What Hidden Costs Do You Still Pay When Using a Government Scheme?

Government schemes like the First Home Guarantee and the First Home Owner Grant are genuinely game-changing for eligible buyers. But here is the...

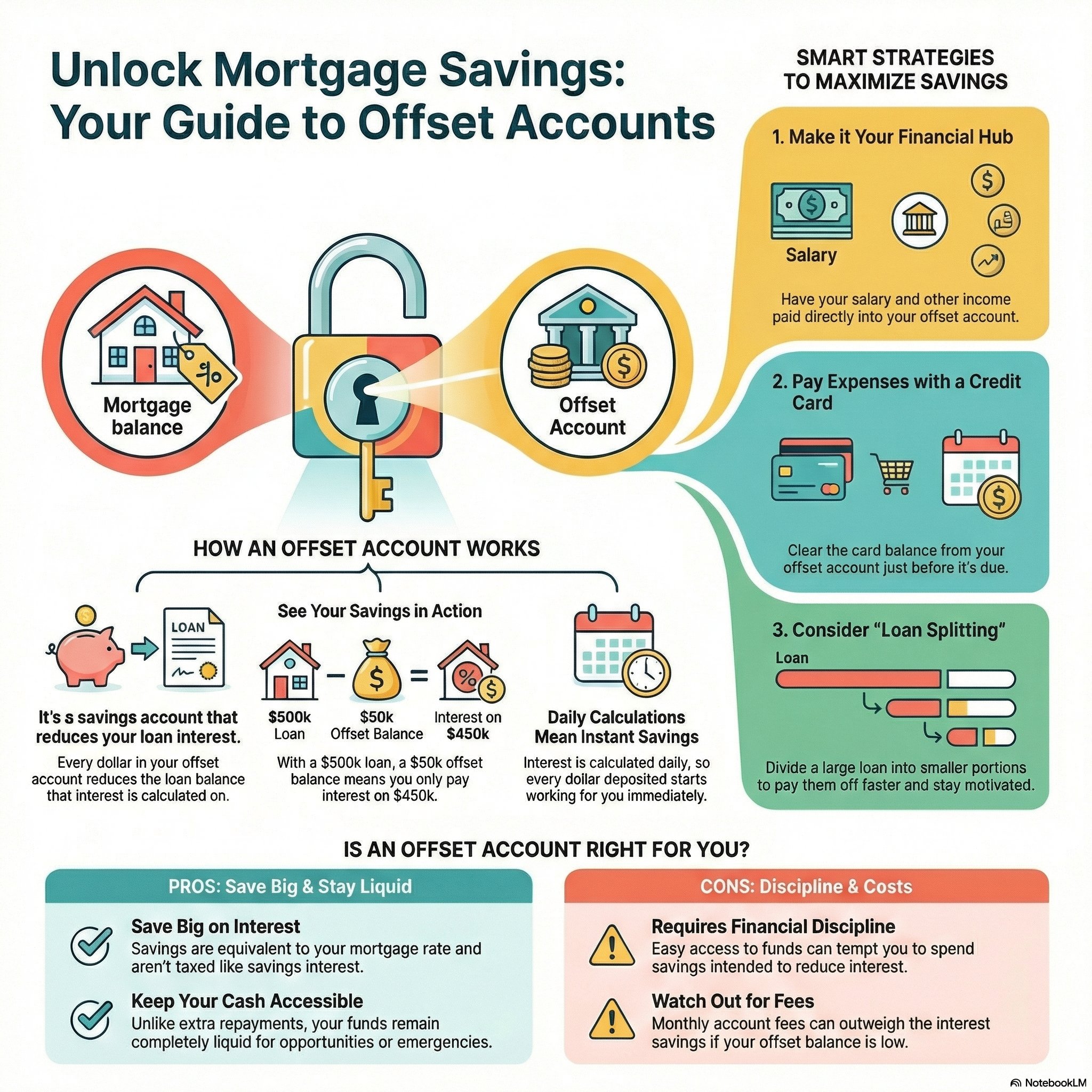

Offset accounts represent one of Australia’s most powerful yet underutilised mortgage tools, capable of saving property investors and homeowners thousands of dollars in interest payments without locking away their cash. Unlike traditional savings accounts that earn taxable interest, offset accounts directly reduce the balance on which your mortgage interest is calculated, delivering immediate and ongoing financial benefits while maintaining complete access to your funds.

The strategy works by linking your transaction or savings account to your home loan, where every dollar in the offset account reduces the loan balance for interest calculation purposes. For example, with a $500,000 mortgage and $50,000 in your offset account, you only pay interest on $450,000, potentially saving hundreds of dollars monthly while keeping your money readily accessible for opportunities or emergencies.

Most borrowers don’t realise that Australian lenders calculate mortgage interest daily and charge it monthly. This timing creates a significant opportunity for strategic offset account users. Every dollar that sits in your offset account for even one day reduces your interest charges immediately.

Consider Sarah, a property investor with a $600,000 investment loan. When she receives her quarterly rental income of $9,000, depositing it into her offset account saves her approximately $45 in interest charges for that quarter, money that would otherwise go straight to the bank. Over a year, strategic use of rental income, tax refunds, and salary bonuses through her offset account saves her nearly $2,000 in interest payments.

The daily calculation system also means timing matters. Savvy borrowers use their offset accounts as their primary transaction account, paying all expenses via credit card throughout the month, then clearing the card balance from the offset account just before the monthly interest calculation. This strategy keeps maximum funds working to reduce interest for the longest possible time.

Property investors often combine offset accounts with interest-only (IO) loans to create powerful wealth-building strategies. With IO loans, monthly payments cover only interest charges, freeing up cash flow that can be directed into the offset account. This approach provides several advantages over traditional principal-and-interest repayments.

When you make extra repayments on a standard loan, that money reduces the principal but becomes inaccessible without costly redraw processes. However, money in an offset account delivers the same interest-saving benefits while remaining completely liquid. This flexibility proves invaluable for investors who need quick access to funds for property improvements, additional investments, or unexpected opportunities.

I’ve built my entire portfolio on the backbone of this strategy. For me, it’s not just about saving interest; it’s about bulletproofing my finances. I tell my clients the same thing: On every property I’ve purchased, my first priority wasn’t paying down the principal quickly, but rather building a robust cash buffer within the offset account. This isn’t just theory—it’s protection against life. Whether it’s a job change, a market correction, or an unexpected repair bill, having that accessible cash means I never have to panic or sell an asset under pressure, allowing me to stay resilient and ready for the next opportunity.

For investors managing multiple properties, the IO-plus-offset strategy provides enhanced cash flow management. Monthly repayments remain lower and predictable, while excess funds in offset accounts provide the equivalent of principal repayments without the commitment. This approach allows investors to maintain financial flexibility while building equity through property appreciation and strategic debt reduction.

Advanced offset account users employ loan splitting strategies to accelerate their debt reduction results. Instead of having one large mortgage with a single offset account, they divide their loan into smaller portions, each with its own offset account. This approach creates psychological and practical benefits that drive faster debt elimination.

Take Michael, who split his $400,000 investment loan into four $100,000 portions, each with a dedicated offset account. By focusing all surplus funds into the first offset account until it reached $100,000, he effectively eliminated interest charges on that portion entirely. This achievement provided immediate motivation and substantial monthly savings, which he then directed toward filling the second offset account.

The splitting strategy works because it creates clear, achievable targets rather than the overwhelming prospect of paying off a massive loan. When one offset account reaches its target, the sense of accomplishment drives continued progress. Additionally, some lenders offer different interest rates for smaller loan amounts, potentially providing additional savings opportunities.

Your choice of offset account structure significantly impacts your savings potential. One hundred percent offset accounts, where every dollar counts fully against the loan balance, provide maximum benefits. Some lenders offer partial offset accounts (such as 60% or 80% offset), but these dilute your savings and should generally be avoided in favour of full offset options.

The most effective offset users treat their account as their primary banking facility. All income gets deposited directly into the offset account, while expenses are managed through a linked transaction account or credit card. This approach ensures maximum funds remain working to reduce interest charges while maintaining convenient access to money for daily expenses.

Smart borrowers also coordinate their offset strategy with other financial products. For instance, using a credit card for all monthly expenses and paying the balance from the offset account at month-end keeps more money working to reduce interest for longer periods. Similarly, timing large payments like quarterly insurance or annual memberships to coincide with bonus income or rental receipts maximises the offset benefits.

To fully harness the power of offset accounts, consider implementing these strategic practices:

By implementing these strategies systematically, you can significantly enhance your offset account’s effectiveness and accelerate your mortgage reduction timeline.

Many borrowers undermine their offset account benefits through poor management habits. The most common mistake involves frequently accessing offset funds for non-essential purchases. While offset accounts provide flexibility, constantly dipping into these funds eliminates their interest-saving benefits and can create a dangerous spending pattern.

Another frequent error involves choosing banks based solely on interest rates while ignoring offset account quality. Some lenders impose monthly fees on offset accounts, require minimum balances, or limit the number of transactions. These restrictions can significantly erode the benefits, making a slightly higher interest rate with superior offset features more cost-effective overall.

Borrowers also often misunderstand the tax implications. Unlike traditional savings accounts, offset accounts don’t generate taxable interest income, the benefit comes through reduced mortgage interest payments. This distinction makes offset accounts particularly valuable for higher-income earners who would face significant tax on traditional savings interest.

Despite their benefits, offset accounts aren’t suitable for every borrower. Individuals who struggle with spending discipline may find easy access to offset funds counterproductive to their savings goals. For these borrowers, making extra principal repayments or investing in term deposits might provide better outcomes through forced savings discipline.

Offset accounts also become less valuable when interest rates are very low relative to investment returns available elsewhere. During periods when quality investments consistently outperform mortgage interest rates, directing surplus funds toward those investments rather than offset accounts may generate superior long-term wealth building results.

Small balances in offset accounts may not justify account keeping fees charged by some lenders. If you typically maintain less than $10,000 in surplus funds, the monthly fees for offset account access might exceed the interest savings generated, making the facility counterproductive to your financial goals.

Successful offset account implementation requires a systematic approach and ongoing management. Begin by calculating your potential savings using your current loan balance and typical surplus funds. Most lenders provide online calculators that demonstrate the interest savings and shortened loan terms possible with different offset balances.

Review your current banking arrangements and identify opportunities to consolidate accounts and streamline fund flows into your offset account. Consider whether loan splitting might accelerate your progress and whether your current lender offers competitive offset account terms compared to alternatives in the market.

Establish clear rules for offset account management, including guidelines for when funds can be accessed and how you’ll maintain target balances. Many successful offset users implement a “replacement rule”, any money withdrawn must be replaced within a specific timeframe to maintain interest-saving momentum.

Remember that offset accounts work best as part of a comprehensive financial strategy rather than standalone solutions. Choosing the right loan structure and understanding your refinancing options can enhance your offset account benefits and overall financial position.

The power of offset accounts lies not just in their interest-saving capabilities, but in the flexibility they provide for building long-term wealth. When used strategically, they become a cornerstone tool for property investors and homeowners seeking to minimise borrowing costs while maintaining financial agility for future opportunities.

Whether you’re just starting your property journey or managing an established portfolio, implementing an effective offset account strategy can save thousands of dollars annually while keeping you positioned for your next investment opportunity. The key lies in understanding how these accounts work, choosing the right structure, and maintaining the discipline to maximise their benefits over time.

Ready to discover how much you could save with the right offset account strategy? Book a mortgage review call today to explore how these powerful tools can accelerate your path to financial freedom while keeping more money in your pocket.

How much can I actually save with an offset account on my mortgage?

Your savings depend on your loan balance, offset account balance, and interest rate. For example, maintaining $50,000 in an offset account against a $500,000 loan at 6% saves approximately $3,000 annually in interest payments while keeping your money accessible. The higher your loan interest rate, the greater the savings benefit from your offset account.

Should I use an offset account or make extra repayments on my mortgage?

Offset accounts provide identical interest savings to extra repayments but maintain complete liquidity of your funds. This makes them superior for most borrowers, especially property investors who need access to capital for opportunities or unexpected expenses. If you’re certain you won’t need to access your extra funds, direct repayments may work well, but offset accounts offer greater flexibility with the same financial benefit.

Do offset accounts work with fixed rate mortgages?

Most lenders don’t offer offset accounts with fixed rate loans, as the fixed rate structure conflicts with the variable balance calculations required for offset benefits. You’ll typically need a variable rate loan to access offset account features. Some lenders offer partial offset features on fixed loans, but these generally provide reduced benefits compared to full offset accounts on variable loans.

Can I have multiple offset accounts for one mortgage?

Many lenders allow multiple offset accounts linked to a single loan, and some borrowers split their loans into smaller portions with dedicated offset accounts for each. This strategy can accelerate debt reduction by creating achievable targets for each account. Multiple offset accounts can also help separate funds for different purposes while all working to reduce your mortgage interest.

Are there any fees I should know about with offset accounts?

Some lenders charge monthly account keeping fees for offset accounts, ranging from $10-30 per month. These fees can erode benefits for smaller balances, so compare the potential interest savings against any ongoing costs before choosing an offset account facility. Additionally, some premium offset accounts with enhanced features may have higher ongoing costs that need to be factored into your decision.

Government schemes like the First Home Guarantee and the First Home Owner Grant are genuinely game-changing for eligible buyers. But here is the...

Disclaimer: These are generated via AI – please note that you need to do your own due diligence and read the report yourself to make your own...