What Do the 2026 Budget Tax Changes Mean for Your Property Investment Strategy in Australia?

Australia's 2026 Federal Budget has delivered the most significant tax reform for property investors in more than 25 years, reshaping the rules...

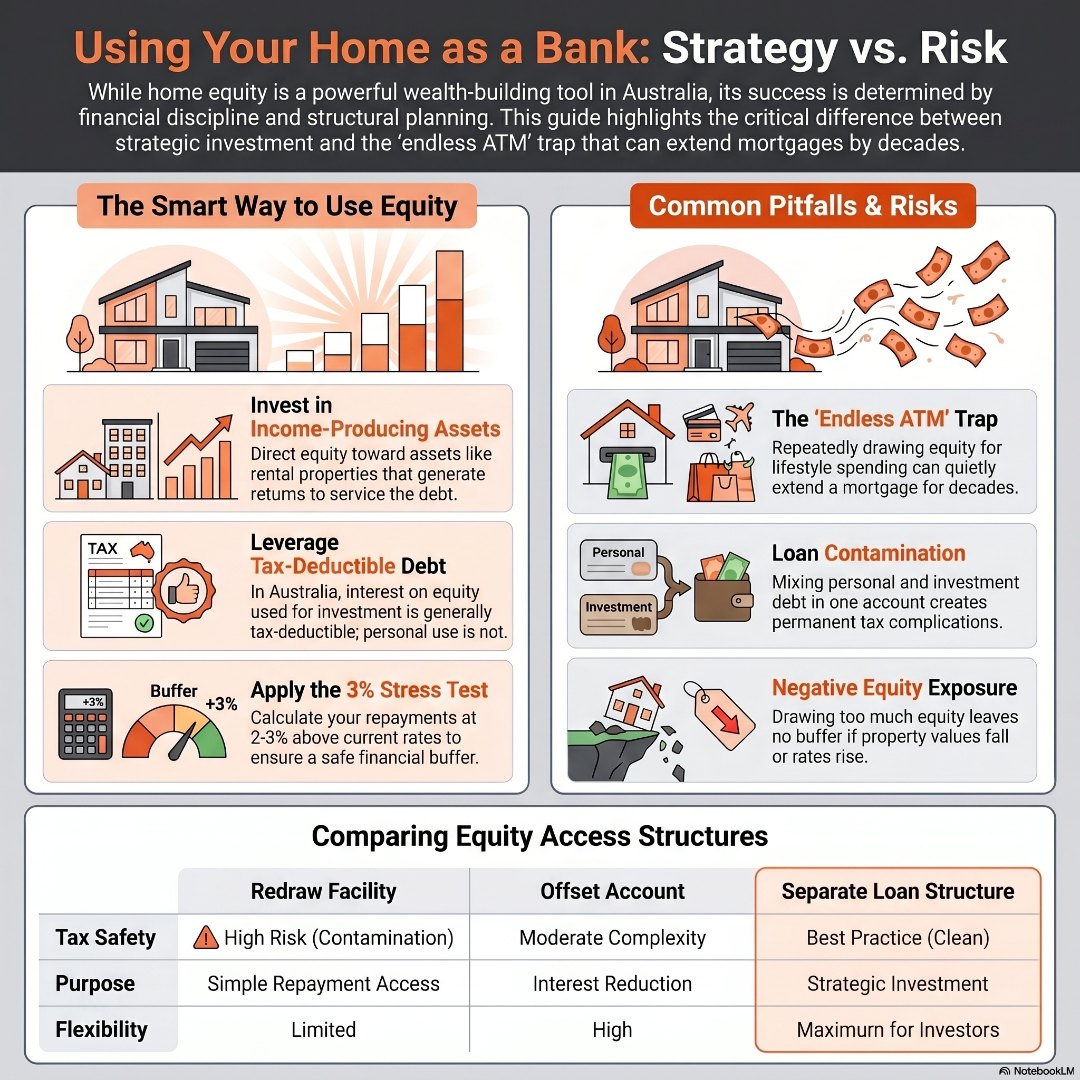

Using your home as a bank is not inherently risky – but the risks of using home equity are real, and they are almost entirely determined by how disciplined you are with the money and how clearly you have planned to repay it. Borrowing against your house value in Australia can be a powerful wealth-building strategy when the funds are directed toward income-producing investments, value-adding renovations, or purposeful financial goals. However, when equity is accessed without a clear repayment plan, used for lifestyle spending, or drawn on repeatedly without regard to rising interest rates, it can quietly extend your mortgage by decades and place your most important asset at serious risk.

It often starts with a conversation at a dinner party, a letter from a bank, or a quick look at recent suburb sale prices. Someone mentions that property values have risen considerably over the past few years and suddenly you are thinking about the equity sitting inside your walls – money built up through years of repayments and rising market values.

For many Australians in their 40s and 50s who have owned their home for a decade or more, this is not a small number. A homeowner who bought in a capital city in 2015 may now be sitting on several hundred thousand dollars of usable equity. It feels almost wasteful not to do something with it.

That feeling is not wrong. Accessing home equity strategically has been a foundational step in building property portfolios for thousands of Australian investors. The key word is strategically – because the same mechanism that can accelerate your wealth can quietly erode it if you go in without a plan.

The risks of using home equity do not live in the act of accessing it. They live in the decisions made after you do.

The most common trap: a homeowner pays down their mortgage, builds equity, and accesses some of it for a renovation, a holiday, or a car – then does it again a few years later. Each time, the mortgage resets or grows. Before long, a homeowner in their mid-50s who could have been mortgage-free is staring at 20 more years of debt with no clear path forward.

This is not a hypothetical. It is one of the most consistent patterns seen among homeowners who struggle financially in their later years. They were not irresponsible people. They simply never had a concrete repayment strategy tied to each draw.

There is a fundamental difference between borrowing against your home to purchase an investment that generates income, and borrowing to fund a depreciating expense. A car loses value the moment you drive it away. A holiday is a memory. Neither generates a return sufficient to service the additional debt you have taken on.

Equity borrowed for a well-selected investment property, on the other hand, may deliver rental income, potential capital growth, and tax deductions on the interest. When the return exceeds the cost of borrowing, the strategy makes financial sense. When it does not, you are borrowing at your home’s expense.

If your equity release is structured as a variable-rate loan – common for lines of credit in Australia – your repayments will rise when rates rise. Australians experienced exactly this between 2022 and 2024, with the RBA lifting the cash rate 13 times. Those who had stress-tested their borrowing absorbed the impact. Those who had not found themselves in genuine mortgage stress.

Understanding what happens if interest rates rise on your investment loans before you borrow is not optional – it is essential.

If you draw heavily on your equity and property values then fall, you may find yourself owing more than your property is worth. This is called negative equity. While it does not trigger automatic lender action if you are still making repayments, it eliminates your flexibility to refinance, sell, or access further credit. The lower you draw your equity buffer, the more exposed you become.

Borrowing against your house value in Australia can be a very smart move when three conditions are met.

1. The money is going toward an asset that will generate a return.

Funding the deposit on a well-researched investment property, completing a strategic renovation that adds measurable value, or starting a business with a realistic income projection. In each case, there is a clear mechanism by which the borrowed money should generate more than it costs to service. That is responsible leverage.

2. Your repayment capacity has been stress-tested.

Before drawing on equity, run your numbers at a rate at least 2 to 3 per cent higher than your current rate. If that scenario breaks your budget, you are overextending. Maintain a cash buffer of at least three to six months of total repayments across your existing mortgage and the new equity loan. You can stress-test your mortgage using ICM’s free tools to confirm your position is genuinely solid before you act.

3. Your investment and personal debt are kept in separate loan structures.

In Australia, interest on debt used for investment purposes is generally tax-deductible, while interest on personal debt is not. If you draw from a redraw facility or line of credit and mix investment spending with personal spending in the same account, you create what is known as a contaminated loan. The ATO does not allow proportional deductions on mixed-purpose debt, and it becomes a costly, complex problem to resolve. Keeping each purpose in its own account from the very beginning is the clean, compliant, and financially smarter approach.

For a full breakdown of how to structure this correctly, the guide on how to get cash from home equity walks through exactly how to calculate your usable equity, choose the right product, and protect your tax position.

This is a question many Australian homeowners ask, and the answer depends on what you intend to do with the funds.

A redraw facility allows you to access extra repayments you have made above the minimum. It is a lower-cost option, but funds drawn from a redraw facility on an owner-occupier loan may lose their tax deductibility for investment purposes – a critical point many borrowers are not told before they act.

An offset account reduces the interest you pay by holding funds against your loan balance. If you draw offset savings and use them for investment purposes, the tax treatment can become complicated.

For most investors looking to access equity strategically, a line of credit or a top-up loan in a separate investment loan structure is the cleaner, more tax-efficient approach. The right choice depends on your specific circumstances – which is exactly why a mortgage review with a specialist, rather than a bank manager, makes such a difference.

The homeowners who use equity well share a few common habits. They go in with a written plan – what the money is for, how it will generate a return, and how they will repay it. They do not draw equity to its limit. They keep a meaningful buffer and structure their loans correctly from the start, rather than trying to fix a mess after the fact.

Think of it this way: your home equity is a powerful tool. In skilled hands with a clear purpose, it builds things. Without a plan, it causes damage.

Opening opportunities with your home equity starts with understanding the full picture – before you commit.

Using your home as a bank is a legitimate and often powerful financial strategy – but the risks of using home equity are real and worth understanding clearly before you act. The danger is not in accessing equity. It is in accessing it without a plan, without stress-testing your repayments, and without structuring your loans correctly for tax purposes.

Used well, your home equity can fund the next stage of your financial life. Used carelessly, it can extend your mortgage by decades and leave you exposed when the market or interest rates move against you.

If you are thinking seriously about borrowing against your home’s value, get the numbers right first. Do not navigate home equity blind. Book a mortgage review call today and work through the strategy with an experienced, property-focused mortgage broker who can show you exactly what is possible – and exactly what to watch out for.

Is it risky to borrow against my home equity in Australia?

It depends on how you use the funds and whether you have stress-tested your repayments. Borrowing against your home to invest in income-producing assets with a clear repayment strategy is a well-established wealth-building approach in Australia. The risk rises sharply when equity is used for lifestyle spending without a plan, drawn to its limit, or structured in a way that contaminates your tax deductions. A mortgage specialist can help you assess whether the risk is appropriate for your situation.

Can I lose my house if I borrow against my home equity?

In an extreme scenario – where you can no longer service repayments and property values have fallen significantly – a lender can move to recover the debt. This is rare, but it is a real risk when homeowners extend their borrowing position beyond what they can comfortably repay and have no cash buffer. Stress-testing your repayments at higher interest rates and maintaining a buffer of at least three to six months of expenses is the most effective protection.

What are the hidden costs of refinancing to access equity in Australia?

Refinancing to release equity typically involves discharge fees from your existing lender (often $150 to $400), application fees with the new lender, property valuation costs ($200 to $600), and legal or settlement fees. If you are exiting a fixed-rate loan early, break costs can be significant and vary based on how far rates have moved. Always request a full cost breakdown before proceeding with a refinance.

Is the interest on a home equity loan tax-deductible in Australia?

Only if the funds are used for investment purposes, such as purchasing an income-producing property or shares. Interest on equity used for personal spending – including home renovations, holidays, or car purchases – is not tax-deductible. This distinction makes loan structure critical. Mixing investment and personal debt in the same account creates a contaminated loan that is difficult to separate for tax purposes. A property-focused mortgage broker can help you structure this correctly from the outset.

Australia's 2026 Federal Budget has delivered the most significant tax reform for property investors in more than 25 years, reshaping the rules...

Regional property markets are outperforming capital cities across Australia right now, with dwelling values rising 3.3% over the three months to...