Are Mortgage Calculators Accurate?

https://vimeo.com/1186811137/1b4b319ef3 Most Australians start their property journey on an online mortgage calculator. The maths it returns...

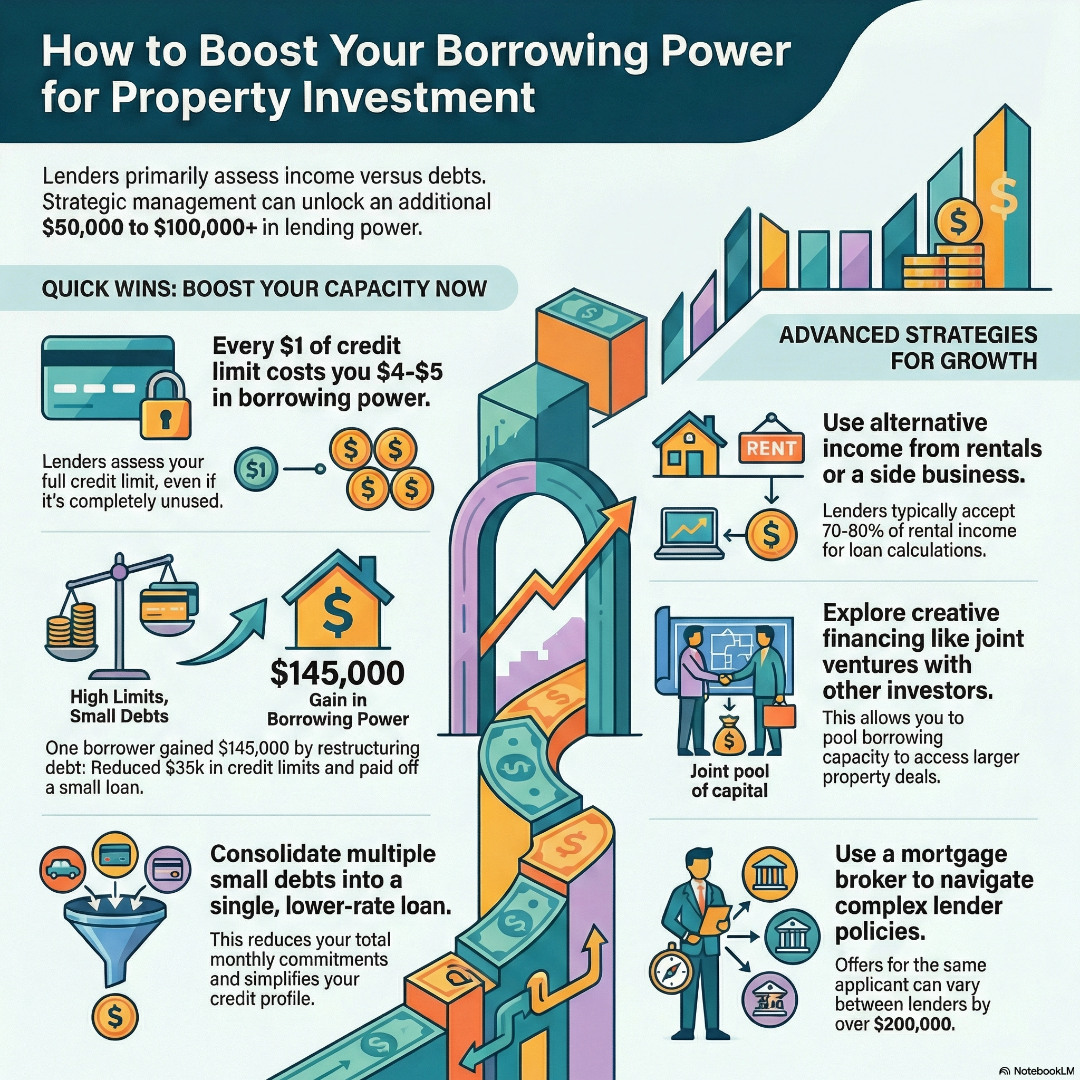

Hitting your borrowing capacity can feel like watching your property investment dreams slip away, but there are multiple proven strategies you can implement to potentially increase your lending power. Most borrowing capacity is calculated on two fundamental factors: what you earn versus what you owe. While increasing income or reducing debt are the obvious starting points, savvy investors know there are creative approaches that can unlock significantly more lending potential, sometimes adding $50,000 to $100,000 to your borrowing power through strategic financial restructuring.

The key lies in understanding exactly how lenders assess your application and then systematically addressing each component that impacts their decision. Many property investors discover they’re sitting on untapped borrowing capacity simply because lender policies have evolved, their personal circumstances have improved, or they haven’t optimised their existing debt structure.

One of the most overlooked factors destroying borrowing capacity is unused credit card limits. Lenders don’t care if you never use that $20,000 credit card – they assess your borrowing capacity as if you’re spending the full limit every month. This means a single high-limit credit card could be costing you $80,000 to $100,000 in borrowing power.

Sarah, a 42-year-old marketing manager, discovered this costly mistake when preparing for her second investment property. Despite earning $95,000 annually, her borrowing capacity was limited by three credit cards totaling $35,000 in unused limits. By reducing these limits to $5,000 total and paying off a small personal loan, she increased her borrowing capacity by $145,000 – enough to secure the investment property she’d been targeting.

The mathematics are stark: lenders typically reduce your borrowing capacity by $4-5 for every $1 of credit limit because they calculate repayments at the minimum 2-3% monthly requirement. A $10,000 credit card limit translates to approximately $300 monthly in potential repayments, which directly reduces how much mortgage repayment you can afford.

While paying off high-interest debt improves borrowing capacity, strategic restructuring can be even more powerful. Consider consolidating multiple smaller debts into a single, lower-rate personal loan with a shorter term. This approach often reduces your total monthly commitment while simplifying your credit profile.

Investment-savvy borrowers also explore debt recycling strategies, where existing home equity is used to pay down non-deductible debt, then redrawn for investment purposes. This maintains borrowing capacity while improving tax efficiency – though this strategy requires careful planning and professional guidance.

Some property investors benefit from switching from interest-only to principal-and-interest repayments on existing investment loans, demonstrating improved serviceability to lenders. While this increases short-term cash flow requirements, it can unlock capacity for additional borrowing.

Mortgage markets are constantly evolving, with lenders regularly adjusting their assessment criteria, interest rate buffers, and borrowing calculators. What limited your borrowing capacity 12 months ago might no longer be relevant today.

Major banks have periodically increased their borrowing calculations, particularly for borrowers with strong employment history and minimal dependents. Smaller lenders and non-bank institutions often have more flexible policies for property investors, especially those with existing portfolios.

Your credit score improvement can also unlock additional borrowing power. Credit scores above 750 often qualify for premium lending rates and higher borrowing multiples. If you’ve improved your credit score since your last application – perhaps by maintaining consistent repayments or reducing credit utilisation – you might qualify for significantly more favourable lending terms.

Traditional employment income isn’t the only way to demonstrate borrowing capacity. Lenders increasingly recognise diverse income streams, particularly for property investors building portfolios.

Rental income from existing properties typically contributes 70-80% of its value to borrowing capacity calculations. However, some lenders offer higher rental assessments for well-located properties with strong rental histories. Room-by-room rental strategies, where investors rent individual rooms or parking spaces separately, can significantly boost demonstrable rental income.

Side business income becomes assessable after two years of consistent earnings, with some lenders accepting business income after just one year for established professionals. Freelancing, consulting, or e-commerce businesses can provide the additional income verification needed for increased borrowing capacity.

When traditional borrowing reaches its limits, creative financing structures open new possibilities. Joint ventures with other investors allow you to leverage combined borrowing capacity and share both investment risk and returns.

I know firsthand how frustrating it is to reach that bank-imposed ceiling. I was already highly leveraged but saw a compelling opportunity I couldn’t ignore. It was at that point I realised the only way forward was to think completely outside the traditional box. I started exploring overseas models, specifically crowdfunding and pooling resources with others who had different strengths. By combining skills—one person bringing a deep understanding of renovation, another with high cash flow, and myself managing the project—we effectively pushed past the personal equity ceilings that the banks had set for me alone. It became clear that leveraging collective capacity, whether through formal joint ventures or creative skill-set pooling, is a powerful way to keep investing when your individual borrowing capacity is maxed out.

Some investors explore option contracts, where they secure future purchase rights without immediate large capital requirements. This strategy allows continued market participation while building additional borrowing capacity over time.

Sweat equity arrangements, where investors contribute labour or expertise instead of cash, can provide property investment opportunities without relying solely on borrowing capacity. Finding and renovating properties, managing developments, or providing specialised skills can create investment opportunities that traditional lending cannot support.

Navigating borrowing capacity optimisation requires understanding dozens of different lender policies, assessment criteria, and documentation requirements. Professional mortgage brokers access lenders unavailable directly to consumers and understand which lenders suit specific borrower profiles.

Different lenders assess identical applications differently, with some variations exceeding $200,000 in borrowing capacity for the same borrower. Specialist investment lending brokers understand how to present applications for maximum impact and can guide the timing of applications for optimal results.

Improving borrowing capacity requires systematic analysis of your current position, identification of optimisation opportunities, and strategic implementation of improvements. Start with the quickest wins – reducing credit card limits and paying down high-interest debt – before exploring more complex strategies like income diversification or alternative financing structures.

Remember that borrowing capacity is just one component of successful property investment. Sustainable cash flow, capital growth potential, and risk management remain crucial for long-term success. The goal isn’t simply to borrow more, but to borrow strategically for investments that build genuine wealth over time.

Consider reviewing your borrowing capacity annually, as your personal circumstances, market conditions, and lender policies continuously evolve. What seems impossible today might become achievable with the right strategy and professional guidance.

Maximising your borrowing capacity is an essential skill for serious property investors looking to build sustainable wealth. By understanding how lenders assess applications and strategically optimising your financial profile, you can potentially unlock tens or even hundreds of thousands in additional borrowing power. Whether through credit limit management, debt restructuring, income diversification, or alternative financing methods, there are multiple pathways to enhance your property investment capacity.

The most successful investors work closely with experienced mortgage brokers who understand the nuances of lender policies and can navigate the complexities of investment lending. By implementing these strategies systematically and reviewing your position regularly, you can continue expanding your property portfolio while maintaining financial stability and working toward long-term wealth creation.

Book a mortgage review call today to discover your true borrowing capacity and unlock the strategies that could add tens of thousands to your lending power for your next property investment.

How much can reducing credit card limits increase my borrowing capacity?

Reducing credit card limits typically increases borrowing capacity by $4-5 for every $1 of limit reduction. A $20,000 total limit reduction could increase your borrowing power by $80,000-$100,000, depending on your lender’s assessment criteria and your overall financial profile. This makes credit card limit reduction one of the fastest and easiest ways to boost your borrowing capacity without changing your income situation.

Will closing credit cards improve my borrowing capacity more than reducing limits?

Closing credit cards can provide slightly better results than limit reduction, but the difference is often minimal. Reducing limits to $1,000-$2,000 per card maintains some flexibility while achieving most of the borrowing capacity benefit. Complete closure eliminates any ongoing annual fees and removes temptation entirely. Consider keeping your oldest card with a low limit to maintain credit history length, which benefits your overall credit score.

How long after improving my credit score will lenders recognise the change?

Credit score improvements typically appear on credit reports within 30-60 days of positive changes. However, lenders may require 3-6 months of consistent good behaviour before offering their best rates and maximum borrowing capacity. Some lenders update their internal scoring models quarterly. If you’re planning to apply for investment property finance, start working on credit score improvements at least six months in advance for optimal results.

Can rental income from my existing investment property help me borrow more?

Most lenders assess rental income at 70-80% of its actual value when calculating borrowing capacity. Properties with strong rental histories, professional management, or above-market rents may qualify for higher assessments. Some specialist lenders offer up to 90% rental income recognition for well-located properties. To maximise this benefit, ensure your property manager provides detailed rental statements and consider having your property professionally revalued if you believe its value has increased significantly.

https://vimeo.com/1186811137/1b4b319ef3 Most Australians start their property journey on an online mortgage calculator. The maths it returns...

The instinct makes perfect sense. You see government targets for 1.2 million new homes, headlines about record building approvals, and your first...