How Can I Consolidate Debt by Refinancing?

What is refinancing to consolidate debt? Refinancing to consolidate debt is the process of using the equity in your home to pay off...

What is refinancing to consolidate debt? Refinancing to consolidate debt is the process of using the equity in your home to pay off multiple high-interest debts, such as credit cards, personal loans and car loans, by rolling them into your home loan. The result is a single loan with one repayment and, usually, a much lower interest rate. Whether it actually saves you money depends on your loan term, your repayment behaviour and the full cost of refinancing.

Every month, thousands of Australians wake up to the same quiet dread: checking their bank accounts and doing the mental juggle of which repayment hits when. A credit card minimum here, a personal loan instalment there, a car loan direct debit somewhere in between. Debt consolidation refinancing is the strategy many Australians are turning to, and when it is done right, it can genuinely change the financial trajectory of a household.

But “done right” is the operative phrase. Getting this strategy wrong can cost you more in the long run, not less. This guide gives you the honest picture so you can make a decision that actually moves you forward.

Debt consolidation refinancing is the process of taking out a new home loan, or restructuring your existing one, that is large enough to pay out your current mortgage plus your other outstanding debts. The result is a single loan, secured against your property, at a significantly lower interest rate than most unsecured consumer debts carry.

Because your property provides security, lenders are willing to offer lower rates than you would receive on credit cards or personal loans. This can reduce your total monthly repayments, simplify your finances and, when managed well, accelerate your path to financial freedom.

This article is for Australian homeowners who carry a mix of consumer debts alongside a home loan and want to understand whether consolidating those debts through refinancing is the right move. It is particularly relevant if you are an aspiring or active property investor who wants to strengthen your borrowing position for future purchases.

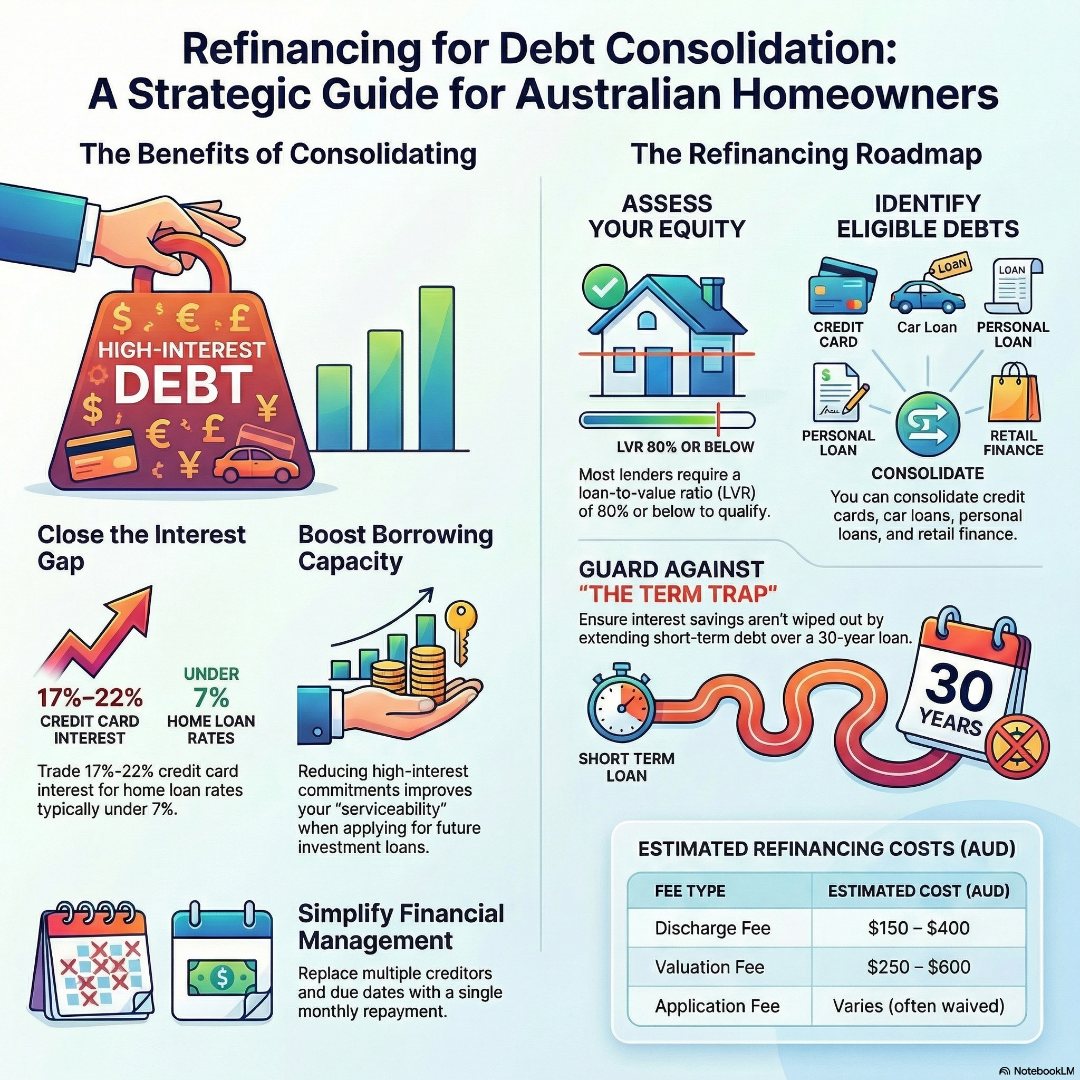

The average Australian credit card charges interest somewhere between 17% and 22% per year. Personal loans typically sit in the range of 8% to 15%. Your home loan, by contrast, generally sits well below 7%. That gap is not just a number on paper, it is real money leaving your household every single month.

The problem is not just the interest. It is the mental load. When you have four or five different creditors, each with their own due dates, their own minimum repayments and their own fine print, making smart financial decisions becomes genuinely hard. Most people default to just keeping the plates spinning rather than making meaningful progress against the balances.

Over time, this pattern does real damage. High-interest consumer debts grow faster than you can pay them down. You stay stuck. You delay investment decisions. You postpone the retirement timeline. And the anxiety of financial complexity starts to bleed into every other area of life.

Jane Slack-Smith, founder of Investors Choice Mortgages, has seen this pattern hundreds of times across her 20-year career.

Debt consolidation refinancing means taking out a new home loan, or restructuring your existing one, that is large enough to pay out your existing mortgage plus your other debts. You end up with a single loan and a single repayment, secured against your property.

Because your home is used as security, lenders are willing to offer significantly lower interest rates than you would get on unsecured products like personal loans or credit cards. The result can be a much lower combined interest bill and a simplified repayment structure.

The key requirement is equity. You need the value of your property to exceed your outstanding mortgage and the additional debts you want to roll in, with enough buffer to satisfy your lender’s loan-to-value ratio requirements. Most lenders require a loan-to-value ratio of 80% or below to avoid lenders mortgage insurance.

Most lenders will allow you to consolidate the following debts into a refinanced home loan:

Tax-deductible investment loans are generally kept separate for accounting purposes, especially if you hold investment properties. A good mortgage broker will walk you through correct structuring.

| Benefit | What It Means for You |

| Lower interest rate | Mortgage rates are typically far below credit card and personal loan rates |

| Single repayment | One due date, one amount, one lender to deal with |

| Improved cash flow | Monthly repayments often reduce significantly |

| Simplified budgeting | Easier to plan and track your finances |

| Potential credit score improvement | Consistent on-time repayments on one loan builds a stronger credit profile over time |

If you roll $30,000 of personal debt into a 25-year home loan at a lower rate, you may still pay more total interest than if you had cleared those debts faster on their original terms. The monthly saving feels good, but the long-term cost requires careful modelling.

I have had clients come to me genuinely excited about consolidating, and I completely understand why – the idea of rolling everything into one lower-rate loan sounds like an obvious win. But when we sat down together and pulled apart the fine print on their personal loans, the picture changed quickly. The early exit fees and break costs buried in those loan contracts were significant enough to wipe out the interest savings entirely, at least in the short to medium term. It was not that consolidation was the wrong strategy. It was that the timing and the specific loans involved meant we needed a different approach first. Doing this analysis before you commit is not optional. It is the difference between a decision that genuinely improves your financial position and one that just feels like progress.

Unsecured debts like credit cards cannot lead to you losing your home. Once you consolidate them into a secured mortgage, the stakes are different. It is not a reason to avoid consolidation, but it is a reason to go in with a clear repayment plan.

The most common trap post-consolidation is clearing the credit cards and then filling them back up again. The consolidation itself does not fix underlying spending patterns, and that part requires a conscious commitment from you.

Step 1: List all your current debts

Write down every debt you carry: the balance, the interest rate and the monthly minimum repayment. This gives you a clear picture of what you are working with and allows you to model the actual benefit of consolidation.

Step 2: Understand your property equity

Subtract your outstanding mortgage from the current market value of your property. If you have meaningful equity, ideally 20% or more remaining after consolidation, you are in a solid position to apply.

Step 3: Run the numbers honestly

This is where the Investors Choice Mortgages AI-powered hub becomes genuinely valuable. Use professional-grade calculators to compare your current total repayments against a consolidated structure, model the interest savings and account for any upfront costs.

Step 4: Speak to a specialist mortgage broker

Not all lenders approach debt consolidation refinancing the same way. Some are significantly more flexible with policy, better priced or better structured for investors versus owner-occupiers.

Step 5: Apply and proceed to settlement

Your broker manages the application, coordinates with your current lender’s discharge team and ensures the settlement process runs smoothly.

Step 6: Commit to the plan post-settlement

Close or reduce the limits on any credit facilities you just paid out. Redirect the cash flow you have freed up into either accelerating the loan repayment or, if your strategy calls for it, building the savings position you need for your next investment.

For aspiring or active property investors, getting debt under control is often the essential first step before they can qualify for the next investment loan.

Lenders assess your borrowing capacity based on your income relative to your total debt commitments. High-interest consumer debts reduce your assessed serviceability, which limits what you can borrow for investment purposes. Consolidating those debts into your home loan at a lower rate and lower monthly commitment can improve your borrowing position for the next purchase.

This is the strategic dimension that a general finance comparison website will not tell you. The decision is not just “does this save me money today?” It is also “does this position me better for my next investment move?”

Typical upfront costs:

A well-structured broker will ensure these costs are clearly disclosed upfront.

Debt consolidation refinancing is a genuinely powerful financial tool for Australians who carry high-interest consumer debt alongside a home loan with available equity. It can simplify your finances, reduce your monthly obligations and, when combined with smart post-consolidation habits, accelerate your path to financial freedom.

The critical variable is the quality of the advice and the structure of the loan. Done correctly, it is a stepping stone toward the kind of financial position that makes property investment possible. Done carelessly, it can cost you more than it saves.

If you are carrying multiple debts and wondering whether consolidation is the right move, the smartest first step is to run the numbers with the right tools and speak to someone who genuinely understands your long-term goals, not just your current balance.

Take the next step with Australia’s first AI-powered mortgage and property hub.

Professional-grade calculators, tools and strategic insights are available now.

Test the hub and get your personalised picture.

How much equity do I need to consolidate debt by refinancing?

Most lenders require your loan-to-value ratio to remain at 80% or below after consolidation to avoid lenders mortgage insurance.

Does consolidating debt through refinancing hurt my credit score?

There is typically a small, temporary dip in your credit score when you apply for any new credit, including a refinance. Over time, managing the new loan responsibly usually has a positive impact.

Is it better to refinance to consolidate debt or get a personal loan?

Most homeowners with adequate equity will find home loan refinancing produces a much lower interest rate.

Can I consolidate debt by refinancing if I am a property investor?

Yes, but take care not to mix investment and non-investment/debt, as specialist structuring is needed.

What is refinancing to consolidate debt? Refinancing to consolidate debt is the process of using the equity in your home to pay off...

What is refinancing to consolidate debt? Refinancing to consolidate debt is the process of using the equity in your home to pay off...