How to Reduce Your Monthly Mortgage Payments

There is no single magic switch, but there are several proven levers you can pull to reduce your monthly mortgage payments - and the right one...

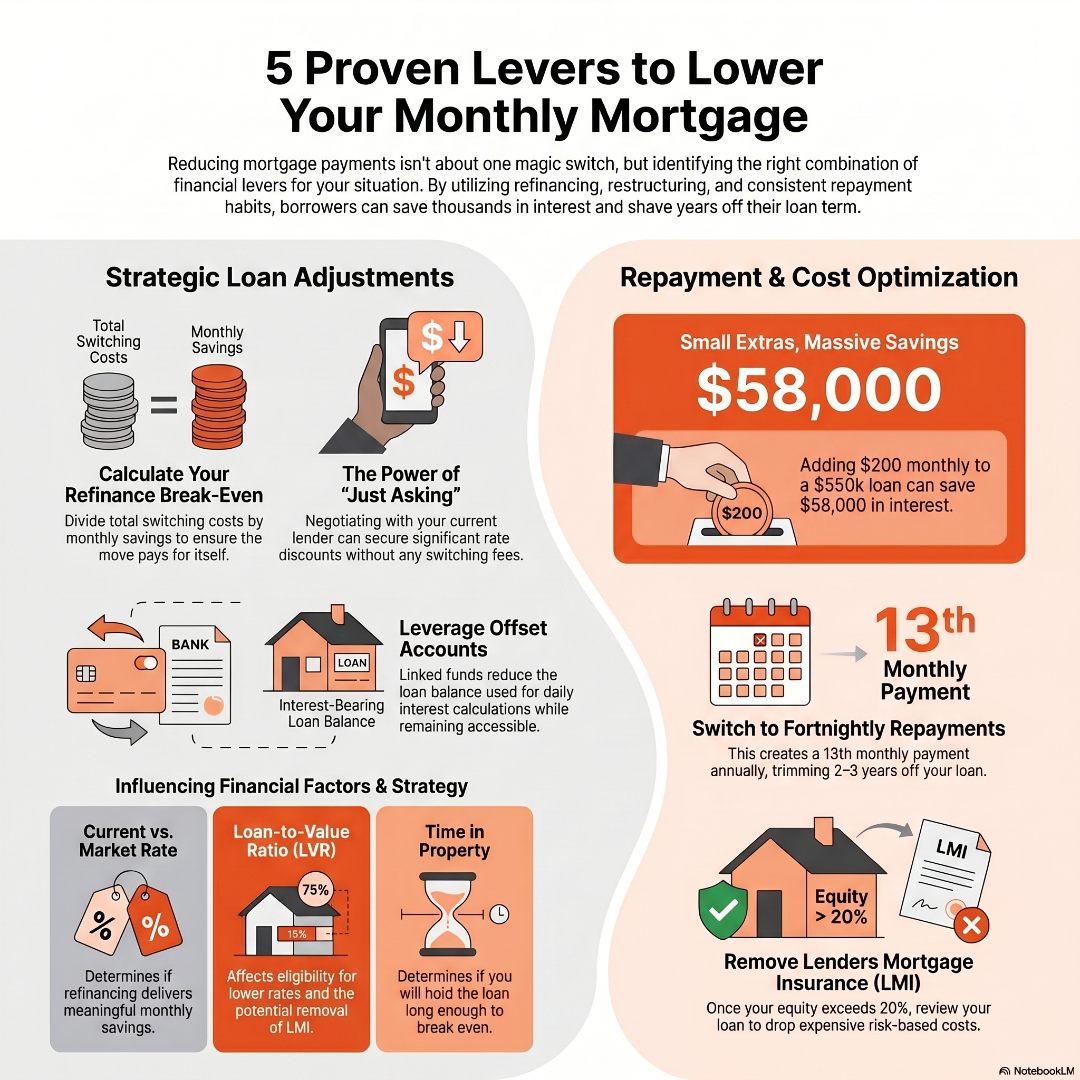

There is no single magic switch, but there are several proven levers you can pull to reduce your monthly mortgage payments – and the right one depends entirely on where you sit with your loan right now. For most Australian homeowners, the biggest wins come from refinancing to a lower rate, restructuring the loan to use an offset account more effectively, making small but consistent overpayments, or cutting extras like lenders mortgage insurance that may no longer apply to your situation. The best result, though, almost always comes from running your actual numbers rather than relying on generic advice – because what saves one borrower $300 a month might cost another one dearly.

Mark and Lisa bought their home four years ago on a rate that felt competitive at the time. They watched rates move, received letters from their bank, and kept telling themselves they would “look into it.” They never did. By the time they finally sat down with a broker, they discovered they were paying 0.8% more than they needed to on a $620,000 loan. That gap was costing them roughly $340 extra every single month – more than $4,000 a year.

This story is not unusual. A significant number of Australian homeowners are sitting on loans that no longer serve them, either because rates have shifted, their financial position has improved, or their loan structure was never quite right to begin with.

The good news is that there are multiple strategies available right now. Some require a formal loan change. Others are adjustments you can make today. Knowing which lever to pull – and in what order – is where the real savings happen.

Refinancing is the most talked-about way to lower your mortgage payment, and for good reason. Even a half a percentage point reduction on a $500,000 loan over a 25-year term can translate to roughly $150 in monthly savings. Over five years, that is $9,000 back in your pocket.

But refinancing is not free. You need to factor in:

The key calculation is your break-even point: divide your total switching costs by your monthly saving. If you are spending $1,800 to switch and saving $180 a month, you break even in 10 months. After that, every month is pure saving. If that number is less than the time you plan to stay in the property, refinancing makes sense.

You can dig deeper into the full fee breakdown in our detailed guide on how much it costs to refinance in Australia.

One critical warning: do not chase a headline rate without reading the total cost of the loan. Some low-rate products carry ongoing fees or restrictive features that quietly erode your savings over time.

Before you commit to refinancing with a new lender, it is worth reviewing the structure of your current loan. Often, the biggest gains are hiding in plain sight.

Fixed vs variable: If you are on a variable rate that has not been reviewed recently, your lender may offer you a rate reduction just to retain your business. It costs nothing to ask.

I always tell this story because it still makes me laugh – and cringe – a little. A few years ago, I sat down to look at my own lending situation and realised I had not reviewed my rates in ages. I was like the plumber with the leaking tap at home: I spend my days fixing other people’s finances and had completely ignored my own. So I picked up the phone, called my bank, mentioned a couple of comparable rates from other lenders, and just asked. That one conversation dropped my interest rate by 1.9%. I did not switch lenders. I did not pay a single fee. I just asked. The experience stuck with me because it was such a blunt reminder that lenders are not going to call you to volunteer a discount – they are quietly hoping you do not notice. Over the years, I have sat with four families and walked them through the same process of calling their existing lender, armed with the right information and a clear comparison. The combined result across those four families? Over $155,000 saved over ten years – money that stayed in their pockets, not the bank’s. The rate you are paying right now is almost certainly not the best rate your lender is willing to give you. The only question is whether you are going to ask.

If you are on a fixed rate that is ending soon, timing your review carefully can help you avoid rolling over onto a much higher standard variable rate.

Offset accounts: An offset account linked to your home loan reduces the loan balance on which your interest is calculated – every single day. If you have $40,000 sitting in a savings account earning 4.5% taxable interest, but your mortgage rate is 6.2%, you are financially better off keeping those funds in a 100% offset account instead. The interest saving is effectively tax-free, and your money stays completely accessible.

For a step-by-step look at how to maximise offset accounts, read our full guide on using offset accounts to save thousands on your mortgage.

Redraw facilities: Similar to offset accounts, a redraw facility lets you make extra repayments and pull them back if needed. It is slightly less flexible than an offset account but still reduces your daily interest calculation.

Refinancing gets all the headlines. Offset accounts sound impressive at a dinner party. But one of the most effective – and underrated – ways to reduce your total monthly interest burden is simply paying a little bit more than the minimum, consistently.

Consider this: on a $550,000 mortgage at 6%, adding just $200 extra per month reduces your loan term by roughly four years and saves you approximately $58,000 in interest. Your monthly minimum does not drop immediately, but you are dramatically reducing the principal, which means each repayment covers more principal and less interest as time goes on.

Even switching from monthly to fortnightly repayments has a meaningful effect. Because there are 26 fortnights in a year but only 12 months, you effectively make 13 monthly repayments instead of 12 – without it feeling like extra effort. For most borrowers, this simple change trims two to three years off a standard 30-year loan.

These tactics are covered in depth in our practical piece on how to shave years off your mortgage.

When you bought your property with less than a 20% deposit, you likely paid Lenders Mortgage Insurance (LMI). As your property value rises and your loan balance falls, your loan-to-value ratio (LVR) improves. If your LVR has now dropped below 80%, LMI is no longer a factor on a new loan – but you may still be sitting on a rate or product structured around that original high-LVR risk profile. This is an excellent conversation to have with a mortgage broker: has your property appreciated enough to justify a refinance that removes this cost layer entirely?

One lever many homeowners overlook is consolidating higher-interest personal debt – such as car loans, credit cards, or personal loans – into their home loan at a lower interest rate. Rolling a $15,000 car loan at 11% into your mortgage at 6% reduces the monthly interest burden on that debt immediately.

The risk, however, is real. When you consolidate shorter-term debt into a 25 or 30-year mortgage, you may pay far more in total interest over time, even at the lower rate. The right approach is to maintain a disciplined extra repayment strategy to pay down the consolidated amount quickly – not treat it as a reason to relax your repayments.

There is no universal answer. The best strategy depends on variables only you can quantify:

| Factor | What It Influences |

| Current interest rate vs market rate | Whether refinancing delivers meaningful savings |

| Loan-to-value ratio | Eligibility for better rates and LMI removal |

| Cash surplus available | Whether an offset account or extra repayments fit better |

| Other debts | Whether consolidation creates net cash flow relief |

| How long you plan to stay | Whether refinancing costs are worth the break-even period |

| Income stability | Whether fixing part of your rate provides peace of mind |

A good mortgage broker does not just compare rates. They pull together your full financial picture, run scenarios using your real numbers, and show you what actually moves the needle for your specific situation – not a generic case study.

Reducing your monthly mortgage payments is not about finding one dramatic solution. It is about identifying the combination of levers that works for your income, your goals, your loan structure, and your timeline. Refinancing might be the headline move, but offset accounts, extra repayments, loan restructuring, and smart debt management each have a role to play – sometimes together.

If you are ready to stop guessing and start knowing your numbers, head to the ICM Hub – your go-to resource for tools like the Mortgage Stress Test, Fix or Float Assessor, and personalised calculators that help you map your next move with confidence. The resources are there to give you a genuine advantage on your property journey.

How can I lower my mortgage payment without refinancing?

There are several options that do not require a formal loan change. You can link an offset account to your existing loan to reduce daily interest calculations, switch to fortnightly repayments to make an extra month’s worth of payments each year, or ask your lender if they can match a competitor’s rate to retain your business. If your loan-to-value ratio has improved since you first borrowed, you may also qualify for a lower rate tier within your existing lender’s product range.

Is it worth refinancing to reduce monthly mortgage payments?

It depends on your break-even point. Calculate all the switching costs – application fees, discharge fees, valuation, and government charges – then divide by the monthly saving your new rate delivers. If you break even within 12 to 18 months and plan to hold the loan longer than that, refinancing is very likely worth it. If you have a fixed-rate loan, check whether break fees apply before making any moves.

How much does it cost to refinance a mortgage in Australia?

For most Australians, refinancing costs between $500 and $2,000 when you account for application, valuation, settlement, discharge, and government fees. If your loan-to-value ratio exceeds 80%, you may also face Lenders Mortgage Insurance again, which can add significantly to the cost. Always get a full itemised quote from your new lender before committing. Our full breakdown is available at how much it costs to refinance in Australia.

Can making extra mortgage repayments really make a big difference?

Absolutely. On a $500,000 loan at 6%, adding just $200 extra per month can reduce your loan term by around four years and save tens of thousands in interest. Even rounding up your regular repayment to the nearest hundred dollars creates a meaningful compounding effect over time. The key is consistency rather than the size of the individual payment.

There is no single magic switch, but there are several proven levers you can pull to reduce your monthly mortgage payments - and the right one...

The first time home buyer mortgage process follows six clear steps: sort your finances, save a deposit, speak to a mortgage broker, secure...