Property Review Video – August 2023

Stay up to date with the latest developments in the property market over the past month. Our video takes you through an overview of the state of...

Many of us have dreamed of owning a holiday home, creating an escape from the hustle and bustle of city life. Holiday homes are great for bringing family and friends together and making memories. Whether it’s a beach house or a place in the bush, it’s a place to unwind and relax. It can also be used to generate income as a short-term rental property when you’re not using it.

If this is on your bucket list, then here are some things you need to keep in mind.

Firstly, plan how you’re going to use the property and finance it. For example, if you want somewhere to escape to every weekend, can you realistically afford to buy somewhere a few hours away and keep it just for family and friends? Would you consider buying with other family members? Or would you prefer to rent it out to cover costs, and how many weeks rental would you need to rent it to become profitable?

Most holiday homes charge peak rental for school holidays, the summer break or the snow season – times when you probably want to stay there yourself. So, be honest about the trade-offs you’re willing to make.

If you would need to let your property at least part of the time, then location is key. The home will need to be easy to maintain as well as have the amenities and aesthetics that paying guests want. Including things like a BBQ, pool, ceiling fans or heating and comfortable furnishings. All of these can bump up what a rent-worthy property costs to set up and the time you need to commit to it. It’s a good idea to check out other rentals in your preferred areas to see what successful holiday lets offer and what fees they charge.

Lenders and the ATO view a holiday home as an investment property – whether or not you rent it out. Lenders want a bigger deposit and higher interest rate than for an owner-occupied property. While you may be able to use the equity you have in your main home for the deposit, lenders still want to see that you can service the loan. Some take proven short-term rental income from the property into account. Otherwise, they only accept long-term lease rental projections. We can review your circumstances and prepare an investment plan to help identify properties that may have a greater chance of being approved by lenders.

You can get an idea of what properties earn on sites such as Airbnb’s AirDNA.i

While it’s true short-term holiday lets could earn much higher rents, the income may not be year-round, even though the property’s ongoing expenses and upkeep are. These include extras like specialised landlord insurance, property listing website costs, regular maintenance, cleaning, utilities and the replacement of household items such as towels and kitchen items. You’ll also need to consider the current council rules for short-term lets. In some areas there are restrictions such as the number of weeks a property can be let. These rules can change and it’s the landlord’s responsibility to stay up-to-date.

The good news is that you can claim property-related costs as a tax deduction. If you’re only renting for part of the year, then the deductions are for the rentable period only. And, if you’re thinking of buying the property through your Self-Managed Super Fund, remember that it can only be used for maximum income generation and not family use. It’s a good idea to check with the ATO website or your accountant about the tax rules around rental income and any capital gains you’d have to pay if you sell.ii

While a holiday home can become your own piece of paradise and create many happy memories, organising how to finance it takes preparation.

Please get in touch if you’d like to chat through your options so we can start getting things organised for a successful completion on your dream holiday home.

It’s challenging to get a foot on the property ladder and coming up with a large enough deposit can seem like an impossible task at times. One way of increasing your savings is to boost the amount of money you have coming in.

When it comes to boosting your income, every little bit helps, so let’s look at some of the ways you can top up your savings.

The first step is to look at what you are currently earning and see if there is the potential to earn more by working overtime or by increasing your contribution or responsibilities.

Is it time to ask for a raise? With wage growth stagnating, it’s important to present a compelling argument for a salary increase. It’s not just about summoning the courage to have ‘the talk’ with your boss – you need to maximise your chances of receiving that increase. Think about how you can demonstrate where you have added value, taken on more in your role, or achieved cost or efficiency savings for the company. It might even be an idea to consider doing further study and developing additional skills that could see you increase your earning capacity.

The employment market has swung in favour of job seekers of late so it can be a good time to see what else is on offer as a way of increasing your income. In fact, data shows workers who move jobs received pay rises of between 8 per cent and 10 per cent, while research out of the Reserve Bank of Australia suggests a more modest 5 per cent pay rise for switching jobs is in the normal range.i

On a cautionary note – consider your overall career objectives and don’t just jump ship for more money. You don’t want to move to a higher paying job to find that it makes you miserable.

We all have stuff lying around that we don’t need that can generate extra income and ‘one man’s trash is another man’s treasure’. Sites that are good for selling items online include Facebook marketplace, Gumtree and Ebay and you may also want to consider second hand markets in your local area or having a garage sale. Make sure you do your research and know what things are worth as you don’t want to give away a sought-after collectable for a song when it’s worth a bomb!

It’s also possible to get income from renting out your stuff you are not using. Do you have tools in the garage that someone would pay to access? Or camping equipment that others would want to use for their get-away? Australian company Releaseit provides a renting platform where you can list your items and accept booking requests from members of the public.

A side hustle does not have to be a second job. Think about what skills you have that may be marketable. For example, are you a whizz with words? If so, you could earn some money writing cover letters and CV’s for job applicants. If you are a gardening green thumb you might be able to help others with their garden design and plant selection. Or if you are creative, selling your work on a platform like Etsy can be financially worthwhile. Even just sharing your opinion can earn you money as participating in paid market research can earn up to $100-$150 per session. ii

Boosting your income is a great way to reach your property goals faster than focusing solely on saving but saving is still an important part of getting your deposit together. Paying any extra income into a dedicated account can make sure you don’t touch it.

It’s also helpful to have a firm figure in mind to be aiming for, so please reach out if we can be of assistance in exploring your borrowing capacity and options.

i https://www.afr.com/policy/economy/want-a-pay-rise-then-you-should-switch-jobs-20220330-p5a9ds

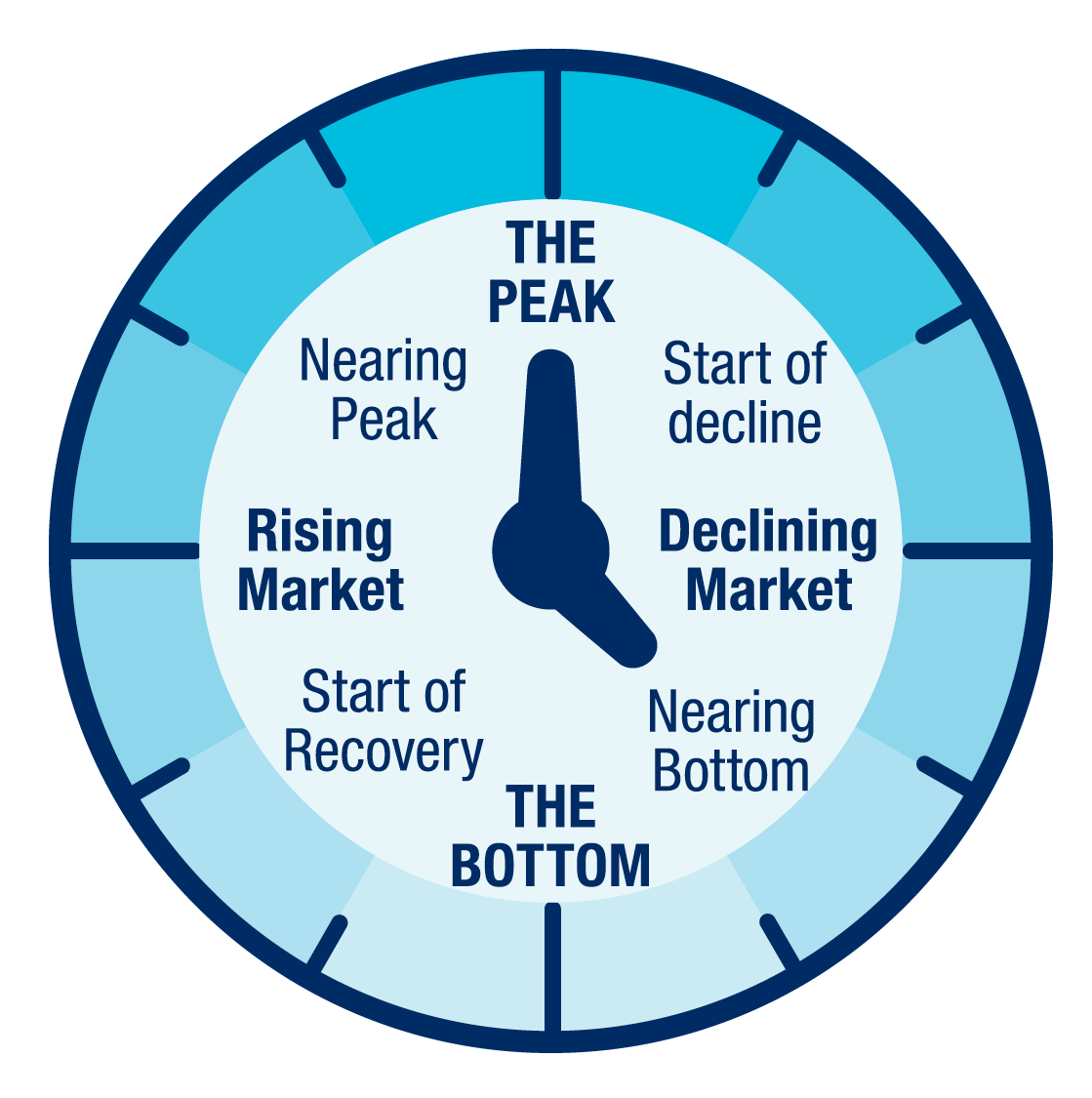

Property investors say that succeeding in real estate is all about timing. Buying at the bottom and selling at the top is easier said than done as there is no easy way to predict exactly when the market is at its peak or trough.

Many real estate experts agree that “time” is everything and it’s more about “time in the market” rather than “timing the market”.

Some real estate analysts use a clock analogy to explain market cycles. The hands moving around the clockface represent where local markets are, at any one point in time.

While the idea of a property clock is logical, the notion of a top and a bottom should be taken at face value.

Experts break down the major capital city performance into “house” and “unit” markets and refer to “regional” figures separately, consolidating hundreds of regional cities and towns into one collective data group.

Cities and towns might be heading one way as a whole but dig deeper and some suburbs can be running their own individual race.

Buyers and sellers should narrow their research to fit their own personal circumstances. The big picture is great, but knowing exactly what is happening where you plan to buy, or sell is more relevant.

During the pandemic, people were looking to get out of the city and choosing to move to regional areas with more space and tranquility as they worked from home.

Interest rates were at record lows allowing some people to secure their dream property. As a result, inner city apartments were out, as people were opting for larger homes meaning houses and regional properties boomed.

In early 2022, many locations moved from the “12 o’clock” spot transitioning away from their market peak. Houses started to become even more unaffordable for many and with interest rates rising swiftly, the desire (and the ability) to pay top dollar dropped.

Apartments gradually started coming back into favour and less demand for high-priced houses saw values slip. It’s not yet determined whether the property market has reached the “6 o’clock bottom”. Unfortunately, pinpointing when values hit a trough is usually declared once the moment has passed.

Australia has a diverse property market with varying cycles. Although, as a population we might experience the same external economic factors – such as inflation pressures and interest rate rises – how each of them impact each corner of the country, can vary greatly.

Experts cannot predict exactly how long each cycle will be or the extent of the rises and falls. For example, when Covid hit many economists were signalling a property market crash – the market proved them wrong.

Sophisticated property investors look for real estate in desirable locations that may appear more likely to hold their value and increase over time.

“Time” can also refer to the right time for you as a buyer as you need to have your financial ducks in a row to purchase a property.

Whether you’re an investor or a homebuyer, holding out to buy at the bottom means you may risk missing out on time in the market because as history has shown us – the longer you hold a home, the more valuable it may become.

To talk about the right time for you to make your next step onto the property ladder, speak to us today.

The key to achieving goals is to identify them – make them quantifiable and put a plan in place to reach them.

Entering the property market as a first home buyer can be exciting and daunting, and saving for the deposit can be hard. However, the government has introduced a few grants that could help eligible first home buyers.

Whether you’re new to investing in property or building your portfolio, your goals should take into account your investment strategy. Do you want to be negatively geared to generate wealth or are you investing in property to create a passive income stream for retirement.

Larger homes, are typically more expensive; therefore, factor this in when setting your goals and understand how this may impact your budget – will you need to make sacrifices to your current lifestyle to service the loan?

There are many different approaches when it comes to goal setting. You’ve likely heard of SMART goals, which are Specific, Measurable, Achievable, Relevant and Time-Bound.

Identify each of your goals and consider what steps you need to put in place to achieve them.

As you begin setting your property goals, think about how these goals will influence your family’s day-to-day life, as this can impact your decision making.

If you’re a first home buyer, identify how much you will be able to borrow, as this will determine how much deposit you’ll need and whether you’re eligible for any home owner grants. Other costs that may be associated with purchasing a home can include a conveyancer/solicitor as well as building or pest inspections. Plus the cost of furnishing the home, so it’s important to understand exactly how much your initial outlay will be.

For the investor, you might be working towards a specific amount in passive income you want to generate, or you may want to own a set number of investment properties by a certain age.

If you have equity in your current home, you could use that to purchase an investment property, or perhaps buy a property off the plan, as these properties can sometimes be less expensive than an established home.

It’s also important to factor in the potential rental returns in the area you are looking to buy. Investment properties require regular maintenance, so having an emergency fund could be a good idea.

The upgrader may have a floorplan in mind or be looking to move to a new area. Again, factor in how you are going to service the loan and other costs associated with the upgrade. You’ll probably need to purchase additional or different furniture to fill a larger home.

Sometimes we can lose our way with our goals by setting a framework that is unrealistic. If you’ve set goals that are unachievable – especially when it comes to budgeting – it can be challenging to see them through. Perhaps you decided to save for a deposit but are finding the lifestyle sacrifices are too much. Leaning on your support network as a reminder as to your ‘why’ can be helpful.

Visualising your goals can also be powerful. Imagine getting the keys to your investment property or moving into a bigger house – these thoughts can often keep you motivated. Tracking your progress regularly will not only keep you working towards your property goal, but it can help you recognise the small wins and where you might need to adjust your goals.

And finally, be accountable – share your goals with others so you can feel more motivated to reach them.

If you are considering purchasing a property in 2023, we are here to help so contact us today.

Despite a widespread dwelling price correction – down –3.5% nationally for the quarter to 30 November – getting onto the property ladder is still as challenging as ever.i

To help ease the burden, both the Federal and State governments are assisting with grants, schemes and tax exemptions. However, with so many schemes on offer it can be hard to compare and to find the most appropriate for your situation.

In the October Federal Budget, prospective first-home buyers were thrown a new lifeline with the National Housing Accord.

Treasurer Jim Chalmers announced an accord between all levels of government, institutional investors and the construction industry, which would see 1 million new “well-located” homes built over five years, starting in 2024.

The budget committed an initial $350 million in additional funding for 10,000 affordable homes, on top of existing commitments. State and territory governments would match the 10,000 home pledge, meaning 20,000 dwellings will be delivered per year.

Each state and territory has its own First Home Owner Grant with different eligibility requirements.

In some states, first-time purchasers can receive a one-off payment when buying a newly built home or purchasing vacant land, while in other states, the grants have been replaced by stamp duty (also known as transfer duty) concessions. To understand what’s on offer in your state or territory, visit First Home Scheme.ii

While lenders traditionally expect first-home buyers to provide a 20% deposit (or less with Lender’s Mortgage Insurance) this scheme helps buyers with a 5% deposit. The Government will guarantee 15% for eligible purchasers.

The initiative (formerly First Home Loan Deposit Scheme) has pledged 35,000 spots until 30 June 2023.

Single first-home buyers can earn up to $125,000, while couples are capped at $200,000 a year, depending on eligibility. Limits on purchase prices also apply and can be found at National Housing and Finance Investment Corporation.iii

This package isn’t just for first-home buyers. The Federal Government will co-purchase a property with eligible homebuyers. The buyer requires a 2% deposit, and the Government will contribute up to 40% towards the purchase.

Homeowners can choose to either buy the portion of the home (co-purchased by the Government) during the life of the loan or sell it and repay any money owed along with the share of any capital gain. This scheme is due to commence from July 2023.

From 1 October 2022 – 30 June 2023, 10,000 new places became available in this scheme for regional first-home buyers.iv The Federal Government is pledging to guarantee up to 15% of a home’s value so local first-home buyers can buy with a 5% deposit.

This program is aimed at getting more Aussies into their own home – whether they’re a first-home buyer or not, with 5000 places created for single parents with at least one dependent.v

Eligible buyers will need a 2% deposit with the Government guaranteeing up to 18% of the property’s value to meet the 20% lenders’ standard.

For most first-home buyers, the deposit is the biggest hurdle. Eligible first-home buyers can access some of their superannuation to put towards a home deposit.

While this initiative offers you a way to “beef up” your deposit, it’s important to note you’ll be dipping into future retirement savings.

First-home buyers can release up to $15,000 each financial year to a maximum of $50,000. Further information can be found on the ATO website.

Working out which schemes you can apply for will take some research and we can assist.

i https://www.corelogic.com.au/__data/assets/pdf_file/0024/12777/2212-CoreLogic-HVI-Nov22-Final.pdf

ii https://www.firsthome.gov.au/

iii https://www.nhfic.gov.au/support-buy-home/family-home-guarantee

iv https://www.nhfic.gov.au/support-buy-home/regional-first-home-buyer-guarantee

v https://www.nhfic.gov.au/support-buy-home/family-home-guarantee

Stay up to date with the latest developments in the property market over the past month. Our video takes you through an overview of the state of...

During the cooler months of the year it’s easy to get into ‘hibernation habits’. Comfort food is much more appealing when it’s awful...