Why Do Interest Rates Rise During Inflation?

When inflation climbs, interest rates typically rise because central banks - like Australia's Reserve Bank - deliberately make...

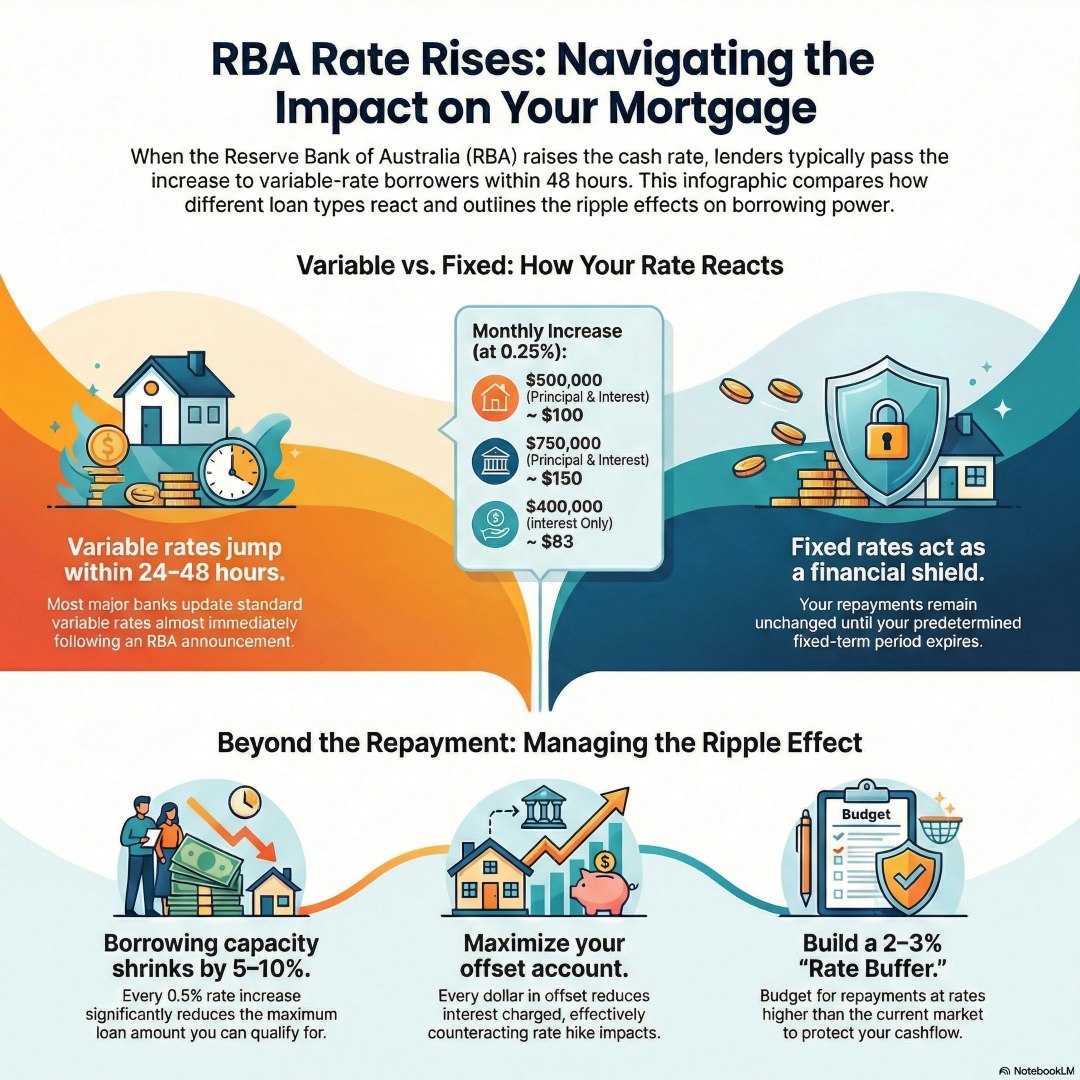

If you have a variable rate mortgage, your repayments will likely increase when the RBA raises interest rates. Banks typically pass on these rate rises within days or weeks of an RBA announcement. However, if you’re on a fixed-rate mortgage, your repayments remain unchanged until your fixed term expires. A 0.25% rate increase on a $500,000 loan typically adds around $100 to monthly repayments.

When the Reserve Bank of Australia adjusts the official cash rate, it sets off a chain reaction that reaches your mortgage repayments faster than most borrowers expect. The cash rate is the interest rate charged on loans between banks, and it forms the foundation for all lending rates across Australia.

If you’re holding a variable rate mortgage, you’re essentially agreeing to ride the interest rate rollercoaster. Within 24 to 48 hours of an RBA announcement, most major banks update their standard variable rates to reflect the change. This isn’t a maybe. It’s standard banking practice that’s been consistent for decades.

The mathematics are straightforward but the impact is real. For every 0.25% increase on a $500,000 loan over 30 years, expect your monthly repayments to climb by approximately $100. On a $750,000 loan, that same increase translates to roughly $150 extra per month. These aren’t abstract numbers. They represent real money coming out of your household budget.

While the monthly repayment increase captures most attention, rising interest rates create ripple effects that extend far beyond your regular mortgage payment. Your borrowing capacity shrinks with each rate rise, potentially affecting future investment plans or refinancing options.

Banks recalculate your serviceability using the new, higher rates when assessing any new loan applications. A borrower who could previously qualify for a $600,000 loan might find their maximum borrowing capacity reduced to $550,000 or less after a series of rate increases.

Interest-only borrowers face even sharper impacts. Since they’re only paying interest charges, any rate increase flows directly to their repayments without the cushioning effect of principal reduction. A borrower paying interest-only on a $400,000 loan sees their monthly payments jump by $83 for every 0.25% increase.

Property investors managing multiple mortgages experience multiplied effects. Three investment properties with variable rate mortgages means three separate payment increases, creating significant cash flow pressures that can strain even well-planned investment strategies.

Fixed-rate mortgages operate as your financial insurance policy against interest rate uncertainty. When you lock in a fixed rate, you’re essentially purchasing protection from rate movements for a predetermined period, typically one to five years.

This protection works both ways. If rates rise, you continue paying your locked-in rate, but if rates fall, you miss out on potential savings. The decision becomes a calculated risk assessment of where you believe rates are heading and how much certainty you value in your budgeting.

Many Australian borrowers adopt a split strategy, fixing a portion of their loan while keeping another portion variable. This approach provides some protection from rate rises while maintaining flexibility to benefit from potential rate reductions.

However, fixed rates aren’t permanent solutions. When your fixed term expires, you’ll face whatever the current market rates are at that time. Many borrowers who fixed during the ultra-low rate environment of 2020-2022 are now confronting significantly higher rates as their fixed terms conclude.

Understanding how to calculate your new repayments empowers you to budget proactively rather than waiting for your bank’s notification. The calculation involves compound interest mathematics, but online mortgage calculators simplify the process.

Most Australian lenders provide online calculators where you can input your current loan balance, interest rate, and remaining loan term to determine new repayments under different interest rate scenarios. This tool becomes invaluable for stress-testing your budget against potential rate increases.

For manual calculations, the monthly repayment formula considers your principal loan amount, the new interest rate, and remaining loan term. However, given the complexity of compound interest calculations, digital tools provide more accurate results and allow for easy scenario modelling.

But understanding the numbers isn’t just a technical exercise; it’s the foundation of financial confidence, a lesson I learned firsthand early in my career.

When I talk to clients about preparing for interest rate rises, I’m always reminded of a very real turning point in my own property journey. Years ago, just as my partner and I had stretched ourselves into our first renovations, the RBA delivered a rate hike that sent our hearts racing. We weren’t seasoned investors—not by a long shot. Honestly, we worried we’d bitten off more than we could chew. But here’s what changed the game: every Sunday night, we had an unglamorous “spreadsheet ritual.” We’d sit at the kitchen table, plug the latest rate into our trusty Excel sheet, and watch those repayment numbers dance up and down. It wasn’t fancy, but it meant that when the RBA made its surprise move, we weren’t scrambling. We saw—sometimes uncomfortably—how even a 0.25% jump could nudge our repayments and our sense of financial control. Instead of panicking, we adjusted our budget before the new repayments landed and reached out to our broker to explore restructuring options. That routine gave us more than numbers; it gave us peace of mind—and the confidence to make proactive decisions, not reactive ones. If you haven’t run your numbers since the last RBA announcement, you’re not alone. But trust me: a few honest minutes with your finances now means a world of less stress later. And you don’t need to be an accountant—just willing to look and, if it’s time, ask for expert help.

Banks typically notify borrowers of repayment changes through multiple channels, including email, SMS, and postal letters, usually giving at least one cycle’s notice before new repayments take effect. This notification period provides time to adjust household budgets accordingly.

Despite currently higher fixed rates compared to variable rates in many cases, fixing can still provide value in specific circumstances. Borrowers who prioritise budget certainty over potential savings often find comfort in knowing their exact repayment amount for years ahead.

First-time homebuyers frequently benefit from fixing at least a portion of their loan during their initial years of homeownership. This period typically involves highest financial stress as borrowers adjust to mortgage repayments while establishing their household budgets.

Investors with tight cash flow margins might consider fixing to ensure their investment properties remain positively geared or to limit negative gearing impacts. Predictable repayments enable more accurate investment return calculations and reduce the risk of forced sales due to unaffordable repayments.

Borrowers approaching retirement or those on fixed incomes often prioritise repayment certainty over potential savings. For these groups, budget predictability outweighs the possibility of benefiting from future rate reductions.

Building a buffer in your budget provides the first line of defence against rate rise impacts. Financial experts recommend maintaining repayments as if rates were 2-3% higher than current levels, treating the difference as automatic savings or loan principal reduction.

Offset accounts become increasingly valuable during rising rate environments. Every dollar in your offset account reduces the interest charged on your loan, effectively providing a return equal to your mortgage rate. Maximising offset balances can partially counteract rate increase impacts.

Refinancing options deserve consideration when your current lender’s rates become uncompetitive. However, factor in switching costs including discharge fees, application fees, and valuation costs when calculating potential savings.

Some borrowers choose to increase their repayment frequency from monthly to fortnightly or weekly. This strategy reduces total interest paid over the loan term and can help manage cash flow during periods of rate volatility.

Regular mortgage health checks with qualified mortgage professionals help identify optimisation opportunities before rate pressures become overwhelming. These reviews can uncover better rate options, improved loan structures, or alternative strategies to manage rising costs.

Don’t let rising interest rates derail your property and financial goals. Book a mortgage review call today to explore strategies for protecting your budget and optimising your loan structure in the current rate environment.

How much can my mortgage repayment increase if the RBA raises rates by 0.25%?

A 0.25% rate increase typically adds approximately $100 per month to a $500,000 loan over 30 years. The exact increase depends on your loan balance, remaining term, and current interest rate. Larger loans see proportionally larger increases, while shorter loan terms result in smaller monthly payment changes. For example, on a $750,000 loan, the same 0.25% increase would add about $150 to your monthly repayments.

Are there any early exit fees if I refinance to a lower rate?

Most variable rate mortgages in Australia don’t charge early exit fees, as these were banned for loans taken out after July 2011. However, fixed-rate loans often include break costs if you exit before the fixed term ends. These break costs can be substantial, especially in a falling interest rate environment. Additionally, discharge fees from your current lender (typically $300-$400) and application fees with your new lender are standard costs to factor into refinancing decisions.

What costs should first home buyers budget for during a rising interest rate cycle?

Beyond increased repayments, first home buyers should budget for reduced borrowing capacity if still house hunting, potential mortgage insurance premium increases, and higher minimum deposit requirements as lenders become more conservative. It’s also wise to consider the opportunity cost of delayed purchases if waiting for rates to stabilise. Building a rate rise buffer of 2-3% above current rates into your budget calculations provides crucial protection against future increases.

How can I estimate my new repayments as rates change?

Use your lender’s online mortgage calculator or independent calculation tools to model different rate scenarios. Input your current loan balance, interest rate, and remaining term, then adjust the rate to see new repayment amounts. Most calculators also show total interest savings or costs over the loan term. For a more personalised assessment, many mortgage brokers offer free repayment analysis services that account for your specific loan features and circumstances.

What are the hidden costs associated with rising interest rates?

Beyond monthly repayment increases, consider reduced borrowing capacity for future purchases (typically 5-10% less borrowing power for each 0.5% rate increase), potential negative equity if property values stagnate while rates rise, increased opportunity costs of holding cash instead of paying down debt, and the psychological stress of budget uncertainty during volatile rate periods. For investors, rising rates can also trigger changes in taxation benefits and rental yield calculations.

When inflation climbs, interest rates typically rise because central banks - like Australia's Reserve Bank - deliberately make...

Market volatility is inevitable in property investing, but it doesn't have to derail your wealth-building plans. Most successful...