What Do the 2026 Budget Tax Changes Mean for Your Property Investment Strategy in Australia?

Australia's 2026 Federal Budget has delivered the most significant tax reform for property investors in more than 25 years, reshaping the rules...

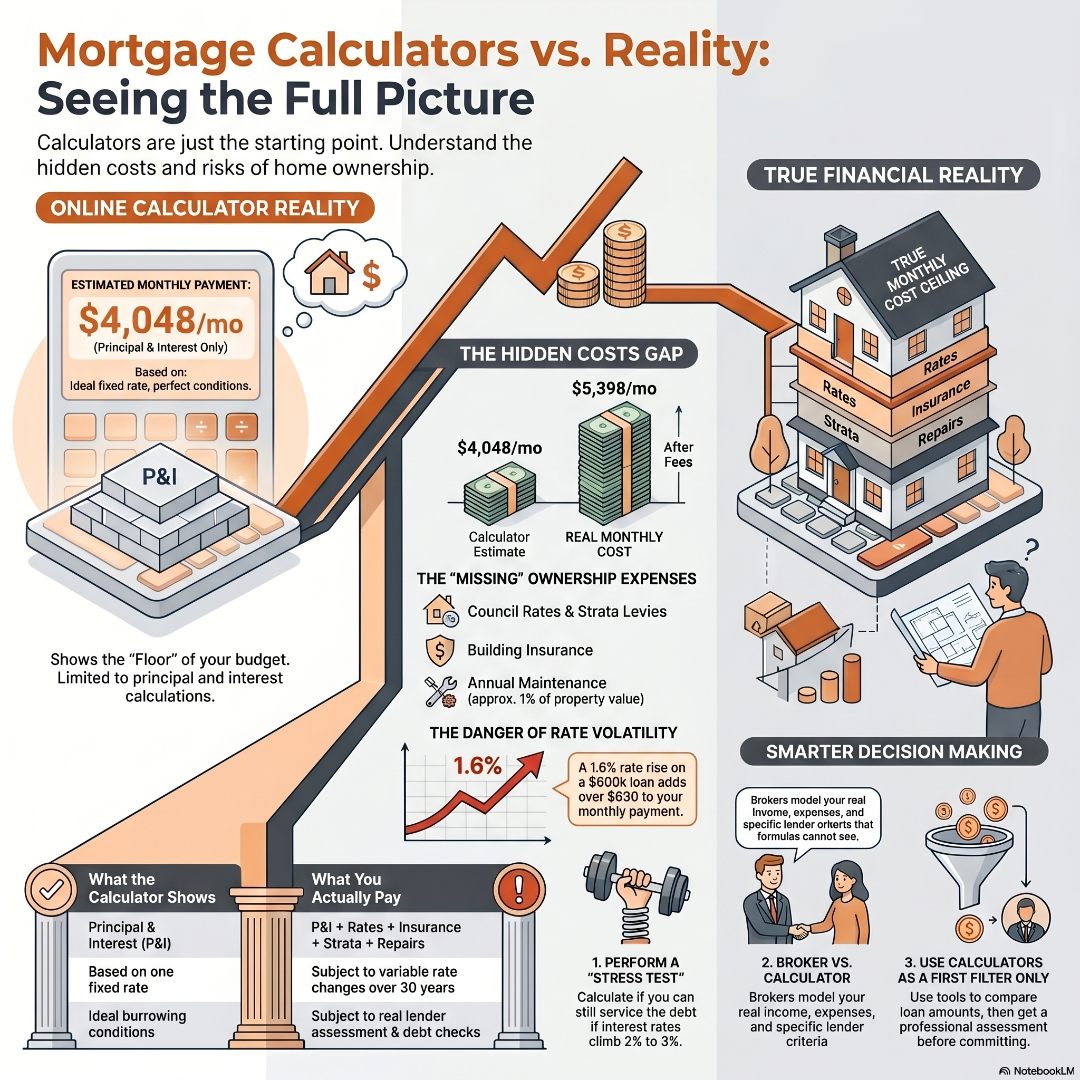

Most Australians start their property journey on an online mortgage calculator. The maths it returns is genuinely correct for what it calculates – but what it calculates is far less than the full picture. A mortgage repayment calculator accurately works out your principal and interest repayments based on a fixed loan amount, interest rate, and loan term. However, it leaves out ongoing costs like council rates, strata fees, insurance, and maintenance, and it assumes your rate never changes – meaning the figure on screen can significantly understate what you will actually pay each month. Understanding where the calculator ends and reality begins is one of the most important steps you can take before committing to a property.

At its core, a mortgage repayment calculator is straightforward. You enter three inputs: the loan amount, the interest rate, and the loan term in years. The tool then applies a standard amortisation formula to divide the total debt into equal periodic repayments – usually monthly or fortnightly – spread across your chosen term.

That formula accounts for the way interest accrues on a reducing balance. In the early years, a larger share of each repayment goes toward interest. Over time, as the principal shrinks, more of each payment chips away at the actual debt. This is called amortisation, and it is the same mathematical process every lender uses.

For example, if you enter a $600,000 loan at 6.25% over 30 years, the calculator will return a monthly repayment of around $3,694. That figure is correct based on those inputs. The maths does not lie.

So why do so many borrowers end up confused – or worse, financially stretched – after settlement?

Here is where the gap between a screen result and real life opens up. Most standard online calculators make several assumptions that do not hold in the real world.

They assume a fixed interest rate for the entire loan term. In practice, Australian home loans are almost always variable, or fixed for a short period before reverting to a variable rate. If you locked in at 5.9% and rates move to 7.5%, your actual repayment on that $600,000 loan rises from roughly $3,565 to around $4,196 per month – a difference of over $630 monthly. The calculator told you none of that.

They calculate the loan repayment, not your total housing cost. The loan itself is only one piece of the financial puzzle. A calculator will not factor in:

When you add these costs back in, the monthly out-of-pocket figure looks materially different from what a basic calculator shows.

They ignore your personal financial profile. Lenders do not approve loans based on the number a calculator returns. They assess your income, living expenses, existing debt commitments, credit history, and employment type. The calculator has no way of knowing any of that. It has no idea whether you have a $15,000 car loan or three children in private school.

| What the Calculator Shows | What You Actually Pay |

| Principal and interest repayment | P&I + council rates + insurance + maintenance + strata (if applicable) |

| Based on a fixed rate you input | Subject to rate changes over the life of the loan |

| Assumes ideal borrowing conditions | Subject to lender assessment criteria |

| No account for other debts | All liabilities assessed by banks |

It helps to think of your mortgage repayment as the floor, not the ceiling, of your monthly housing cost.

Take a first-home buyer purchasing a $750,000 apartment in Brisbane with a 10% deposit. They borrow $675,000 at 6.0% over 30 years. The calculator returns a monthly repayment of approximately $4,048. That number is accurate for the principal and interest component of the loan.

But add $4,500 per year in strata levies, $2,000 in council rates, $2,200 in building insurance, and a conservative $7,500 in maintenance – and their actual annual cost is closer to $64,776, or $5,398 per month. That is $1,350 per month more than the calculator suggested.

For a buyer budgeting tightly, that gap can be the difference between a manageable loan and genuine mortgage stress. This is precisely why understanding what the calculator does and does not include matters so much – especially for first-home buyers who may already be stretching their deposit.

You can explore how your borrowing capacity is shaped by income and existing commitments in our guide to strategies to improve your borrowing capacity for property investment.

Of all the limitations a mortgage repayment calculator has, the assumption of a permanent fixed rate is arguably the most dangerous for Australian borrowers.

This is not a theoretical risk. I know what rate shock looks like up close, and it is something I have carried with me for my entire career. My father lost everything – every dollar he had saved – after investing with a company called Estate Mortgage. It collapsed in the late 1980s when interest rates soared to levels that would be unthinkable to most borrowers today. He had no buffer, no stress test, and no one in his corner who had asked him the hard question: what happens if rates go up by 3%, 4%, or 5%? The answer, for him, was ruin. He never financially recovered, and I believe that loss contributed to his death. It is a heavy thing to carry, but it is also the reason I have spent over two decades making sure that my clients – and anyone I can reach – never walk into a loan without understanding what they are actually signing up for.

Australia has seen multiple rapid rate cycles over the past decade. Borrowers who fixed their thinking around a 2% or 3% rate environment in 2021 found themselves servicing loans at 6% and above by 2023. A calculator run at the original rate would have wildly understated what they were actually paying.

This is why stress testing – running your repayments at rates 2% to 3% higher than your current rate – is not optional. It is essential. The question you need to answer is not “can I afford this loan at today’s rate?” but “can I still service this debt if rates climb to 8% or 9%?”

Understanding how the Reserve Bank of Australia’s decisions flow through to variable mortgage rates is also part of this picture. Our article on how the RBA impacts variable mortgage rates breaks this down clearly.

If you want to know what a rate rise would mean specifically for your repayments, the ICM Hub includes a Mortgage Stress Test tool that lets you model exactly that – free for all users.

A mortgage calculator is genuinely useful as a first filter. If you are browsing properties and want a rough sense of whether a $500,000 loan or an $800,000 loan sits within your ballpark budget, a calculator is the right tool for that job.

Where it falls short is at the decision-making stage. Once you are seriously considering a property, the calculator’s limitations become risks. You need to know how much a bank will actually lend you – which depends on your income, existing debts, and living expenses. You need to know what the true monthly cost of ownership looks like, not just the loan repayment. And you need to understand what happens to your cashflow if rates move.

Our article on what happens if interest rates rise on your investment loan walks through exactly those scenarios, including the buffers lenders apply when assessing your application.

The most important next step for any buyer is to stress-test their mortgage position before they make an offer – not after.

A mortgage broker does what no calculator can: they model your situation using your real numbers and the actual lending criteria applied by banks.

They will factor in your income type (PAYG, self-employed, or contractor), your existing debt, your living expenses, your deposit size, and the specific property you are buying. They will run multiple lender scenarios to find the most suitable structure. And critically, they will show you what your repayments look like not just today, but if rates move by 1%, 2%, or 3%.

Think of the calculator as a starting point – the tool you use to get oriented. A broker conversation is where you get the real number: the one that accounts for your life, not just a formula.

A mortgage repayment calculator is accurate for what it does – and limited in ways that matter enormously. It correctly calculates your principal and interest based on the rate you enter. What it cannot tell you is how much you will actually pay each month once you factor in insurance, rates, strata, maintenance, and the very real possibility that rates will not stay where they are today.

Use the calculator to get oriented. Then get a proper assessment before you commit. The difference between the two is not just a number on a screen – it is the difference between a comfortable loan and one that stretches you thin when life gets unpredictable.

Ready to go beyond the calculator? Head to the Investors Choice Mortgages Hub to access tools including the Mortgage Stress Test, Fix or Float Assessor, and expert resources designed to give you a genuine picture of what you can afford – free for every user.

Are mortgage calculators accurate for Australian home loans?

Mortgage calculators are mathematically accurate for the principal and interest figures they return. However, they leave out significant ownership costs including council rates, building insurance, strata levies, and maintenance. They also assume a fixed interest rate, which rarely reflects how Australian variable home loans perform over time. Always treat the calculator result as a starting point, not a final budget.

Why is my actual mortgage payment higher than the calculator estimate?

The most common reasons are rate changes since you first modelled the loan, and ownership costs the calculator does not include – such as insurance, council rates, strata fees, and repairs. Some buyers are also surprised when lender fees or mortgage insurance are not factored into the figure they modelled online.

Does a mortgage repayment calculator include taxes, strata, and insurance?

Standard mortgage calculators in Australia do not include council rates, strata levies, home insurance, or maintenance costs. They show you the loan repayment only. Some more advanced tools allow you to add these manually, but most basic calculators you find online do not prompt you to do this.

How do I calculate how much I can actually afford to borrow, and what is mortgage stress testing?

True borrowing capacity is determined by your gross income, existing financial commitments, living expenses, deposit size, and the serviceability requirements set by individual lenders. An online calculator cannot assess these variables. Stress testing takes this a step further – it means calculating whether you could still service your loan if interest rates rose by 2% to 3% above your current rate. Australian lenders are required to apply a serviceability buffer of typically 3% above the loan rate when assessing applications. Running your own stress test before you apply helps you understand your true financial comfort zone. Speaking with a mortgage broker is the most reliable way to get an accurate borrowing figure based on your specific situation.

Australia's 2026 Federal Budget has delivered the most significant tax reform for property investors in more than 25 years, reshaping the rules...

Regional property markets are outperforming capital cities across Australia right now, with dwelling values rising 3.3% over the three months to...