How to Reduce Your Monthly Mortgage Payments

There is no single magic switch, but there are several proven levers you can pull to reduce your monthly mortgage payments - and the right one...

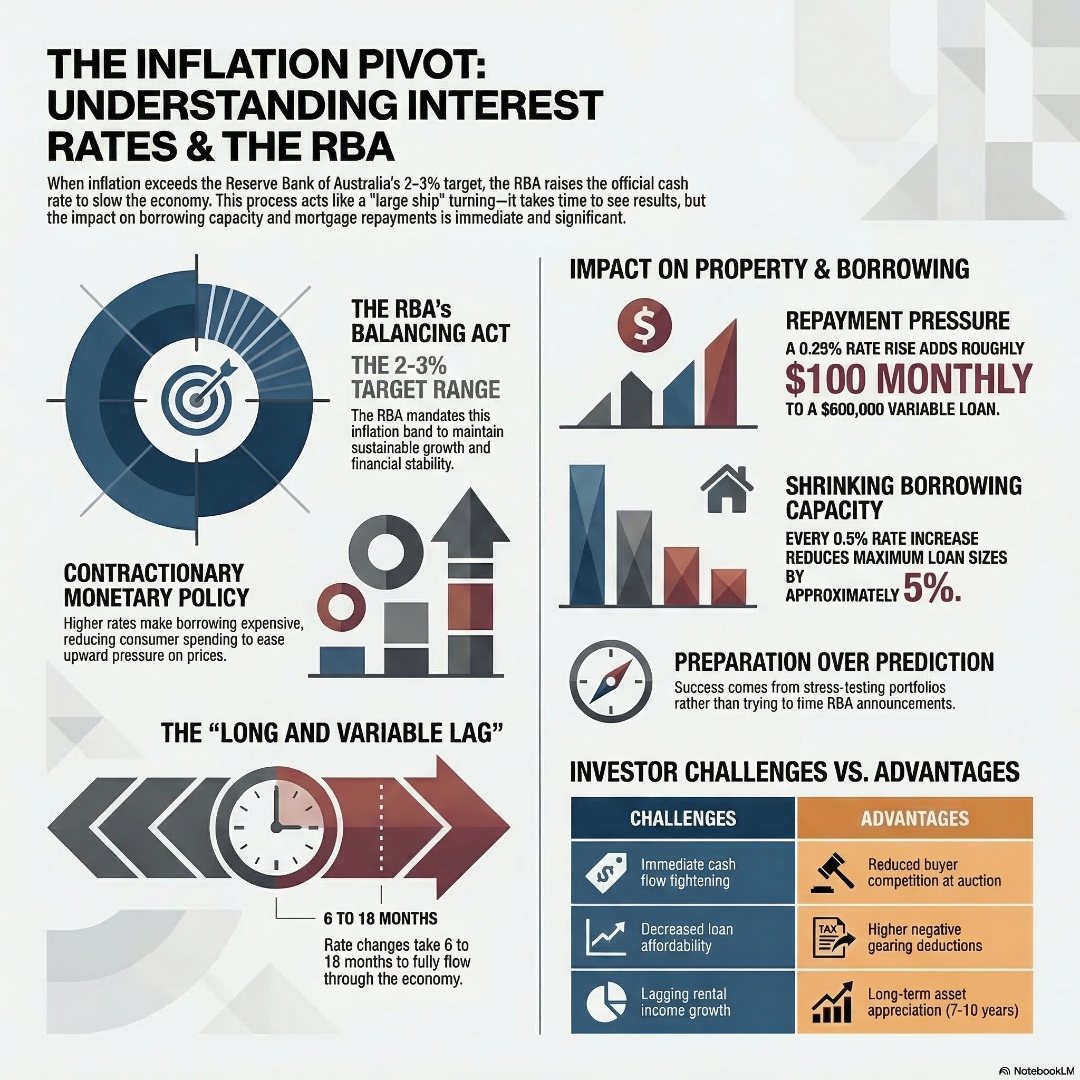

When inflation climbs, interest rates typically rise because central banks – like Australia’s Reserve Bank – deliberately make borrowing more expensive to slow spending, reduce demand, and bring prices back under control. The RBA targets an inflation rate of 2 to 3% on average, and when inflation pushes beyond that range, raising the official cash rate is its primary lever to pull the economy back into balance. Understanding why interest rates rise during inflation is not just an economics lesson. It is the foundation for every smart decision you will make about your mortgage, your property portfolio, and your long-term financial security.

Imagine you have $100,000 sitting in a savings account earning 2% interest per year. Now imagine inflation is running at 7%. On paper, your balance is growing. In reality, the purchasing power of that money is shrinking by roughly 5% every year. That new car, that renovation, that investment property deposit – all of them are costing you more in real terms even though the number in your bank account keeps ticking up.

This is the silent damage inflation causes. It is not just about prices at the supermarket or petrol stations, though those are the most visible symptoms. Inflation erodes the real value of every dollar you earn, every dollar you save, and every dollar you invest.

For property investors and homeowners watching the RBA’s every move, this dynamic is critical. Because the moment inflation gets away from the Reserve Bank’s target range, it activates its most powerful tool: the interest rate lever.

The Reserve Bank of Australia has one primary mandate when it comes to monetary policy: keep inflation low and stable, within the 2 to 3% target band on average over time. The RBA considers this the essential foundation for everything else it values – strong employment, sustainable economic growth, and financial stability.

So when inflation breaks out above that target, the RBA raises the official cash rate. The logic is direct.

When borrowing becomes more expensive, people and businesses spend less. A homeowner whose monthly repayments jump by $300 thinks twice about that kitchen renovation. A business facing higher loan costs delays expanding. Consumers postpone big purchases. All of that reduced activity takes pressure off demand – and when demand falls, the upward pressure on prices eases.

This is called contractionary monetary policy. It is the RBA tightening the screws on the economy, deliberately slowing it down just enough to bring inflation back to target without tipping the country into recession. It is a careful calibration, and the RBA is very deliberate about it.

The key thing to understand is that this is not punitive. The RBA is not raising rates to hurt borrowers. It is trying to restore balance – to protect the purchasing power of every Australian, including yours.

Here is where it gets genuinely complex, and where many investors get caught off guard.

Interest rate changes do not work immediately. There is a well-documented delay between when the RBA raises the cash rate and when those changes fully flow through to the broader economy. Economists call this the “long and variable lag.”

Think of it like steering a large ship. You turn the wheel, but the bow does not change direction for several hundred metres. The RBA might raise rates in February, but the full economic effect – reduced spending, eased price pressures, lower inflation readings – may not show up clearly until six, twelve, or even eighteen months later.

This creates a genuine challenge for policymakers and for borrowers alike. By the time the effect of rate hikes is visible in the data, the RBA has often already moved multiple times. And for you as a mortgage holder or property investor, this lag means you might feel the pain of rate rises long before you see the benefit of inflation coming back under control.

It also means timing the market around rate cycles is notoriously difficult. The best protection is not trying to predict the next RBA move – it is stress-testing your own financial position against a range of possible rate environments.

Understanding how RBA rate changes directly impact your mortgage can help you build that buffer into your planning before the next announcement catches you off guard.

Let’s bring this back to something tangible.

When the RBA lifts the cash rate by 0.25%, lenders typically pass the increase through to variable rate mortgage holders within days. On a $600,000 variable rate loan, a 0.25% increase adds roughly $95 to $100 to your monthly repayments. A series of four or five consecutive hikes – which is exactly what happened in Australia during the 2022 to 2023 rate cycle – can add $400 to $600 per month to your repayments on that same loan.

That is not abstract. That is real budget pressure, and it arrives fast.

Fixed-rate borrowers are temporarily shielded from this, but only until their fixed term expires. Many Australians who locked in ultra-low rates during 2020 and 2021 faced a sharp adjustment when those terms rolled over into a very different rate environment.

The broader implication for property investors is significant. Rising rates reduce borrowing capacity – often by more than people expect. For every 0.5% increase in assessment rates, a borrower’s maximum loan size typically shrinks by around 5%. If you are planning to purchase an investment property, that contraction in borrowing power needs to be factored into your timeline and your deposit strategy.

For more detail on the specific numbers, see our guide on what happens if interest rates rise on my investment loans.

I will be honest with you – I am not immune to this pressure myself. When I first started hearing serious talk about the RBA hiking rates aggressively back in 2022, my stomach dropped. I have property loans. I know what a 3% movement does to a portfolio. For a moment, I felt exactly what many of you are probably feeling right now: a flash of real, visceral fear. But here is what twenty years of working with Australian property investors has taught me. The borrowers who came out the other side of every single rate cycle I have lived through were not the ones who predicted the RBA’s next move. They were the ones who had quietly done the unglamorous work beforehand – built cash buffers, reviewed their loan structures, and bought properties with genuine fundamentals rather than hope. In fact, when I looked back over a decade of my own mortgage clients’ results, nearly 70% had built over $100,000 in equity, even through tightening lending rules and rate volatility, because they had planned conservatively from the start. The rate cycle will pass. It always has. But the gap between the investors who thrive and the ones who are forced to sell at the worst possible moment almost always comes down to one thing: preparation, not prediction.

Rising interest rates do not exist in isolation. They interact with property values, rental demand, and construction costs in ways that matter deeply to property investors.

When rates rise sharply, property prices in overheated markets often soften. Buyers can borrow less, competition at auctions thins out, and vendor expectations adjust. This is not necessarily bad news if you are a patient investor with a clear-eyed view of the long game. Slower markets create negotiating room that frenzied markets do not.

At the same time, inflation itself can support property values over time. When the cost of materials, labour, and land rises, the replacement value of existing property increases. This is one of the reasons property has historically served as a reasonable long-term hedge against inflation – the underlying asset tends to reprice upward along with the broader cost of goods and services.

The key distinction is time horizon. In the short term, rising rates and inflation create uncertainty and cost pressure. Over a seven to ten year period, well-selected properties in areas with strong fundamentals have consistently delivered positive returns through every rate cycle Australia has experienced.

Understanding how to position yourself strategically – with the right loan structure, appropriate buffers, and properties in locations with genuine growth drivers – is what separates investors who thrive through rate cycles from those who are forced to sell at the worst possible time.

For context on how interest rates interact with your broader investment strategy, our article on how interest rates affect property investment strategies goes deeper into that relationship.

Understanding the theory is useful. Knowing what to do with that understanding is what matters.

First, stress-test your current position. Run your mortgage repayments at a rate 2 to 3% above your current rate. Can you still service your loans comfortably? If not, now – before rates move further – is the time to build a cash buffer or review your loan structure.

Second, review your loan type. If you are on a variable rate, consider whether a partial fixed rate arrangement might provide useful certainty for your budgeting. If you are approaching the end of a fixed term, get professional advice early rather than defaulting onto whatever standard variable rate your lender offers.

Third, do not assume your current lender is offering you the best available rate. Competition among lenders remains real even in rising rate environments, and refinancing can sometimes unlock meaningfully better terms – without changing your underlying investment position.

Finally, keep perspective. The relationship between inflation and interest rates is cyclical, not permanent. The RBA raises rates to slow inflation, eventually succeeds, and then eases rates again as the economy stabilises. Every previous rate cycle in Australia’s recorded history has ended. Your long-term investment strategy should be built to survive them all, not just the current one.

The reason why interest rates rise during inflation comes down to one fundamental goal: protecting the purchasing power of every Australian by bringing prices back under control. The RBA uses the cash rate as its primary lever to slow demand, ease price pressure, and restore economic balance. For you as a borrower, property investor, or homeowner, understanding this mechanism means you can plan ahead rather than simply react.

The rate cycle you are navigating today is one chapter in a longer story. The investors who navigate it best are not the ones who guessed the RBA’s next move correctly. They are the ones who stress-tested their position in advance, structured their loans intelligently, and held quality assets through the cycle.

If you are unsure whether your current loan structure is positioned well for the rate environment ahead, the next step is a conversation with an expert. Book a mortgage review call today and get clarity on where you stand – and what you can do to protect and grow your financial position from here.

Why do interest rates rise during inflation in Australia?

The Reserve Bank of Australia raises the official cash rate when inflation climbs above its 2 to 3% target band. Higher borrowing costs reduce spending by households and businesses, which takes pressure off demand and helps bring prices back down. This is the RBA’s primary tool for restoring price stability and protecting the purchasing power of Australians.

How does inflation affect mortgage rates in Australia?

When inflation rises, the RBA typically increases the cash rate, and lenders pass this increase through to variable rate mortgage holders within days. A single 0.25% rate rise adds approximately $100 per month to repayments on $500,000 loan. Sustained inflation can trigger multiple consecutive rate hikes, adding hundreds of dollars monthly to mortgage costs and reducing borrowing capacity for future purchases.

What is the relationship between inflation and interest rates?

Inflation and interest rates move in opposite directions as a matter of policy design. When inflation rises above target, central banks raise rates to slow the economy. When inflation falls back into the target range and economic growth weakens, rates are typically cut. This inverse relationship is the foundation of monetary policy in Australia and most developed economies.

How long does it take for interest rate rises to reduce inflation?

Rate hikes work with what economists call a “long and variable lag.” The full effect of rate increases typically takes six to eighteen months to flow through the economy. This delay is why the RBA often needs to raise rates several times before inflation data shows a clear downward trend – the ship takes time to change course after the wheel is turned.

There is no single magic switch, but there are several proven levers you can pull to reduce your monthly mortgage payments - and the right one...

The first time home buyer mortgage process follows six clear steps: sort your finances, save a deposit, speak to a mortgage broker, secure...