Why Do Interest Rates Rise During Inflation?

When inflation climbs, interest rates typically rise because central banks - like Australia's Reserve Bank - deliberately make...

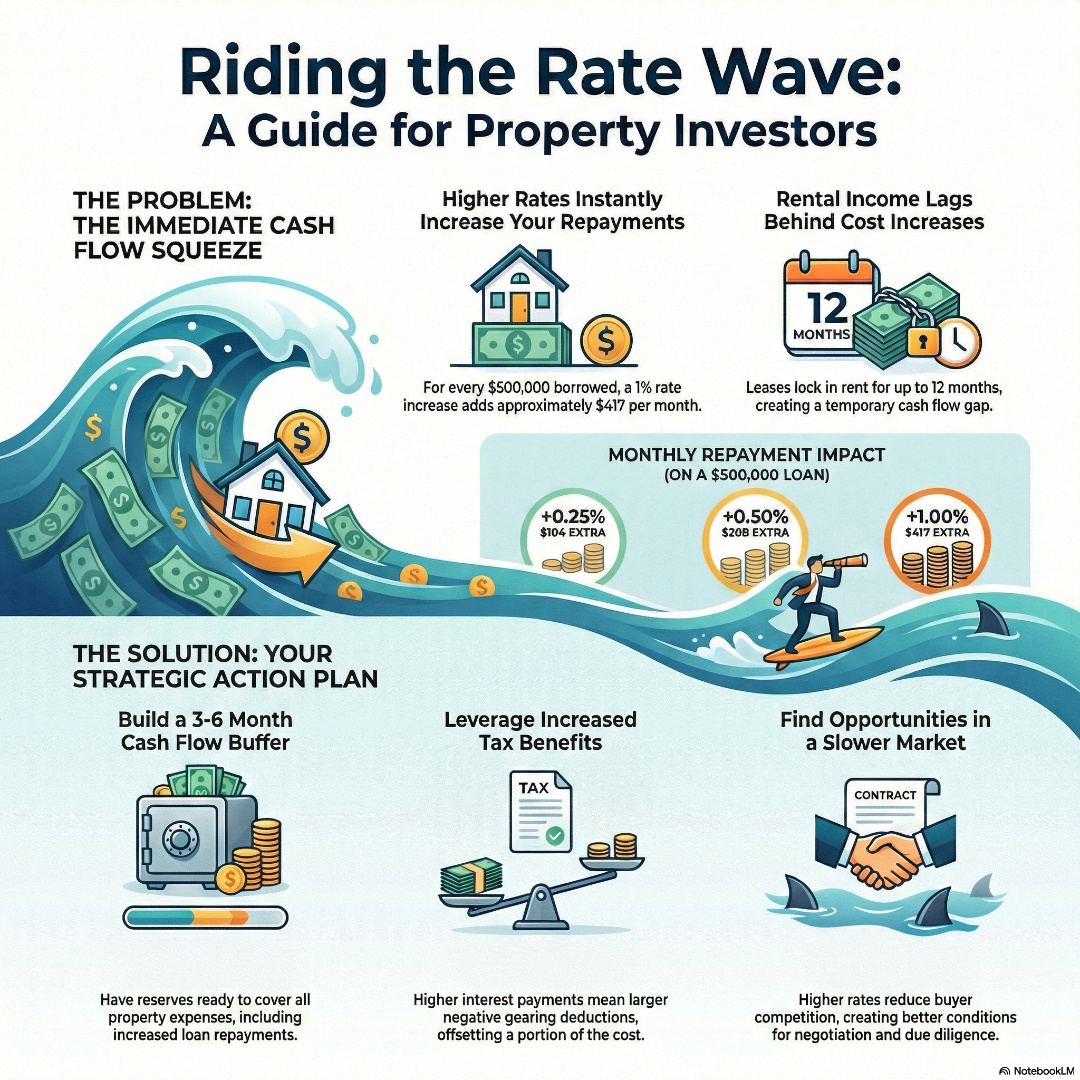

When interest rates rise on your investment loans, your monthly repayments increase immediately, squeezing your cash flow and potentially turning a positively geared investment into a negatively geared one. For every $500,000 borrowed on an interest-only investment loan, a 1% rate increase adds approximately $417 per month to your repayments. The key to weathering rate rises lies in understanding the exact financial impact and having proper cash flow buffers in place before rates move.

Rising interest rates deliver an instant blow to your investment property cash flow. Unlike your family home where you might absorb higher repayments through budget adjustments, investment properties operate on tighter margins where every dollar counts.

When the Reserve Bank increases the cash rate, lenders typically pass on the full increase within weeks. If you’re paying 6% interest-only on a $500,000 investment loan, your monthly repayments sit at $2,500. A jump to 7% pushes this to $2,917, an additional $417 every month that must come from somewhere.

The rental income from your property won’t increase immediately to match this higher cost. Most lease agreements lock in rent for 12 months, meaning you’ll likely face several months where your property’s cash flow deteriorates significantly. This is where many inexperienced investors panic and make costly decisions.

Smart investors prepare for this scenario by maintaining cash reserves specifically for rate rises. The general rule is holding 3-6 months of total property expenses (including the potential increased repayments) in a separate account as a financial buffer.

Understanding exactly how much extra you’ll pay helps remove the fear and uncertainty around rising rates. Here’s how different rate increases affect various loan amounts on interest-only investment loans:

These figures assume interest-only loans, which most property investors use to maximise tax deductions and maintain cash flow flexibility. Principal and interest loans experience similar short-term impacts, though the long-term compounding effect differs.

For precise calculations with your specific loan details, use online borrowing capacity calculators that factor in your exact interest rate, loan term, and repayment type.

Rate increases don’t just impact your monthly budget, they reshape your entire investment landscape. Higher borrowing costs reduce your purchasing power for future properties, as lenders assess your serviceability based on current rates plus a buffer.

If you were planning to buy a second investment property, rising rates might push that timeline out by 6-12 months while you rebuild your borrowing capacity. This delay isn’t necessarily negative, it provides time to strengthen your financial position and potentially find better property deals as market activity slows.

Existing investments benefit from increased negative gearing deductions. Higher interest payments mean larger tax deductions, effectively reducing your after-tax cost of the rate rise. For investors in the 32.5% tax bracket, that extra $417 monthly payment on a $500,000 loan only costs $281 after tax benefits.

The key is maintaining perspective. Property investment success comes from capital growth over 7-10 year periods, not monthly cash flow optimisation. Rate cycles are temporary, but well-located properties in growth areas continue appreciating regardless of short-term borrowing costs.

Experienced investors often view rising rate environments as opportunity creators rather than threats. As borrowing becomes more expensive, competition for investment properties decreases, potentially creating better buying conditions.

Higher rates typically cool overheated markets, giving investors time to conduct thorough research without the pressure of auction bidding wars. Properties may stay on the market longer, allowing for more detailed due diligence and potentially better negotiation positions.

This environment favours investors with strong cash positions and existing equity. While new investors struggle with serviceability, established investors can leverage their portfolio calculator results to identify expansion opportunities others can’t access.

Consider switching investment strategies during high-rate periods. Instead of pursuing maximum leverage, focus on properties with higher rental yields that maintain positive cash flow even with elevated borrowing costs. Regional properties often offer better rental returns during these periods.

Successful navigation of rising rate periods requires proactive planning rather than reactive responses. Start by stress-testing your current portfolio at rates 2-3% above current levels. Can you service all loans if rates reach these levels? If not, consider reducing debt or building larger cash reserves now.

This proactive approach is something I live by, and it’s saved me-and my clients-a fortune. When the market started shifting, I didn’t wait for my lender to send a courtesy email. I immediately called my own bank. My initial rate was sitting around 5.33%, but I knew that wasn’t the best they could do. After some persistence, and pointing out the rates other banks were offering, I negotiated them down to 3.13%. That single phone call saved me thousands of dollars a year in repayments. I apply this same fierce negotiation for all my clients, ensuring they don’t simply accept the default loan offer. Too many investors leave significant money on the table just because they’re afraid to ask, but that one moment of courage can be the difference between a stressed cash flow and a comfortably geared portfolio.

Review your loan structures with a mortgage specialist who understands investment property financing. Interest-only periods, offset accounts, and redraw facilities provide flexibility during challenging rate environments. Some investors benefit from fixing portions of their loans to create certainty around future repayments.

Build relationships with multiple lenders before you need them. Having pre-approved refinancing options provides negotiating power with your current lender and backup plans if your financial circumstances change.

Most importantly, maintain your long-term perspective. Australian property has delivered positive returns over every 10-year period in recorded history, despite numerous rate cycles. The investors who succeeded weren’t those who timed the market perfectly, they were those who bought well-located properties and held them through various economic conditions.

Focus on acquiring properties in areas with strong fundamentals: population growth, infrastructure development, and economic diversity. These properties continue appreciating even when short-term borrowing costs increase, ensuring your strategy remains profitable over the full investment cycle.

Rising interest rates on investment loans create immediate cash flow challenges but don’t fundamentally change the long-term viability of property investment. By understanding the precise financial impact, maintaining adequate reserves, and viewing rate rises as part of normal investment cycles, you can protect and even strengthen your portfolio during these periods.

The key differentiator between successful and unsuccessful property investors isn’t avoiding rate rises, it’s being prepared for them. Book a mortgage review call today to stress-test your current loans and optimise your portfolio structure for whatever interest rate environment lies ahead.

How much extra will I pay each month if rates rise by 0.5% on my $400,000 investment loan?

On a $400,000 interest-only investment loan, a 0.5% rate increase will cost approximately $167 extra per month. This calculation uses the formula: (Loan Amount × Rate Increase) ÷ 12 months. For principal and interest loans, the impact varies depending on your remaining loan term, but generally, the monthly increase would be slightly less than on an interest-only loan.

Can I switch from principal and interest to interest-only if rates rise significantly?

Yes, many lenders allow existing borrowers to switch to interest-only repayments, typically for 1-5 year periods. This can provide immediate cash flow relief during high-rate environments, though you’ll need to meet current lending criteria and the property must remain investment-focused. Most lenders will reassess your financial situation before approving this change, so maintaining good credit and income documentation is essential.

Do rising interest rates affect my negative gearing tax benefits?

Rising rates actually increase your negative gearing deductions because higher interest payments create larger tax-deductible expenses. For investors in higher tax brackets, this can offset 30-45% of the additional interest costs through reduced tax obligations. It’s important to consult with your accountant to ensure you’re maximising these deductions and maintaining proper documentation of all investment property expenses.

Should I sell my investment property when interest rates start rising?

Selling purely due to rising rates is rarely optimal, as you crystallise any capital losses and exit the market when conditions may improve. Instead, focus on improving cash flow through rent increases, refinancing to better rates, or temporarily switching to interest-only repayments while maintaining your long-term investment strategy. Most property cycles outlast interest rate cycles, so well-selected properties typically recover and continue growing after temporary rate increases.

When inflation climbs, interest rates typically rise because central banks - like Australia's Reserve Bank - deliberately make...

Market volatility is inevitable in property investing, but it doesn't have to derail your wealth-building plans. Most successful...