Why Do Interest Rates Rise During Inflation?

When inflation climbs, interest rates typically rise because central banks - like Australia's Reserve Bank - deliberately make...

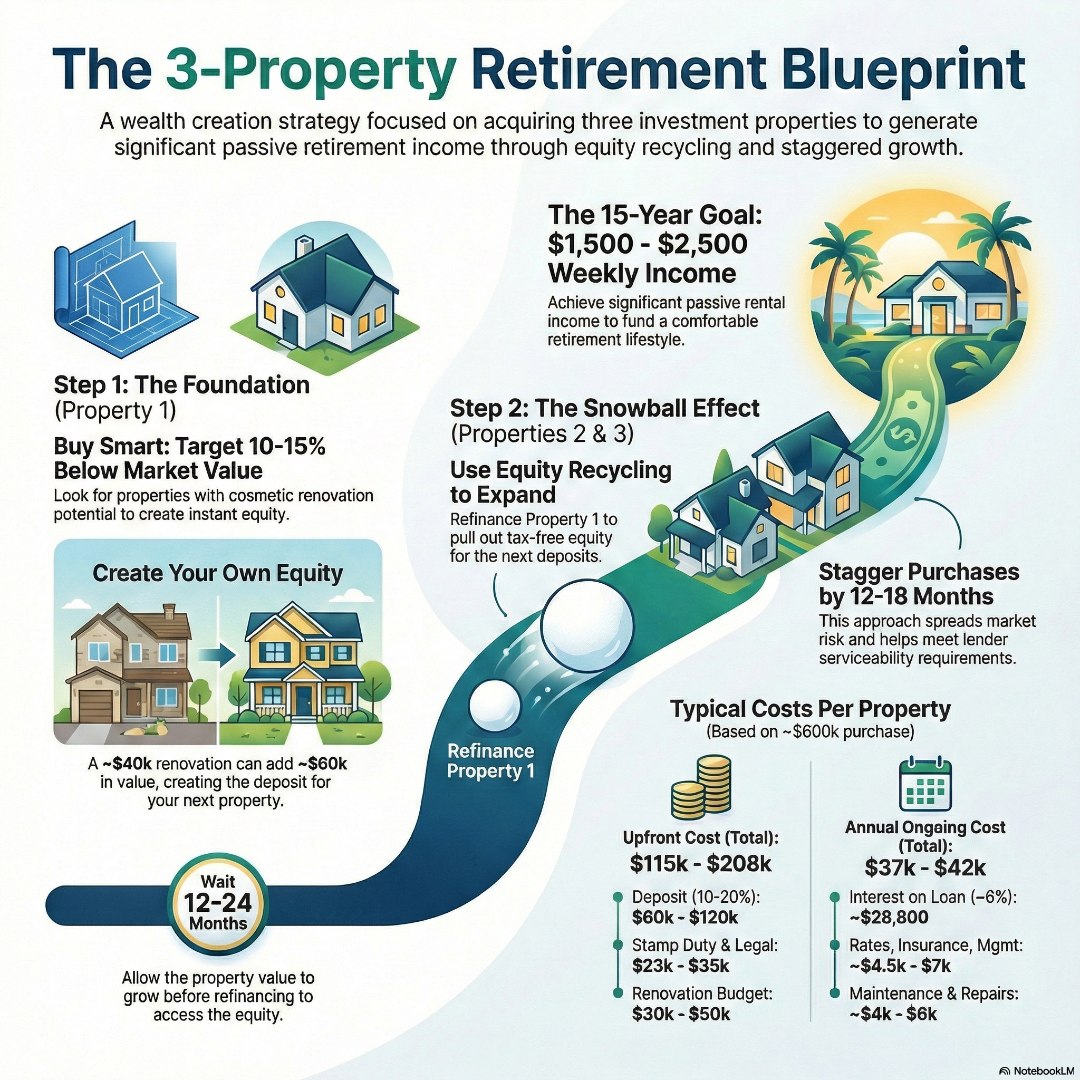

Building a 3-property retirement plan represents one of the smartest wealth-creation strategies for Australians approaching their 50s, but it demands careful planning, realistic budgeting, and strategic execution. For most investors, this approach offers the perfect balance between manageable risk and substantial passive income potential typically generating $1,500-$2,500 per week in rental income within 10-15 years. However, success hinges on understanding the true costs involved and implementing proven strategies that maximise capital growth while maintaining cash flow neutrality. The key lies in starting with the right foundation property, leveraging equity strategically, and planning for both upfront investments and ongoing expenses that can easily reach $50,000-$80,000 annually across three properties.

The magic of a 3-property retirement plan lies in diversification and compounding growth. Unlike superannuation or single-asset strategies, three well-chosen properties across different suburbs or markets provide multiple income streams and capital growth opportunities. This approach recognises that property investment is not about quick wins it is about patient wealth building over 10-20 years.

Rita, a 45-year-old professional from Sydney, discovered this strategy after years of watching her savings account deliver minimal returns. “We had nearly paid off our home but felt like we were sitting on dead money,” she explains. “When we understood how to use our equity strategically, it opened up possibilities we never imagined.”

The three-property strategy works because it provides enough diversification to weather market fluctuations while remaining manageable for time-poor professionals. Unlike larger portfolios that require intensive management, three properties allow you to maintain quality control while building substantial wealth.

Your first investment property sets the tone for everything that follows. The key is finding properties with immediate value-add potential typically unrenovated homes in solid suburbs with good schools, transport links, and employment hubs.

Look for 3-bedroom houses or properties with subdivision or duplex potential in middle-ring suburbs. These properties should be purchased 10-15% below market value, allowing for immediate equity creation through cosmetic renovations. Budget $30,000-$50,000 for kitchen and bathroom updates, fresh paint, and landscaping improvements that can add $50,000-$100,000 in value.

The numbers matter here. On a $600,000 purchase with a $480,000 loan at 6% interest, your annual interest costs hit approximately $28,800. However, rental income of $500-550 per week ($26,000-$28,600 annually) largely offsets this expense, especially when factoring in tax deductions for depreciation, maintenance, and property management fees.

Consider Sarah’s story: she purchased a tired 1960s brick home in Brisbane’s outer growth corridor for $580,000. After a $40,000 renovation focusing on the kitchen, main bathroom, and outdoor entertaining area, the property revalued at $680,000. This $60,000 equity gain became the foundation for her second purchase just 18 months later.

Once Property 1 has seasoned for 12-24 months and grown in value, the equity recycling strategy begins. Refinance to access this equity tax-free, using it as deposits for Properties 2 and 3. This approach accelerates your timeline significantly compared to saving deposits from scratch.

The mathematics are compelling. If Property 1 grows from $580,000 to $680,000, you have created $100,000 in accessible equity. This becomes the deposit for a second $600,000 property, which then begins its own growth cycle. The compounding effect means three properties can grow your net worth faster than single-property strategies.

However, timing matters. Stagger your purchases 12-18 months apart to ensure serviceability requirements are met and each property has time to establish rental income and begin capital growth. This approach also spreads your market entry risk across different time periods.

For Property 2, consider diversifying location or property type. If Property 1 is a house in outer Brisbane, Property 2 might be a townhouse in Melbourne’s growth corridors or a unit in a capital city with strong rental demand. The key is maintaining the same buying criteria: below-market purchase price, value-add potential, and strong rental fundamentals.

The analytical side of property investment is critical, but it’s the emotional commitment that determines success. Even with all the spreadsheets and projections, no amount of numbers can fully prepare you for the leap of faith that real investment requires. I remember standing outside my very first reno project, exhausted from the hundredth trip to Bunnings and close to pulling the plug because suddenly, the cost overruns and renovation chaos seemed insurmountable. But in that moment, I saw beyond the mess and pictured my three kids—not just playing in the yard, but heading off to universities they’d choose, with options I never had at their age. That vision snapped me back. It made every late-night repair and every budget blowout feel like an investment in their future, not just another cost. Looking back now, that decision—stepping through my own doubts and keeping the long game in mind—became the start of a snowball effect in our finances. The first property was hard, yes, but it provided the equity and the confidence for properties two and three. The point is: the numbers stack up, but the real driver is your “why.” When the upfront costs or setbacks hit, anchor yourself to your bigger outcome. That’s what carries you through the grind and into your own version of freedom.

Building a 3-property portfolio requires significant upfront capital, but the numbers are manageable when spread across 3-5 years and funded through equity recycling.

The beauty of this strategy is that only the first property requires saved deposit money. Properties 2 and 3 are funded through equity from earlier purchases, making the strategy accessible to middle-income earners with solid home equity.

Many investors underestimate these costs and find themselves stretched thin. Smart planning includes a 10% buffer above your calculated costs and ensuring you maintain adequate cash reserves for unexpected expenses during the building phase.

The ongoing costs across three properties represent a significant annual commitment, but these expenses are largely offset by rental income and tax benefits, particularly in the early years through negative gearing.

Total annual costs per property: $37,300-$41,800 Three-property total: $111,900-$125,400

However, rental income typically covers 70-80% of these costs, leaving you with a net annual contribution of $25,000-$40,000 across three properties. This negative gearing provides substantial tax benefits for high-income earners while building long-term wealth.

As properties increase in value and rental income grows over time, many investors find their portfolios transition from negative to neutral or positive cash flow within 5-7 years. This transition period requires careful financial planning but rewards patient investors with both tax benefits and wealth accumulation.

This strategy works best for established professionals in their 40s and 50s with household incomes above $120,000, substantial home equity, and stable employment. You need the income to service additional debt and the equity to fund deposits without compromising your family home security.

The strategy particularly suits investors who want enough properties to create meaningful retirement income without the complexity of larger portfolios. Three well-chosen properties generating $1,500-$2,500 per week in rent can support comfortable retirement lifestyles, especially when combined with superannuation and potential property sales to reduce debt.

Consider the tax advantages during accumulation years. High-income earners benefit significantly from negative gearing deductions, potentially saving $10,000-$15,000 annually in tax across three properties. These savings can be redirected into borrowing capacity strategies or additional equity building through loan principal payments.

Success with a 3-property retirement plan requires disciplined execution and careful risk management. Understanding how interest rates impact your mortgage costs becomes critical when managing multiple properties simultaneously.

Stress-test your strategy for 2-3% interest rate increases and 10% property value decreases. Ensure you can service all loans even if one property becomes vacant for 2-3 months. This conservative approach protects your family home and prevents forced sales during market downturns.

Location diversification across different suburbs or cities reduces concentration risk. Consider mixing property types houses for capital growth, units for higher yields to balance your portfolio’s performance characteristics.

Professional support becomes essential. Work with specialist mortgage brokers who understand investment strategies to structure loans optimally and maintain flexibility for future purchases. The right broker can save thousands through proper loan structuring and ongoing portfolio optimisation.

Start by assessing your current financial position. Calculate available equity in your home, review your borrowing capacity, and ensure stable employment before committing to this strategy. The foundation must be rock-solid before building your investment portfolio.

Create realistic timelines. Plan 18-24 months between purchases to allow proper seasoning and equity building. This patient approach reduces risk and ensures sustainable growth rather than overextension.

Establish your investment criteria early: target suburbs, property types, and renovation budgets. Having clear parameters prevents emotional purchasing decisions and keeps you focused on properties that align with your strategy.

Most importantly, understand that this is a long-term wealth-building strategy, not a get-rich-quick scheme. The real benefits compound over 10-15 years as properties appreciate, rents increase, and loan balances decrease.

A well-executed 3-property retirement plan can transform your financial future, but success demands careful planning, realistic budgeting, and strategic patience. The upfront costs are significant potentially $200,000-$400,000 across the portfolio but equity recycling makes this achievable without depleting your savings. Ongoing annual costs of $50,000-$80,000 initially seem daunting but are largely offset by rental income and tax benefits, transitioning to positive cash flow over time.

The key lies in starting with solid foundations: stable income, substantial home equity, and clear investment criteria. Focus on buying 10-15% below market value, add immediate value through strategic renovations, and leverage your growing equity systematically across 3-5 years.

Ready to explore if a 3-property retirement strategy aligns with your financial goals? Book a mortgage review call today to discuss your borrowing capacity, optimal loan structures, and create a personalised roadmap for your property investment journey.

How much deposit do I need for a 3-property retirement plan?

You typically need $60,000-$120,000 deposit for your first property, but properties 2 and 3 can be funded through equity from earlier purchases. This equity recycling strategy means you do not need to save three separate deposits.

Is there a tax advantage to buying three investment properties instead of one?

Yes, three properties provide greater negative gearing deductions during accumulation years, potentially saving $10,000-$15,000 annually in tax. This is especially beneficial for high-income earners in their peak earning years.

What ongoing costs should I budget for three investment properties annually?

Budget $50,000-$80,000 annually across three properties for rates, insurance, management, maintenance, and interest costs. Rental income typically covers 70-80% of these expenses, requiring $15,000-$25,000 net contribution initially.

How long should I hold properties in a 3-property retirement strategy?

Hold each property minimum 7-10 years to maximise capital growth and minimise transaction costs. The real wealth building occurs through long-term appreciation and rental growth, not short-term trading.

Can I build a 3-property portfolio if I am over 50 years old?

Yes, but loan serviceability becomes more critical as retirement approaches. Lenders may require faster loan repayment schedules, so professional mortgage advice is essential to structure loans optimally for your age and income situation.

When inflation climbs, interest rates typically rise because central banks - like Australia's Reserve Bank - deliberately make...

Market volatility is inevitable in property investing, but it doesn't have to derail your wealth-building plans. Most successful...