.

This is why working with a broker who monitors these conditions actively is so different from simply applying to your own bank. The right lender at the right moment in the credit cycle can make a material difference to what you can borrow and what you can buy. If you want to understand how to maximise your position in the current environment, our article on strategies to improve your borrowing capacity for property investment lays out the practical steps in detail.

So what should you actually watch? Here are the signals worth tracking alongside – or sometimes ahead of – RBA announcements:

Monthly credit growth figures. The Australian Bureau of Statistics and the Reserve Bank publish housing credit data monthly. When the month-on-month growth rate begins accelerating – not just staying positive, but growing faster than before – that is an early signal.

Lender policy changes. These are less visible but often more impactful. When major banks begin easing their serviceability buffers, removing investor surcharges, or competing for business in new ways, credit conditions are loosening. A mortgage broker with access to multiple lenders will notice this before it appears in any news headline.

Approval volumes and turnaround times. When brokers and lenders start reporting shorter approval windows and higher conversion rates, loan volumes are building. That is credit acceleration beginning to form.

Competition among lenders. When banks start chasing customers with cashback offers, rate discounts, or relaxed income requirements, they are competing for volume. That competition is itself a sign of loosening conditions.

None of these signals require you to be a data analyst. What they require is access to someone who is watching them in real time and translating them into decisions you can act on. And that is exactly what I see play out inside our business, month after month.

After more than 20 years running a mortgage broking business, I have noticed something that no data report has ever told me first. Long before any price movement shows up in a CoreLogic report or a news headline, I can already feel it in the enquiries landing in our inbox. There is a consistent pattern I have tracked over the years: from the moment a borrower first contacts us to ask about their borrowing capacity, to the day they actually make an offer on a property, it is typically around 150 days. What that means in practice is that when our enquiry volumes start climbing – when more people are beginning that 150-day journey – I know, months before the data confirms it, that buying activity is about to accelerate. No RBA meeting required. I have watched this play out repeatedly across different market cycles, and it remains one of the clearest early signals I know. The flipside is equally true. When enquiries slow, or when the nature of the calls shifts from “how much can I borrow?” to “will the bank still approve me?” – that is a credit contraction starting to form, often before it registers anywhere publicly. This is what brokers who are paying close attention can see that most buyers simply cannot. It is not magic. It is proximity to the data, and the experience to know what it means.

The question most Australians are asking – “What will the RBA do?” – is the wrong one, or at least an incomplete one. The research is clear: what drives property prices in Australia is the acceleration of housing credit. When banks loosen their criteria and lending volumes surge, prices follow. When credit contracts, prices soften – regardless of what the cash rate is doing.

For investors and buyers, this shifts the strategy. Instead of waiting for a rate cut that may or may not materialise, the more productive question is: “Are credit conditions tightening or loosening right now, and is my borrowing capacity positioned to take advantage?”

Answering that question well is exactly what working with the right mortgage broker makes possible. And now, through the ICM Hub our clients get access to insights and tools that translate this kind of data into decisions – giving you the unfair advantage that used to only be available to institutional investors. Old-school service, cutting-edge knowledge.

If you want to know where you stand and what the current lending environment means for your next property decision, Book a mortgage review call today – or explore the tools available Investors Choice Mortgages Hub to get started.

What actually drives property prices in Australia?

Research across thousands of Australian suburbs over more than two decades consistently identifies housing credit growth – specifically the acceleration of bank lending – as the dominant driver of property price movements. The RBA cash rate plays a role, but it is the rate at which lending volumes are growing or contracting that produces the most immediate and measurable price effects.

Does the RBA actually control house prices in Australia?

Not directly, and not as completely as most people believe. The RBA cash rate influences the cost of borrowing, which affects how much buyers can access. But banks have significant independent discretion over their lending criteria, serviceability buffers, and lending appetites. When banks tighten or loosen those standards independently of the RBA, property prices respond – sometimes faster than any RBA move would produce.

Why are house prices rising even when interest rates are high?

Prices can rise during high-rate periods if bank lending conditions are loosening simultaneously. If approval rates are climbing, lender competition is increasing, and credit volumes are accelerating, that surge in accessible capital pushes prices upward – even if the underlying rate remains elevated. The speed of credit growth matters more than the absolute level of rates.

When is the best time to buy property in Australia based on credit conditions?

The optimal window for buyers tends to occur when credit conditions are just beginning to loosen – when banks are starting to compete more aggressively for new business, before that competition has fully pushed prices upward. Monitoring lender policy changes, monthly credit growth figures, and approval trend data gives you a forward-looking indicator that most buyers are not watching.

How does housing credit growth affect my personal borrowing capacity for an investment property?

When banks ease their lending criteria – reducing serviceability buffers, reassessing how rental income is counted, or competing for investor volumes – your assessed borrowing capacity can increase materially, sometimes by $50,000 to $100,000 or more, without any change in your income. Conversely, when credit contracts, the same income and assets may support significantly less borrowing. Working with a broker who tracks these conditions in real time helps ensure you are assessed at your strongest possible position.

All market data and research referenced in these articles is sourced from HTAG Analytics’ April 2026 research report: “A Forced Autoregressive Model of Australian Residential Property Price Dynamics: Credit, Migration, Monetary Policy, and Supply Interactions 2003–2026” by Alex Fedoseev and Dr. Matija Djolic, HTAG Analytics.

Investors Choice Mortgages acknowledges HTAG Analytics as an industry-leading source of Australian property market intelligence.

Australia's property investors are facing a double headwind in 2026 - and the latest lending data confirms the retreat has already begun....

Australia's 2026 Federal Budget has delivered the most significant tax reform for property investors in more than 25 years, reshaping the rules...