What Do the 2026 Budget Tax Changes Mean for Your Property Investment Strategy in Australia?

Australia's 2026 Federal Budget has delivered the most significant tax reform for property investors in more than 25 years, reshaping the rules...

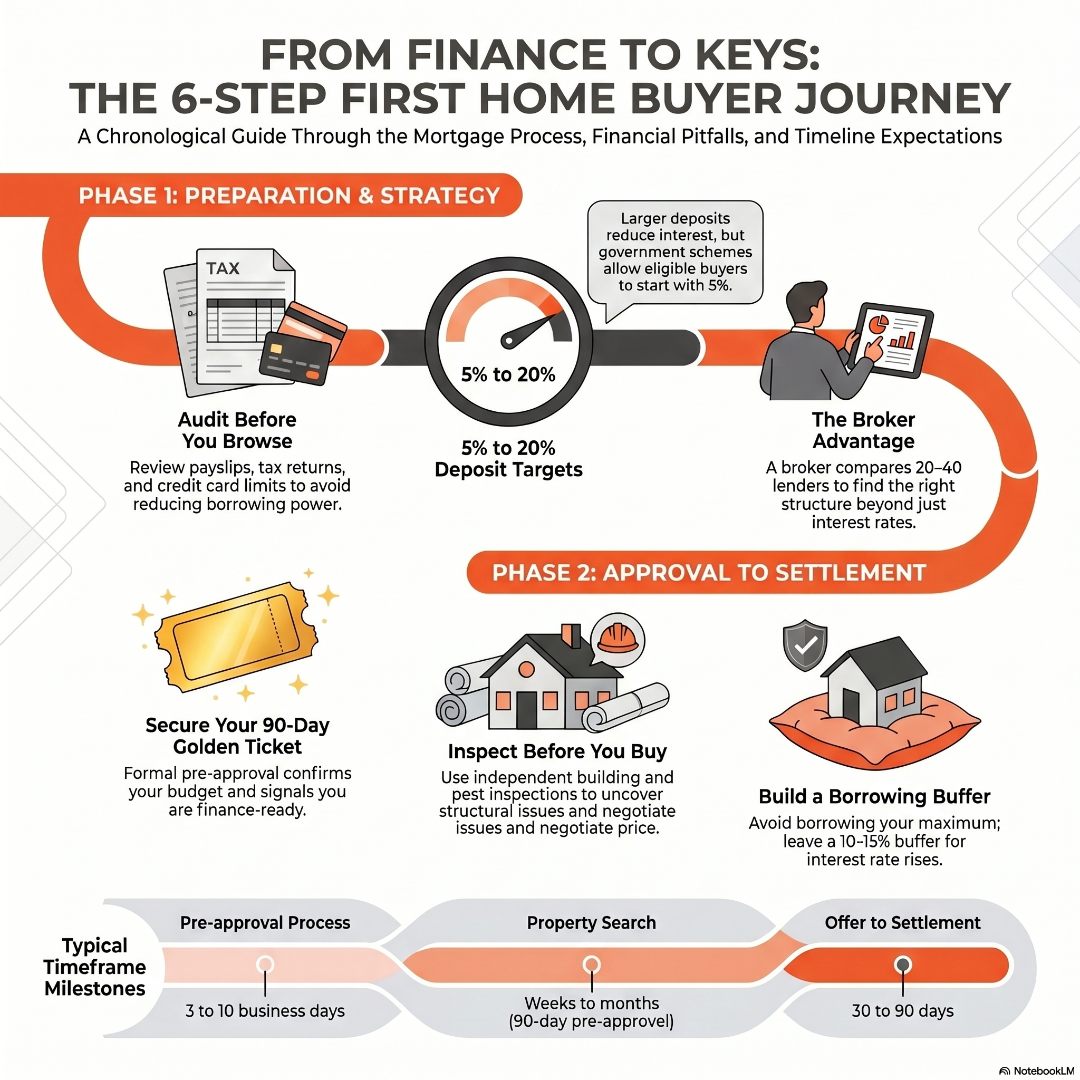

The first time home buyer mortgage process follows six clear steps: sort your finances, save a deposit, speak to a mortgage broker, secure pre-approval, find and make an offer on a property, then move through to full approval and settlement. Understanding each step in the right order makes the difference between a smooth journey and a costly false start. The biggest trap is borrowing to your absolute limit without stress-testing what happens if rates rise or income dips – getting that right is where a good broker earns their keep.

Most first home buyers open a property app before they open a bank statement. That is understandable – scrolling dream homes is far more enjoyable than facing a credit card balance. But starting the mortgage process the right way means beginning with a brutally honest financial audit.

Pull together your recent payslips and tax returns. Check your credit report – you are entitled to a free one through the major credit agencies. List every debt: personal loans, car finance, credit card limits (not just balances), and HECS/HELP repayments. Even an unused $10,000 credit card limit can reduce your borrowing power by $40,000 to $50,000, because lenders assess the limit as if you could draw it all down tomorrow.

This step is not about punishing yourself. It is about building a realistic picture of what you can actually afford – not just what a calculator spits out when you plug in a salary and a dream price. The more clearly you see your starting position, the more confidently you can plan what comes next.

The deposit question stops more first home buyers in their tracks than almost anything else. Most lenders want to see between 5 and 20 percent. The bigger your deposit, the better your loan terms, the less interest you pay over the life of the loan, and the less likely you are to need Lenders Mortgage Insurance (LMI) – an additional cost that protects the lender, not you, and can run to tens of thousands of dollars.

This is a question I wrestled with personally. When I bought my first property, I only had a 5% deposit saved. Twenty percent felt like a moving target – every year I got closer, the market moved further away. So I made a deliberate decision: I paid the Lenders Mortgage Insurance premium, accepted it as the price of entry, and got in. At the time, that LMI cost felt like a sting. Looking back, it was one of the smartest financial calls I made. Waiting another five or six years to avoid it would have meant paying significantly more for the same property – and I had crunched those numbers for a Money Magazine column, so this was not a gut feeling. It was arithmetic. When I later refinanced, I was even able to claim the LMI as a borrowing cost, which softened the blow further. Every situation is different, and I am not suggesting a 5% deposit is always the right move. But the cost of waiting is rarely zero. If you are sitting on 8% or 10% and wondering whether to push on or hold back, that is a conversation worth having with a broker who can actually model both paths for your specific numbers – not just point you at a generic calculator.

The government’s First Home Guarantee scheme allows eligible buyers to purchase with as little as a 5 percent deposit while avoiding LMI entirely – a potential saving of $15,000 to $25,000. Eligibility is capped by income and property price thresholds, and places are limited each financial year. Understanding how these schemes interact with your deposit strategy is exactly the kind of conversation a good broker will walk you through.

Whatever your target deposit, be realistic about the timeline. Trying to save 20 percent in an expensive market while also paying rent is genuinely hard. A broker can help you model different scenarios – buying sooner with 5 percent versus waiting two more years to hit 20 percent – so you make a decision based on numbers, not assumptions.

For a detailed look at what the full costs of buying actually add up to, our guide on 7 common mistakes first home buyers make in Australia covers hidden costs, stamp duty, and conveyancing fees in plain language.

Going directly to your existing bank is the financial equivalent of buying the first car on the lot without asking what else is available. This is the step most first home buyers either skip or leave too late.

A mortgage broker works across a panel of lenders – typically 20 to 40 different banks and non-bank lenders. They assess your full financial profile, run scenarios around rate changes, and match your situation to the lender most likely to approve you on the best available terms. You are not just looking for the lowest rate. You are looking for the right loan structure, the right features (offset accounts, redraw, repayment flexibility), and a lender whose credit policy suits your exact circumstances.

This matters enormously if you are self-employed, if your income includes overtime or commission, or if you have a complicated debt profile. Different lenders treat these situations very differently.

A good broker sits down with you and builds a picture of what you can genuinely carry, not just what the banks will technically allow. That conversation – the one between approved and comfortable – is where real clarity is found.

For a full breakdown of why a broker versus going direct to a bank matters, our mortgage broker vs bank guide explains the difference in detail.

Once your broker has assessed your position and selected the most suitable lender, the next step is formal pre-approval. This confirms a lender is prepared to lend you up to a specified amount, subject to finding a suitable property.

Pre-approval typically lasts 90 days. It tells sellers and agents you are a serious, finance-ready buyer – and in a competitive market, that matters.

A few things worth knowing about the mortgage pre-approval process:

With pre-approval in hand, you can search with confidence. Research recent comparable sales, not just asking prices. Attend the property at different times of day. Get an independent building and pest inspection – never skip this step. A $500 inspection that uncovers a $20,000 structural issue pays for itself many times over, and any issues found can be used to negotiate on price.

When your offer is accepted, notify your broker immediately so they can progress to full loan approval. The lender will conduct their own valuation. If that valuation comes in below your purchase price, it can affect how much they will lend.

Once the lender completes their full assessment – property valuation, final serviceability check, document verification – they issue formal loan approval. Settlement is the day ownership officially transfers. Your conveyancer or solicitor coordinates with the lender and the vendor’s legal representatives to ensure all funds and documents are exchanged correctly.

Before settlement arrives, make sure you have:

The trap that derails even well-prepared first home buyers is borrowing to the absolute maximum the lender will approve.

Consider Daniel, a 31-year-old teacher earning $90,000 a year. His bank approves him for $560,000. The repayments on that loan at 6.2 percent would consume close to 40 percent of his take-home pay – before rates move, before a car needs replacing, before he and his partner plan a family.

The better question is not “what will the bank lend me?” but “what can I confidently carry for 30 years while life happens around me?” Building in a buffer of 10 to 15 percent below your maximum approval is not being timid. It is being strategic.

| Stage | Typical Timeframe |

| Financial audit and deposit saving | Ongoing – weeks to months |

| First broker meeting and assessment | 1 to 2 weeks |

| Pre-approval | 3 to 10 business days |

| Property search | Weeks to months (pre-approval lasts 90 days) |

| Offer accepted to formal approval | 5 to 15 business days |

| Settlement | 30 to 90 days after contract exchange |

Every situation is different. If your documents are organised and your finances are clean, the process from broker meeting to pre-approval can move quickly. The longer stretches happen in the property search phase, which is entirely outside the lender’s control.

The first time home buyer mortgage process is not as complicated as it feels from the outside. It has a clear sequence: audit your finances, save your deposit, engage a broker, secure pre-approval, find the right property, and move through to settlement. The key is doing it in that order – finance first, property second.

The difference between a smooth outcome and a stressful one usually comes down to preparation, the right advice early, and the discipline to borrow what you can comfortably carry rather than what a lender will technically approve.

Before you book a broker meeting, get a head start with the tools inside the Investors Choice Mortgages Hub. You will find mortgage calculators, a borrowing capacity tool, and a Mortgage Stress Test that shows you exactly what your repayments look like at different interest rates – in ten minutes, with no obligation. When you are ready to take the next step, the team at Investors Choice Mortgages is here to walk you through every stage from start to settlement – not just with a loan, but with a strategy. Book a call with us today.

How does the first time home buyer mortgage process work in Australia?

The first time home buyer mortgage process in Australia involves six key steps: auditing your finances, saving your deposit, speaking to a mortgage broker, securing pre-approval, finding a property and making an offer, and progressing through to full approval and settlement. Finance preparation should always come before property searching. A mortgage broker is the most efficient way to navigate lender requirements and find the right loan structure for your situation.

How much deposit do I need as a first home buyer in Australia?

Most lenders require between 5 and 20 percent of the property’s purchase price as a deposit. With a 5 percent deposit, you will generally need to pay Lenders Mortgage Insurance unless you qualify for the government’s First Home Guarantee scheme, which allows eligible buyers to purchase with 5 percent down while avoiding LMI. The larger your deposit, the better your loan terms and the lower your total interest cost over the life of the loan.

How long does the first time home buyer mortgage process take?

From your first broker meeting to pre-approval typically takes one to three weeks, assuming your documents are in order. Once pre-approval is in place, the property search phase can take weeks to months. After an offer is accepted, formal approval usually follows within five to fifteen business days, and settlement is typically 30 to 90 days after contracts are exchanged. The total timeline varies depending on individual circumstances and how quickly you find the right property.

What happens if my mortgage application is denied as a first home buyer?

A declined application is not the end of the road, but it needs to be handled carefully. Common reasons include insufficient income, a high debt-to-income ratio, credit history issues, or a property the lender considers unsuitable. If your application is declined, avoid immediately applying elsewhere – multiple credit inquiries in quick succession can worsen your credit score. A mortgage broker can review the reason for the decline, advise on what needs to change, and identify alternative lenders whose credit policies are better suited to your situation.

Australia's 2026 Federal Budget has delivered the most significant tax reform for property investors in more than 25 years, reshaping the rules...

Regional property markets are outperforming capital cities across Australia right now, with dwelling values rising 3.3% over the three months to...