Why Do Interest Rates Rise During Inflation?

When inflation climbs, interest rates typically rise because central banks - like Australia's Reserve Bank - deliberately make...

Yesterday’s news about Commonwealth Bank lifting their 1, 3, and 5-year fixed interest rates has left many Australian property buyers and investors wondering: should I fix my rate, or what does it mean when banks move before the RBA even meets? The answer is about more than just numbers – it’s about understanding the chess game between the major banks, the Reserve Bank, and your unique property investment strategy.

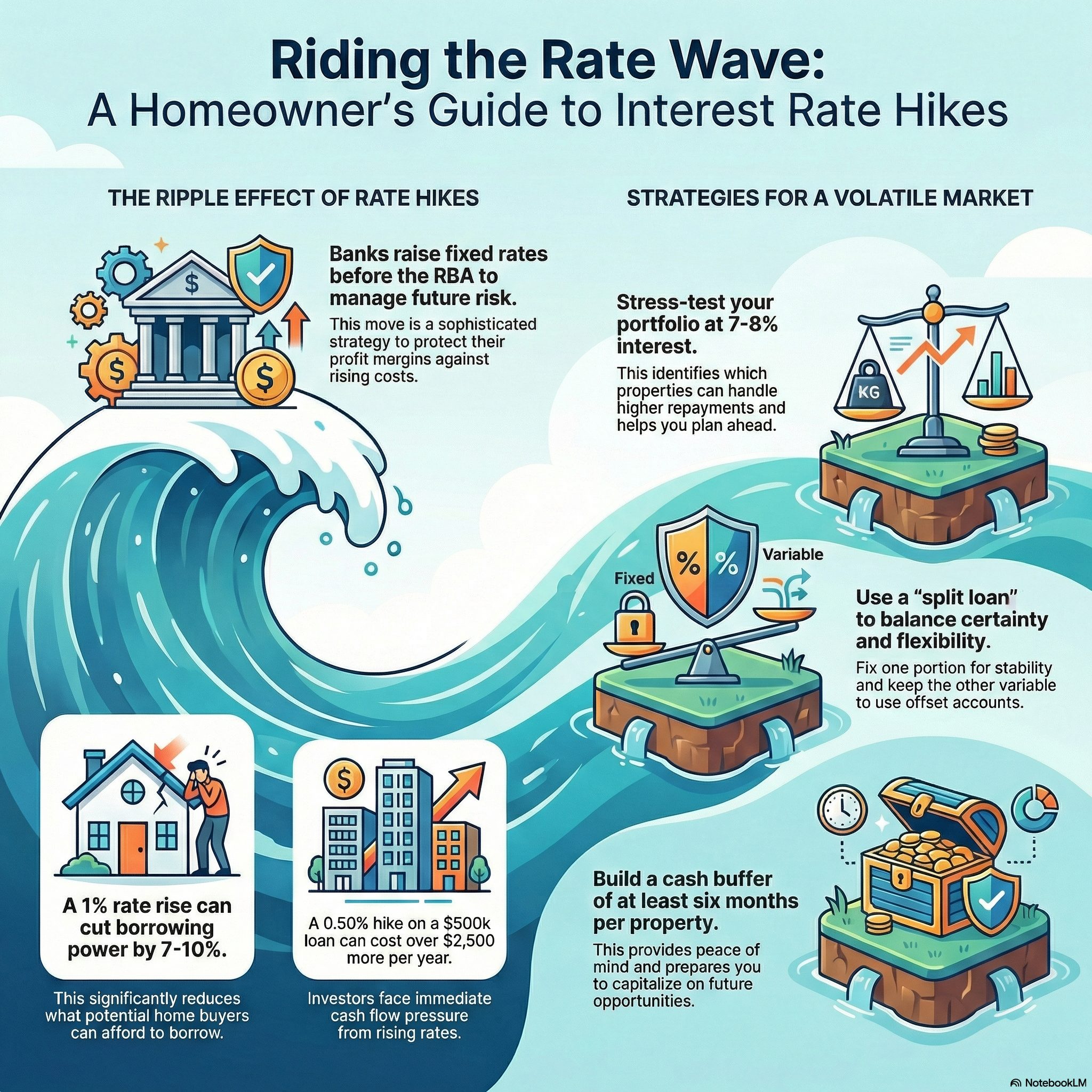

When major lenders like CommBank preemptively increase fixed rates, they’re essentially building in future RBA changes before they happen. This move isn’t speculation; it’s part of a sophisticated risk management approach based on leading economic indicators, inflation figures, and the performance of the bond market. For both buyers and investors, these changes introduce challenges and highlight opportunities that could impact your property ambitions.

Banks do more than mirror the RBA’s cash rate changes; they anticipate them. CommBank’s latest moves on 1, 3, and 5-year fixed rates underscore their expectations of an RBA rate hike in the near term. By increasing fixed rates in advance, banks aim to protect profit margins against rising funding costs that are often driven by bond market volatility and shifting economic forecasts.

Wholesale funding markets respond immediately to expectations of higher interest rates. As a result, banks feel the increased cost before the RBA makes its next move. Raising fixed rates early allows major lenders to maintain competitive variable rates while covering their costs of funds.

This environment – with the RBA cash rate at 3.60% and more hikes likely in 2026 – reflects a market bracing for further tightening. CommBank’s actions send a clear message: upward rate pressure is real, driven by persistent inflation and strong employment data.

For property investors, bank moves are a valuable early warning. Increases in fixed rates often precede RBA action by several months, offering an opportunity to review your loan settings, lock in current variable rates, or prepare for stricter lending criteria.

RBA movements have direct consequences for your borrowing power. Lenders usually assess home loan applications at a serviceability buffer 2–3% above the interest rate, meaning stress-testing is done at rates of 6–7% (or higher). Every 1% increase in rates can reduce your borrowing capacity by 7–10%.

For example, a buyer qualified for a $600,000 loan might see this drop to $540,000 or $550,000 after a series of 0.50% RBA increases. This serviceability reduction particularly affects first home buyers and upgraders in costly locations such as Sydney and Melbourne.

Another complexity: property prices tend to trail changes to interest rates by 6–12 months. This means buyers may see their borrowing power fall before property values adjust, creating a window where competition eases but opportunities arise for those with pre-approval or significant deposits.

Regional markets with more affordable homes tend to resist these changes better than premium metro suburbs, where serviceability constraints are felt more deeply. Targeting growth markets and timing your property search is key when RBA rate decisions loom.

For investors, rising interest rates deliver an immediate hit to cash flow. Those with interest-only loans, popular for tax reasons, will notice the impact sooner, as there is no principal reduction to offset higher interest bills.

Here’s a real-world scenario: An investor with a $500,000 interest-only loan at 5.5% faces a monthly repayment of roughly $2,290. If rates climb by 0.50%, that becomes $2,500, or $2,520 more per year per property. Across a portfolio, these increases add up quickly.

Strong rental market conditions offer some relief, given historic low vacancy rates and migration-driven demand. In many locations, rental yields are up 8–12% year-on-year. This rent growth can help steady cash flow, but the pressure from rising interest costs remains.

Success in this environment rests on building a robust portfolio. Properties in high-demand rental markets with quality tenants are more resilient to rate hikes. Stress-test your portfolio at 1–2% above your current loan rates to pinpoint properties that may struggle if interest costs continue rising.

Adopting the right loan structure is essential in times of rate volatility. Rather than simply choosing between fixed and variable, consider a split loan approach. By dividing your loan between fixed and variable components, you benefit from both certainty and flexibility.

A popular strategy is a 50/50 split. This enables you to use offset accounts against the variable portion to reduce interest, while the fixed portion locks in part of your repayments for budgeting certainty.

Interest-only periods also require careful planning. As rates rise, consider if switching some properties to principal and interest repayments proactively could help you manage future repayment shocks and accelerate equity growth during periods of uncertainty.

Offset accounts are even more valuable in these conditions. For example, a $50,000 offset at 5.5% interest saves $2,750 a year, increasing to $3,250 if rates hit 6.5%. Prioritising building your offset is often wiser than extra repayments, as this maintains flexibility and keeps your funds accessible.

The decision to fix your rate or remain variable depends on more than just interest rate predictions. It’s about understanding your risk appetite, managing cash flow, and having an adaptable property investment strategy. While fixed rates for investors sit at 6.0–6.5% and variables at 5.8–6.2%, this comparison doesn’t tell the full story.

If the RBA raises rates by another 0.50–0.75% over 12–18 months, variable rates will quickly overtake current fixed offers. However, fixed loans limit your ability to use offset accounts and can make refinancing more expensive if rates fall again.

Breakeven analysis shows that fixing makes sense if you expect rates to rise by more than 0.25–0.50% during your fixed term. The market and bank actions suggest this is likely, but locking in everything could cost you flexibility if market conditions change rapidly.

Most investors opt for a balanced approach: fix debt on properties with tighter cash flow and use variable rates for those with strong rental returns. This strategy delivers protection where it is needed and keeps you ready to benefit if things improve.

Successful property investors don’t rely on guesswork – they plan for a range of scenarios. With ongoing RBA and CommBank moves, annual reviews won’t cut it; assess your portfolio each quarter to stay ahead.

It’s easy to feel anxious when headlines about rate hikes land—but I’ve been in your shoes. Back in 2023, I woke up to an email from my lender. They’d quietly lifted my fixed rate, ahead of any official RBA news, and suddenly my monthly repayments jumped by hundreds overnight. I’ll admit, I spent a few sleepless nights tallying numbers and worrying about what-ifs. But out of that anxiety came something game-changing: I realised the value of running my own “rate stress test” every quarter, rather than waiting for big bank news. I restructured my loans, set up a buffer fund, and reviewed each property’s cash flow as if rates were already a full 2% higher—just like the scenario in today’s post. Not only did this give me back my peace of mind, but when the next round of rate rises hit, I was ready. No more panic, just small adjustments and the confidence that my portfolio—and my sleep—could weather whatever changes came next. If you’re staring at potential increases now, take it from me: a little proactive planning makes all the difference.

Stress test each property at interest rates of 7–8% including all running costs like council rates, insurance, maintenance, and vacancy buffers. If a property can’t handle higher repayments, act early by reviewing rents, refinancing, or considering a sale.

Build up at least a six-month cash flow buffer per property. This gives peace of mind and could let you capitalise on distressed buying opportunities, should they emerge.

Active management and frequent portfolio reviews are your best defences in a volatile market. By staying agile and prepared for a range of outcomes, you can keep your investments robust and potentially take advantage of opportunities that others may miss.

Understanding that banks like CommBank raise fixed rates early provides valuable market insight. Take these moves as signals to review your loan arrangements and restructure as needed.

Rate changes bring both risks and opportunities. The investors who will thrive are those who maintain strong cash flows, prudent debt strategies, and ample cash reserves. Don’t let rate uncertainty freeze your property objectives; strengthen your fundamentals and adapt your strategy to changing conditions.

Do you want to ensure your property portfolio is ready for the next round of RBA changes? Now is the time to stress-test your loan setup, review your repayment buffers, and structure your portfolio to weather whatever lies ahead.

Ready to stress-test your property portfolio against rising rates? Book a mortgage review call today and get personalised guidance on optimising your loan strategy for the current market.

Should I fix my investment property loan rates now?

Consider fixing part of your loan – especially on properties where cash flow is tight – and keeping a variable portion for flexibility. A common option is a 50/50 split to balance certainty and opportunity.

How much could my repayments increase if rates rise by 0.50%?

For a $500,000 loan, repayments may rise by about $210–$250 a month, depending on your interest rate and loan structure. Interest-only loans experience the full increase immediately.

What can I do if higher rates push my property into negative gearing?

Review your rental income to see if an increase is possible, consider switching to principal-and-interest repayments if you’re currently on interest-only, and evaluate whether holding or selling best serves your long-term goals.

Are there upsides to rising rates for property investors?

Yes. Higher rates can improve interest earned on deposit accounts, reduce competition from speculative buyers, potentially lift rental yields, and create opportunities to buy well-priced properties from motivated sellers.

When inflation climbs, interest rates typically rise because central banks - like Australia's Reserve Bank - deliberately make...

Market volatility is inevitable in property investing, but it doesn't have to derail your wealth-building plans. Most successful...