How to Reduce Risk During Market Volatility

Market volatility is inevitable in property investing, but it doesn't have to derail your wealth-building plans. Most successful...

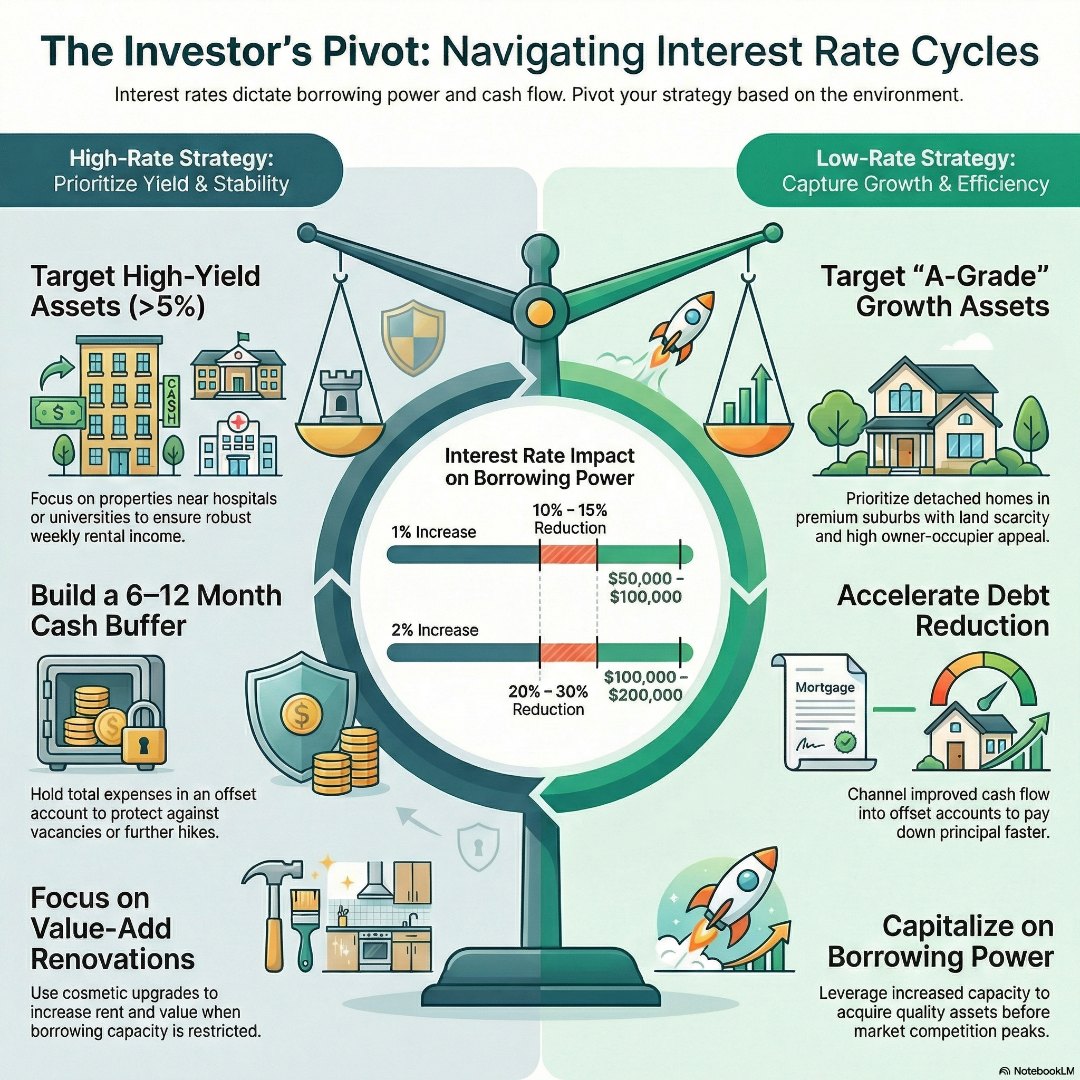

Interest rates are the invisible hand that shapes every property investment decision you make. Whether you’re building your first portfolio or expanding an existing one, understanding how rates influence your borrowing power, cash flow, and buying strategy can mean the difference between building wealth and struggling to keep properties afloat.

For most Australian property investors, adapting your strategy to work with the rate environment is more profitable than fighting against it. Rising rates demand a focus on yield and buffers, while falling rates reward quality acquisition and strategic expansion. The key variables that determine your success include borrowing capacity, rental yields, risk spread, and time horizon – with different approaches working better when rates move in different directions.

When interest rates rise, the effects are immediate and far-reaching. Lenders recalculate your borrowing power against higher repayment scenarios, meaning a property that worked at 4% may become a cash drain at 7%. This can slash your capacity and force tough choices about your portfolio.

Rental yields are critical in high rate periods. Weak rent-to-price ratios, once justifiable by capital growth, may turn properties into financial burdens. That’s why targeting properties in strong rental markets – such as those close to transport, reputable schools, and major employment hubs – becomes vital to maintaining positive cash flow.

Higher rates can also lead to faster corrections in investor-dominated areas, making risk management paramount.

Conversely, falling interest rates expand your borrowing capacity and improve portfolio cash flow. This breathing room enables faster debt reduction or positions you for new acquisitions, as buyer competition increases, especially for quality properties with strong owner-occupier appeal.

A-grade locations with limited supply and enduring family appeal see the strongest positive adjustment in these markets. Hot competition for these assets rewards a focus on fundamentals and long-term growth.

This is also an ideal time to review your refinancing options and lock in more favourable loan terms while retaining the flexibility to capitalise on future changes.

Interest rate movements influence whether you should prioritise cash flow or growth assets. In high-rate environments, properties offering robust weekly rents act as a financial safety net. For example, a $600,000 property generating $500 per week rent is less risky than buying into a more expensive market for similar income.

High-yield properties to target include:

Lower-rate markets, however, often favour growth-focused investments. In these conditions, targeting premium locations yields greater long-term rewards due to fundamental land scarcity and renewed buyer activity.

Strategic finance structures are critical to successfully navigating changing rate environments. Consider split loan arrangements to balance the advantages of fixed and variable rates. This can safeguard parts of your debt when rates are attractive, while allowing offset account benefits on the variable portion.

Interest-only loans may provide relief in high-rate periods if coupled with a solid plan for debt reduction. Always ensure extra cash flow is used for building buffers or paying down your principal place of residence.

Expert mortgage advice becomes invaluable as your property portfolio grows, helping you avoid rigid arrangements like cross-collateralisation, which can limit your ability to adapt.

Having adequate buffers is the hallmark of successful property investors. Aim to hold 6-12 months of total expenses (including maintenance, loan servicing, and personal costs) in accessible offset accounts, not redraw facilities. This approach means you’re better prepared for unexpected vacancies or further rate hikes, and have the liquidity to seize opportunities.

I remember vividly when the 2010 rate shock hit. On paper, my portfolio looked solid, but I’d made the classic mistake of assuming capital growth would outpace any temporary hiccups. I hadn’t built a substantial cash buffer. When those aggressive rate hikes started landing, my repayments jumped almost overnight while rents stayed flat. I spent far too many nights losing sleep over bank notifications, wondering how I’d bridge the gap. That period was a brutal wake-up call that hope is never a strategy. It forced me to strip back every expense, renegotiate my finance, and meticulously rework my cash flow forecasts just to stay afloat. Today, I tell my clients that buffers aren’t just a safety net – they are the only thing standing between you and a forced sale when the market takes an unexpected turn.

Calculate your required buffer by considering:

Cultivate these buffers during market upswings, not when you’re scrambling in a downturn.

Scenario 1: Rates Rising Rapidly

Rita, like many investors, should target yield-generating units near good transport links returning at least 4-5% yields. Strategic cosmetic renovations can further increase both cash flow and property value.

Scenario 2: Rates Stable or Falling

Rita can shift focus to quality family homes in good school zones within established suburbs. These offer both stronger capital growth and solid rental returns.

Scenario 3: Rate Uncertainty

Here, Rita should prioritise split loan structures and maintain healthy offset buffers. Properties offering both yield and some growth potential – such as well-located properties with renovation upside – become ideal.

The most successful Australian property investors develop strategies resilient across all rate cycles. Focus on properties with solid rental demand, strong infrastructure, and enduring owner-occupier appeal, rather than chasing trends.

Prioritise maintaining holdings you can easily afford in difficult market periods; forced sales often lead to greater wealth loss than temporary downturns. Your first step should be to review your current loan structure to ensure it’s fit for purpose, offers enough flexibility, and maximises available buffers.

Remember, rate changes are a natural part of the investment cycle. They offer astute investors fresh opportunities if you adjust your strategy and prepare your finances well.

Seizing the advantages of both high and low rate cycles requires solid preparation, a flexible finance strategy, and the ability to adapt swiftly. Whether the Reserve Bank is increasing rates or setting them low to encourage spending, your goal remains the same: to acquire assets you can safely hold and optimise your cash flow through all market conditions.

Ready to ensure your property investment strategy works in any interest rate environment? Book a mortgage review call today to discuss how current rate changes might affect your plans and to discover financing structures that provide flexibility across different market cycles.

How much do interest rates affect my borrowing capacity for investment properties?

Every 1% jump in rates generally reduces borrowing capacity by 10-15%. For many, this equates to $50,000-100,000 less to invest, as lenders must stress-test your repayments at higher levels, thereby cutting your ability to borrow.

Should I fix my investment property interest rates when they’re rising?

While fixing rates delivers repayment certainty, it also limits flexibility. Consider fixing 60-80% of your investment debt, leaving a portion variable for offset use. Split loans offer a strong balance of stability and adaptability. Read more on fixing your loan.

What’s the minimum rental yield I should target during high interest rate periods?

Aim for a minimum of 5-5.5% yield in reliable markets. This cushion protects your cash flow from rate rises and covers periods with vacancies or additional expenses. Discover more about rental yield importance.

How do falling interest rates change the types of properties I should buy?

With lower rates, you can target higher-value properties with strong capital growth prospects, even if yields are lower. Look for land-scarce, established suburbs, reputable school zones, and areas with enduring owner-occupier appeal.

Market volatility is inevitable in property investing, but it doesn't have to derail your wealth-building plans. Most successful...

Economic uncertainty creates a unique paradox: while most investors freeze in fear, educated investors often find their greatest opportunities....