Is Investor Activity Set to Fall?

Australia's property investors are facing a double headwind in 2026 - and the latest lending data confirms the retreat has already begun....

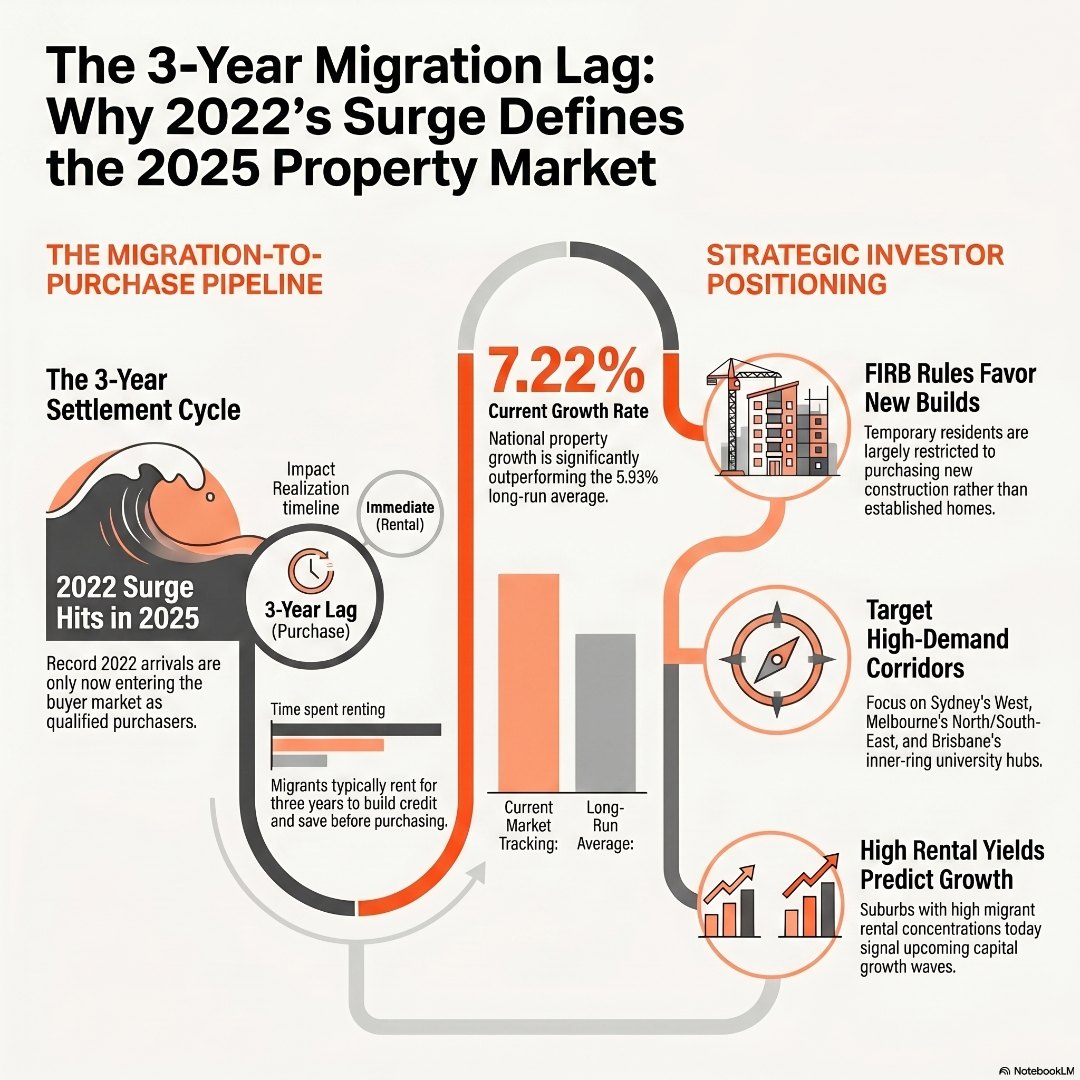

Migration drives Australian property prices, but the effect is not immediate. Research tracking over 7,200 suburbs shows a precise three-year lag between migration surges and accelerated price growth – meaning Australia’s record 2022 arrivals point squarely at 2025 and 2026 as the years deferred demand converts into purchase activity. For investors already in the market, this pipeline represents one of the most compelling forward-looking signals in years. For those still on the sidelines, the window to position ahead of this wave is narrowing fast.

Here is the thing that most property commentators miss entirely. The headlines focus on arrival numbers – record this, surge that – but they skip the critical detail of what newly arrived migrants actually do when they land. They rent.

It makes complete sense when you think about it. A family arriving from India, China, or the Philippines is navigating an entirely new country. They are finding schools, settling into jobs, building a credit history, and learning which suburbs suit their lifestyle. Buying a property in the first six months is not just unlikely – for most migrants on temporary visas, it is legally restricted.

So they rent. They save. They watch the market. They accumulate the deposit. And then, typically around three years after arriving, they make their move into ownership.

This is not speculation. Detailed modelling across more than 7,200 Australian suburbs confirms a precise three-year lag between net overseas migration surges and measurable property price acceleration. The correlation is consistent and predictable, with directional accuracy tracked back to 2003. This is not a theory. It is a pattern that has repeated itself across every major migration wave Australia has experienced.

I have seen this play out up close. Years ago, I had Andrew Mel from Yellow Brick Road on my podcast – a man whose family had arrived in Australia with essentially nothing. No credit history, no established community, no local knowledge of which suburbs were worth watching. What they did have was the drive to settle in properly, find their footing, and build step by step. Andrew reflected on that journey with a kind of quiet pride, and I remember thinking how perfectly it illustrated something I had been observing in the data for years. Migrants do not arrive with a property purchase ready to go. They arrive with ambition and very little else that a lender will accept on day one. They rent. They learn the market from the inside out. They build the financial record that eventually gets them across the line. By the time Andrew’s family was in a position to buy, they understood the market far better than most locals who had been watching it from a distance their whole lives. That is not a gap in the data – it is the pattern. And when you understand that pattern, you stop reacting to arrival numbers and start reading the clock.

Australia’s borders reopened after COVID with a rush of arrivals in 2022 that broke migration records. Net overseas migration that year was extraordinary, as students, skilled workers, and families who had been waiting out the pandemic finally arrived.

Most observers at the time were focused on the immediate rental crisis – and that was real and painful. But the more powerful downstream effect was not visible yet. That deferred ownership demand was quietly building, three years away from expressing itself in the purchase market.

Run the maths forward from 2022 and you land exactly on 2025 and 2026.

Those renters are now three years in. They have established credit histories. They have saved deposits. They have settled into communities. And they are ready to buy. The structural pipeline of new buyers created by that 2022 surge is not speculative – it is already in the system, and it is converting. National property price growth is currently tracking at 7.22% for 2026, a figure that sits meaningfully above the long-run average of 5.93%. That gap is not an accident.

Understanding what drives property prices in Australia means understanding demand. And right now, demand has a very predictable structural driver that most retail investors are not yet pricing into their decisions.

Not all migrants can purchase any property. This is an important detail that directly shapes where demand flows – and where investors should pay attention.

The Foreign Investment Review Board (FIRB) restricts most temporary residents and foreign buyers from purchasing established dwellings. Their options are primarily limited to new builds – off-the-plan apartments, new house-and-land packages, and newly constructed homes. Permanent residents and Australian citizens face no such restrictions, and many migrants make this transition to permanent residency within their first few years.

What this means practically is that new construction corridors, high-density urban precincts, and outer-ring growth areas where new supply is being delivered tend to absorb a disproportionate share of early migrant buyer demand. These are often the same suburbs generating strong rental yields in the years before purchase activity ramps up, which is why investors who bought in these areas three to five years ago have enjoyed both strong rental returns and meaningful capital growth.

For investors thinking about predicting capital growth in their target suburbs, the migration pipeline is one of the most actionable data points available. Suburbs with high migrant rental concentrations today are likely to see above-average purchase demand over the next two to three years.

There is a public conversation happening around migration and housing that generates a lot of heat but not much light. Politicians debate numbers. Commentators argue about causation. Social media conflates foreign investment with migration, and migration with affordability, in ways that obscure rather than clarify.

Here is the honest picture.

The impact of migration on house prices in Australia is real but delayed. It does not happen in year one. It builds steadily and then accelerates as the settlement-to-ownership pipeline matures. The 2022 cohort is not a single event – it is a wave, and that wave is arriving now.

At the same time, migration is not the only driver. Interest rates, housing supply, lending conditions, and employment all interact with migration demand to produce the final price outcome. Migration provides the structural demand floor. The other factors determine how high the market rises above it.

What investors need to understand is that migration-driven demand is more predictable than most other market forces. Interest rate decisions surprise markets. Employment shocks happen. But settlement patterns are consistent. People who arrived in 2022 do not suddenly decide not to buy. That demand is in the pipeline, and it will express itself.

Knowing that a wave of demand is coming is useful. Knowing where to position is more useful. Here are the key strategic considerations.

Follow the settlement corridors. New migrants tend to cluster in areas with established communities, good public transport links, and proximity to employment hubs. In Sydney, the south-west and western corridors continue to attract large migrant communities. In Melbourne, the north and south-east. In Brisbane, inner-ring suburbs with strong university and healthcare employment. In Perth, the coastal northern suburbs have seen significant growth driven partly by migration from Asia and South Africa.

Prioritise rental yield now, capital growth later. Suburbs with high migrant rental populations generate strong yields today and are likely to see purchase demand increase as that cohort moves toward ownership. A property that delivers 4.5% gross yield now while also sitting in the path of emerging ownership demand is a compelling investment proposition.

Consider new builds. Given FIRB constraints, new construction in high-migration suburbs is directly in line with that pent-up demand. New apartments near universities, transport links, and employment precincts are well positioned.

Manage your borrowing capacity strategically. Adding a property to your portfolio in 2025 means competing in a market where demand is building. Getting your structure right now – before that competition intensifies – is a genuine advantage. Understanding strategies to improve your borrowing capacity for property investment can make the difference between moving ahead of the wave or chasing it.

If you are thinking about how to build a profitable investment property portfolio in this environment, migration data gives you a layer of forward-looking confidence that most investors simply do not have access to.

The migration wave of 2022 is not history. It is present tense. The families and professionals who arrived three years ago are making purchase decisions right now. They are in the market, pre-approvals in hand, competing for properties in exactly the suburbs where settlement corridors have concentrated.

If you are an investor, this is one of the rare moments where the data gives you a structural advantage over emotional market participants. You can see the demand coming. You can position ahead of it. Or you can read the headlines in 2026 when national growth prints well above 7% and wonder why you hesitated.

The question is not whether migration will impact Australian property prices in 2025. The data makes clear that it already is. The question is whether you are positioned to benefit from it.

Ready to explore what this migration pipeline means for your specific target suburbs and your own borrowing position? Head to the Investors Choice Mortgages Hub to access suburb research tools, AI-powered property insights, and the expert guidance you need to move with confidence – not fear.

How does migration impact Australian house prices?

Migration affects Australian house prices with a consistent three-year lag. Newly arrived migrants typically rent first while they settle, build credit, and save a deposit, then enter the ownership market around three years after arrival. This creates a predictable pipeline of demand that drives price acceleration in the suburbs where migrants have concentrated.

Do migrants push up house prices in Australia?

Migrants do contribute to rising house prices, but the timing is delayed rather than immediate. The more visible short-term effect is increased rental demand and higher rents. Purchase demand builds gradually and then accelerates as the settlement-to-ownership pipeline matures, typically three years after a major migration surge.

Where are migrants most likely to buy property in Australia?

Migrant buyers tend to concentrate in areas with established communities, strong transport links, and proximity to employment and universities. Western and south-western Sydney, Melbourne’s north and south-east, inner Brisbane, and Perth’s northern coastal corridor all see high migrant purchase activity. Given FIRB restrictions, new construction precincts within these corridors attract a disproportionate share of demand.

Can temporary residents buy property in Australia in 2025?

Temporary residents can purchase property in Australia but are subject to FIRB rules. In most cases, they are restricted to purchasing new dwellings – either off-the-plan or newly constructed homes – and cannot buy established properties. Once migrants gain permanent residency or citizenship, these restrictions no longer apply. FIRB rules can change, so seeking current advice before purchasing is recommended.

All market data and research referenced in these articles is sourced from HTAG Analytics’ April 2026 research report: “A Forced Autoregressive Model of Australian Residential Property Price Dynamics: Credit, Migration, Monetary Policy, and Supply Interactions 2003–2026” by Alex Fedoseev and Dr. Matija Djolic, HTAG Analytics.

Investors Choice Mortgages acknowledges HTAG Analytics as an industry-leading source of Australian property market intelligence.

Australia's property investors are facing a double headwind in 2026 - and the latest lending data confirms the retreat has already begun....

Australia's 2026 Federal Budget has delivered the most significant tax reform for property investors in more than 25 years, reshaping the rules...