What Do the 2026 Budget Tax Changes Mean for Your Property Investment Strategy in Australia?

Australia's 2026 Federal Budget has delivered the most significant tax reform for property investors in more than 25 years, reshaping the rules...

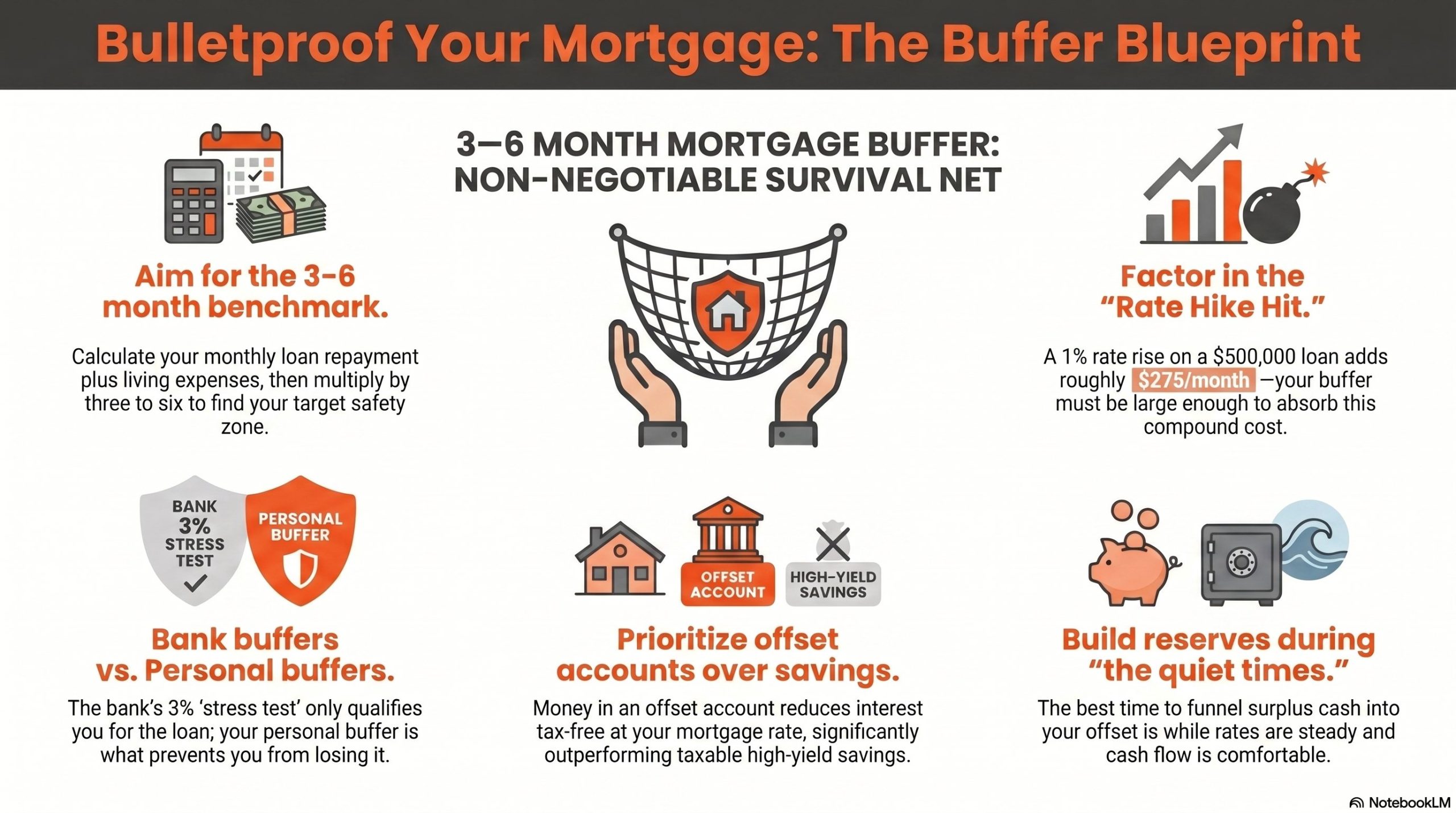

Most Australian homeowners and property investors know they should have a buffer. But knowing you need one and understanding exactly how much – and where to keep it – are two very different things. A mortgage savings buffer of three to six months of loan repayments plus living expenses is the benchmark most financial professionals recommend, though the right amount depends heavily on your income stability, loan size, and risk exposure. Rates can rise faster than most people expect, and the cost of being underprepared is not just financial – it is the stress, the panic, and the poor decisions that follow.

When a lender assesses your home loan application, they are required under APRA guidelines to stress-test your ability to repay at a rate approximately 3% above the product rate at the time of application. If you borrow at 6%, the bank has already checked whether you can handle 9%. So far, so sensible.

But here is where many borrowers relax when they should not. The bank’s buffer is a serviceability test – a pass or fail calculation at the point of application. It does not account for what happens if your income drops, your tenant leaves, your roof needs replacing, or all three happen at once.

The bank’s buffer tells you whether you qualified for the loan. Your personal mortgage savings buffer is what keeps you from losing it.

Mortgage stress in Australia – typically defined as spending 30% or more of pre-tax household income on repayments – is not caused by rate rises alone. It is caused by rate rises colliding with an already stretched household budget, with no reserves left to absorb the shock.

The formula is straightforward, even if the numbers are sobering.

Step 1: Work out your monthly loan repayment. On a $500,000 loan at around 6%, your principal and interest repayment is roughly $3,000 per month.

Step 2: Add your monthly living expenses. For most households, this sits between $3,500 and $6,000 per month depending on family size.

Step 3: Multiply by three to six. Using a combined monthly figure of $6,000, a three-month buffer is $18,000 and a six-month buffer is $36,000.

Step 4: Factor in rate scenarios. A 1% rate rise on a $500,000 loan adds approximately $275 per month. Over six months, that is an additional $1,650 to absorb. A robust home loan repayment buffer has already accounted for this.

For investors with multiple properties, this calculation runs on every loan.

| Scenario | Loan Amount | Rate Rise | Extra Monthly Cost | 6-Month Buffer Needed |

| Owner-occupier | $500,000 | +1% | +$275/mth | ~$36,000 total |

| Investor (2 loans) | $1,000,000 | +1% | +$833/mth | ~$60,000+ total |

| Investor (3 loans) | $1,500,000 | +1% | +$1,250/mth | ~$85,000+ total |

Understanding the real dollar cost of a rate rise removes the fear and replaces it with a plan.

On a variable rate loan of $500,000:

These figures look manageable in isolation – but they compound. If rates moved from 6% to 8% over 18 months, that $500,000 loan now costs $556 more per month than it did at the start. Annualised, that is an additional $6,672 per year coming out of your pocket.

The key lesson from recent rate cycles is clear: rates will rise again at some stage. You need to have that buffer in place before they do, not after.

For a deeper look at how rate movements flow through to your repayments, see our article on how the RBA impacts variable mortgage rates.

This is one of the most important – and most underappreciated – decisions a mortgage holder can make.

A savings account earns interest, typically around 4% to 5% for high-yield accounts. But that interest is taxable income. On a 37% marginal tax rate, a 5% gross return becomes roughly 3.15% after tax.

Now compare that to a 100% offset account. Every dollar parked in your offset directly reduces the balance on which your mortgage interest is calculated. If your loan rate is 6%, your offset effectively earns you 6% – tax-free – because you are reducing interest rather than earning income.

For someone with a $500,000 mortgage holding $30,000 in their offset account, the annual interest saving is approximately $1,800 – compared to around $945 net in a savings account at 5%. The offset wins by a significant margin.

A buffer held in your offset account also quietly chips away at your principal balance, shortening your loan term in the background. You get both the safety net and the debt reduction.

For a full breakdown of this strategy, read our guide on how to use offset accounts to save thousands on your mortgage.

If you hold investment properties, the risk profile is fundamentally different to someone with a single owner-occupied mortgage.

Rental income is not guaranteed. A tenant can vacate. A property can sit vacant for four to twelve weeks during a re-let. A major repair can land a $5,000 to $15,000 bill at any time. And rising rates affect every investment loan simultaneously.

An investor holding two properties with loans totalling $1 million, facing a 1% rate rise, is absorbing an additional $833 per month. If one property is simultaneously vacant, the combined cash flow hit could easily exceed $3,500 per month. Without a buffer, the only options are credit cards, selling under pressure, or missed repayments – none of which lead anywhere good.

I have seen this play out in real portfolios. I recently worked with clients who held multiple investment properties and had been sitting comfortably on fixed rates. When those rates rolled off, they were suddenly staring down $60,000 to $80,000 in additional annual interest – an increase they had not fully planned for. They were weighing up whether to restructure, sell, or simply absorb a hit that was threatening to undo years of patient portfolio building. The conversation we had was not really about interest rates. It was about options – and the painful reality that options shrink fast when the pressure is already on. We worked through the whole portfolio, looked at refinancing possibilities and renegotiation, and found a path forward. But it would have been a very different conversation if a proper buffer had been in place before the fixed rates expired.

Our article on what happens if interest rates rise on your investment loans goes deeper on the specific cash flow scenarios investors need to model.

Mortgage stress does not always arrive as a crisis. It often starts quietly.

Warning signs include:

If any of these sound familiar, the issue is not a lack of income. In most cases, it is a structural problem with how the mortgage and savings are arranged. For a step-by-step self-assessment, the mortgage stress test guide on this site walks you through the process.

The most consistent advice from experienced property investors is this: build your buffer when times are good.

When rates are steady or falling, cash flow feels comfortable. That is exactly the moment to funnel surplus funds into your offset account. The discipline to build reserves during calm periods is what separates investors who hold their portfolios through rate cycles from those who are forced to sell.

If you are currently sitting at a rate that feels manageable, run the numbers at 1% and 2% above your current rate. Ask yourself honestly whether you could absorb those extra costs for 12 to 18 months without depleting your savings. If the answer is no – that is your signal.

A mortgage savings buffer is not just a nice-to-have financial concept. For Australian homeowners and investors, it is the most practical form of protection available against the inevitable ups and downs of the rate cycle.

The benchmark of three to six months of repayments plus living costs, held in a 100% offset account, is a solid starting point. Investors need more. Everyone needs to do the specific calculation for their own situation rather than relying on round-number guesses.

The time to build that buffer is before rates rise – not when the RBA announcement lands and the repayment notice arrives in your inbox.

If you are unsure where your buffer stands today, or whether your current loan structure is set up to weather the next rate cycle, the best next step is a professional mortgage review. Book a mortgage review call today and find out exactly where you stand.

How much mortgage buffer do I need if interest rates rise in Australia?

The standard recommendation is three to six months of your total monthly loan repayments plus living expenses. For a $500,000 loan with $3,000 in monthly repayments and $3,500 in living costs, that is between $19,500 and $39,000. Investors with multiple properties should calculate this across every loan and factor in vacancy and repair costs.

What happens to my repayments if interest rates go up 1% on my mortgage?

On a $500,000 variable rate home loan, a 1% rate rise adds approximately $275 per month to your repayments. On a $1 million loan across multiple investment properties, the same rise costs around $833 per month extra. Over 12 months, that is a significant cash flow impact that a well-maintained buffer can absorb without disruption.

Is an offset account better than a savings account for storing my mortgage buffer?

Yes, in most cases. An offset account effectively earns your mortgage interest rate – tax-free – by reducing the balance on which interest is calculated. A savings account earning 5% is taxed, leaving a net return of around 3.15% for someone on a 37% marginal rate. If your mortgage rate is 6%, the offset outperforms a savings account after tax by a meaningful margin, while keeping your money fully accessible.

Does the APRA 3% buffer mean I am automatically protected from rate rises?

Not entirely. The APRA 3% buffer is a serviceability test applied when your loan is assessed, confirming you can theoretically service the loan at a higher rate. It does not account for income changes, vacancy periods, major repairs, or the practical challenges of managing a stretched budget over many months. Your personal mortgage savings buffer is a separate and essential layer of protection.

Australia's 2026 Federal Budget has delivered the most significant tax reform for property investors in more than 25 years, reshaping the rules...

Regional property markets are outperforming capital cities across Australia right now, with dwelling values rising 3.3% over the three months to...