The 5 Forces Quietly Controlling Australian Property Prices Right Now

Most commentary on Australian property prices zeroes in on one thing: interest rates. But reducing a complex, multi-trillion-dollar market to a...

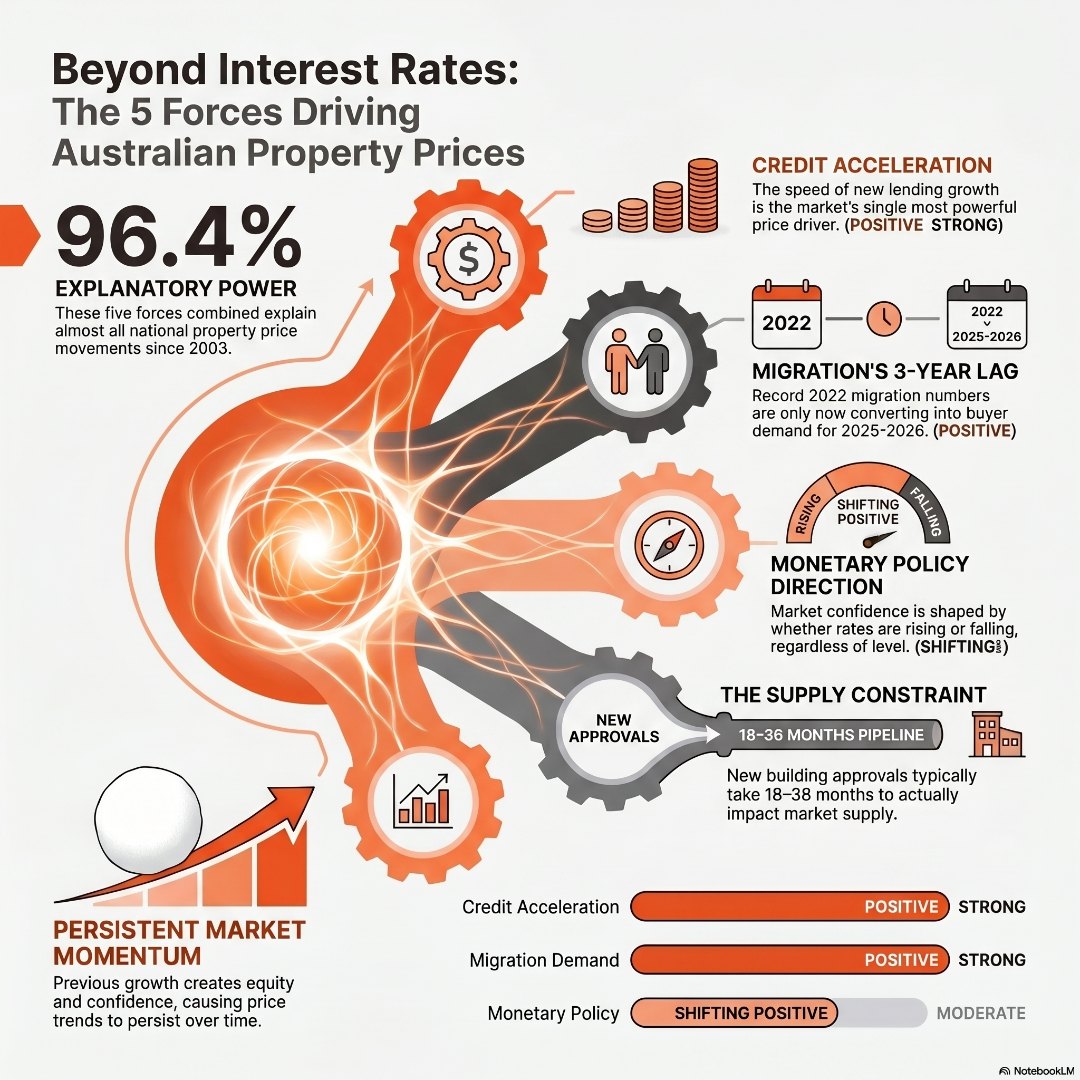

Most commentary on Australian property prices zeroes in on one thing: interest rates. But reducing a complex, multi-trillion-dollar market to a single variable is like diagnosing a patient’s health by only checking their temperature. Research by HTAG Analytics, which has tracked over 7,200 suburban markets since 2003, identifies five macroeconomic forces that together explain 96.4% of the variation in national property price growth. Understanding what is driving Australian property prices – and where each force currently sits – transforms the way you read the market and make decisions.

Picture a Monday morning in 2025. A finance journalist warns on radio that RBA rate cuts will ignite a housing frenzy. The economist after them predicts a surge in new apartment approvals will dampen prices within 12 months. Both are correct in isolation. Both are incomplete.

The problem is not a lack of opinions on Australian property prices. It is an abundance of single-variable analysis dressed up as insight. Rates go down and people assume prices go up. Building approvals rise and commentators declare the shortage is solved. Migration hits the headlines and everyone blames population growth for affordability pain.

I’ve been running Q&A sessions on property investing, renovation, and finance for over a decade – every single month, without fail. And maybe once every three months, right at the end of a session, someone would say: “But I was talking to a taxi driver on the way here and he said I shouldn’t invest in Williamstown.” My business partner John and I would catch each other’s eye across the room. We called it the taxi driver problem. Because here’s the thing – the taxi driver wasn’t wrong exactly. He might have had a real experience, a genuine opinion. But a single story, from a single source, is not a framework. It is noise dressed as wisdom. And it costs people. I’ve watched buyers freeze, stall, or lurch in the wrong direction because one voice – whether it was a taxi driver, a breakfast radio economist, or a worried parent – carried more weight in that moment than two decades of data.

Each of these forces is real. None of them is sufficient on its own.

The HTAG Analytics research framework cuts through this noise by quantifying how much each force contributes to price outcomes – measured across more than two decades of real market data. The result is a model that explains nearly all price movement, and a decision framework that serious buyers and investors can actually use.

Credit acceleration refers to the rate at which mortgage lending is growing across the economy. Not the level of interest rates. Not whether your bank is offering a fixed rate of 5.89% or 6.14%. The speed at which new lending is expanding.

When credit accelerates, more buyers enter the market with more purchasing power. Demand lifts. Prices respond. When credit contracts – as it did sharply in 2008 and again briefly in 2019 – the market pulls back even when rates are relatively low.

Right now, conditions for credit acceleration are supportive. The RBA cutting cycle has expanded borrowing capacity for most households. Lenders are competing more aggressively for business. The pipeline of pre-approvals is building. This is the force with the single greatest explanatory power in the HTAG model, and it is currently pointing in a positive direction.

The practical implication: watching what the RBA does is less important than watching what lenders actually do in response. Credit conditions on the ground tell you more than the cash rate headline.

Here is the insight that most property market commentary overlooks entirely. Migration does not translate into housing demand the moment a new arrival steps off a plane. It takes roughly three years.

Newly arrived migrants typically rent first. They settle in, assess their finances, understand the local market, accumulate savings, and build credit history. The conversion from renter to buyer generally happens around the two-to-three year mark. That means the housing demand being felt in 2025 and 2026 is not driven by today’s migration intake. It is driven by the record numbers who arrived in 2022.

Australia’s 2022 net overseas migration was among the highest on record. That cohort is now moving through the property market in large numbers. Understanding the impact of migration on house prices in Australia and this three-year lag effect is one of the most powerful – and least discussed – forward indicators available to buyers and investors.

This force is currently strongly positive and will remain active through at least 2026.

Everyone talks about interest rates. Fewer people talk about them correctly.

The HTAG research distinguishes between the level of rates and the direction of change. A market with rates at 6% and falling behaves very differently from a market with rates at 4% and rising. Psychology and confidence are shaped not by where rates sit today, but by where they appear to be heading.

The RBA began its cutting cycle in early 2025. This directional shift from tightening to easing has material effects on consumer confidence, buyer activity, and lender risk appetite. However, as explored in detail in our analysis of why the RBA rate cut has not triggered a property market boom yet, the full effect of rate changes plays out over years, not months.

This is a transitional force right now – moving from headwind to tailwind – but the full impact is still unfolding. Waiting for rate cuts to produce an obvious market surge before acting may mean waiting until the opportunity has already passed.

Supply and demand is economics at its most basic. But the relationship between building approvals and Australian property prices is slower and less predictable than most buyers expect.

When building approvals rise, new dwellings typically take 18 to 36 months to reach completion. A surge in approvals today signals supply arriving in 2026 or 2027 – not immediately. In the meantime, the undersupply that has characterised most major Australian capital cities since 2020 continues to provide a floor under prices.

Current building approvals suggest meaningful new supply will enter the market in 2026 and 2027. In specific markets where high-density approvals are concentrated – parts of inner Melbourne and south-east Queensland – supply may moderate price growth more quickly. In tightly held suburban markets and regional hubs, the constraint remains acute.

Understanding what drives property prices in Australia at the suburb level – rather than accepting national averages – is essential, because this force operates very unevenly across markets.

The fifth force is the most counterintuitive for buyers who have been taught to fear markets that have already risen.

Market momentum refers to the well-documented tendency for property price growth to persist from one year to the next. Markets that outperformed last year are statistically more likely to outperform this year – unless one of the other four forces turns sharply negative.

The mechanism is straightforward. Rising prices create equity. Equity creates confidence. Confidence unlocks new buyers, investors, and upgraders. Activity generates further demand. The cycle reinforces itself until an external shock – a credit contraction, a supply surge, or a sharp rate rise – interrupts the sequence.

Australian capital cities have shown positive momentum through late 2024 and into 2025. Unless credit conditions tighten, migration reverses, or supply floods the market simultaneously, the base case is for this momentum to continue in the near term. Momentum is not a guarantee – but it is a measurable, quantifiable force that investors should respect rather than dismiss.

Reading all five forces together is what separates strategic property decisions from guesswork.

| Force | Current Direction | Strength |

| Credit Acceleration | Positive | Strong |

| Migration Demand | Positive | Strong |

| Monetary Policy | Shifting Positive | Moderate |

| Residential Supply | Neutral (building) | Moderate |

| Market Momentum | Positive | Moderate |

Three forces are currently positive and two are neutral-to-transitional. This broadly explains the moderate-growth environment across most Australian markets in 2025: not a repeat of the 2021 boom, where credit, rates, and supply all aligned strongly at once, but not a correction either.

Understanding the five forces does not mean timing the market perfectly. It means making decisions with a structural framework rather than reacting to the most recent headline.

For buyers considering their first or next investment property, the forces point to a window where credit conditions are supportive, migration demand is active, and momentum has not reversed. The supply constraint in most markets has not yet been resolved. Monetary policy is moving in a favourable direction, even if incrementally.

To build a profitable investment property portfolio in this environment, the key question is not “should I buy?” but “which market is seeing the most favourable combination of these five forces right now?”

That question requires suburb-level analysis, not national averages. It requires understanding your borrowing capacity in the context of an easing credit cycle. And it requires guidance from someone who is reading the same data – not just relaying the latest interest rate news.

The Investors Choice Mortgages Hub is built exactly for this – giving our clients and curious community access to broker expertise grounded in data like this, with the kind of personalised attention that the big banks simply do not offer anymore. Because in today’s market, information without guidance is just noise.

What are the five forces that control Australian property prices?

The five macroeconomic forces are credit acceleration, migration demand, monetary policy, residential supply, and market momentum. Research tracking over 7,200 Australian suburban markets since 2003 shows these forces together explain 96.4% of the variation in national property price growth. Understanding each force – and their combined direction – gives buyers and investors a far clearer picture than focusing on any single variable.

How do interest rates affect Australian house prices?

Interest rates influence property prices primarily through their effect on borrowing capacity and consumer confidence, but the direction of rate movement matters more than the level. A market with rates at 6% and falling behaves very differently from one with rates at 4% and rising. The RBA cutting cycle that began in 2025 is shifting monetary policy from a headwind to a tailwind for property prices, but the full effect typically unfolds over years rather than months.

How does migration affect Australian property prices?

Migration affects Australian property prices with approximately a three-year lag. New arrivals typically rent first, then transition to buying after roughly two to three years. This means the record migration intake of 2022 is directly converting into buyer demand during 2025 and 2026, making migration-driven demand one of the most clearly positive forces currently active in the market.

Will Australian property prices keep rising in 2026?

Based on the five-force framework, the outlook for 2026 is for continued moderate growth in most markets. Credit conditions are supportive, migration-driven demand is actively converting to purchases, monetary policy is easing, and market momentum is positive. The main moderating factor is residential supply, with new dwelling completions expected to begin increasing from 2026 to 2027, which may temper price growth in specific high-density markets more than others.

Most commentary on Australian property prices zeroes in on one thing: interest rates. But reducing a complex, multi-trillion-dollar market to a...

National property data gives you a number. What it rarely gives you is the truth about a specific suburb. For most Australian investors...