Australian Property Market Update July 2026

Disclaimer: These are generated via AI – please note that you need to do your own due diligence and read the report yourself to make your own...

Australia’s 2026 Federal Budget has delivered the most significant tax reform for property investors in more than 25 years, reshaping the rules around negative gearing, capital gains tax (CGT) and discretionary trusts. For most existing investors, properties purchased before 7.30pm on budget night remain fully protected – but for anyone buying an established investment property from 1 July 2027 onwards, the old tax playbook no longer applies. Whether you hold one investment property or are building a portfolio, understanding these changes now is the difference between a strategy that still works and one that quietly erodes your returns.

Picture this: Rita, 45, has worked hard, nearly paid off her family home, and has been quietly researching her first investment property. Her plan was straightforward – buy an established property in a growth suburb, use negative gearing to reduce her tax bill while the property appreciated, and sell it in ten years with the benefit of the 50% CGT discount. It is a strategy that millions of Australians have used successfully for decades.

Then, on the evening of 12 May 2026, Treasurer Jim Chalmers announced what he called “the most significant tax reform package in more than a quarter of a century.”

The headline numbers tell the story of why. House prices have risen more than 400% since 1999 – more than twice the pace of wages growth. Since 2020, investors have grown their share of new home loans from under 30% to more than 40%, while owner-occupier rates have fallen. For younger Australians and first home buyers, the odds have been stacking against them for years.

The government’s position is that generous tax settings – particularly negative gearing and the 50% CGT discount – have distorted property demand and contributed to prices running ahead of incomes. The reforms aim to tilt the balance back, with Treasury estimating the changes will help an additional 75,000 Australians into home ownership over the next decade.

For investors like Rita, this complexity means it is time to understand exactly what has changed – and what has not.

Negative gearing allows investors to claim tax deductions when an investment property’s expenses (mortgage interest, rates, maintenance) exceed rental income. For decades it has allowed investors to reduce their taxable salary income by the amount of the property loss.

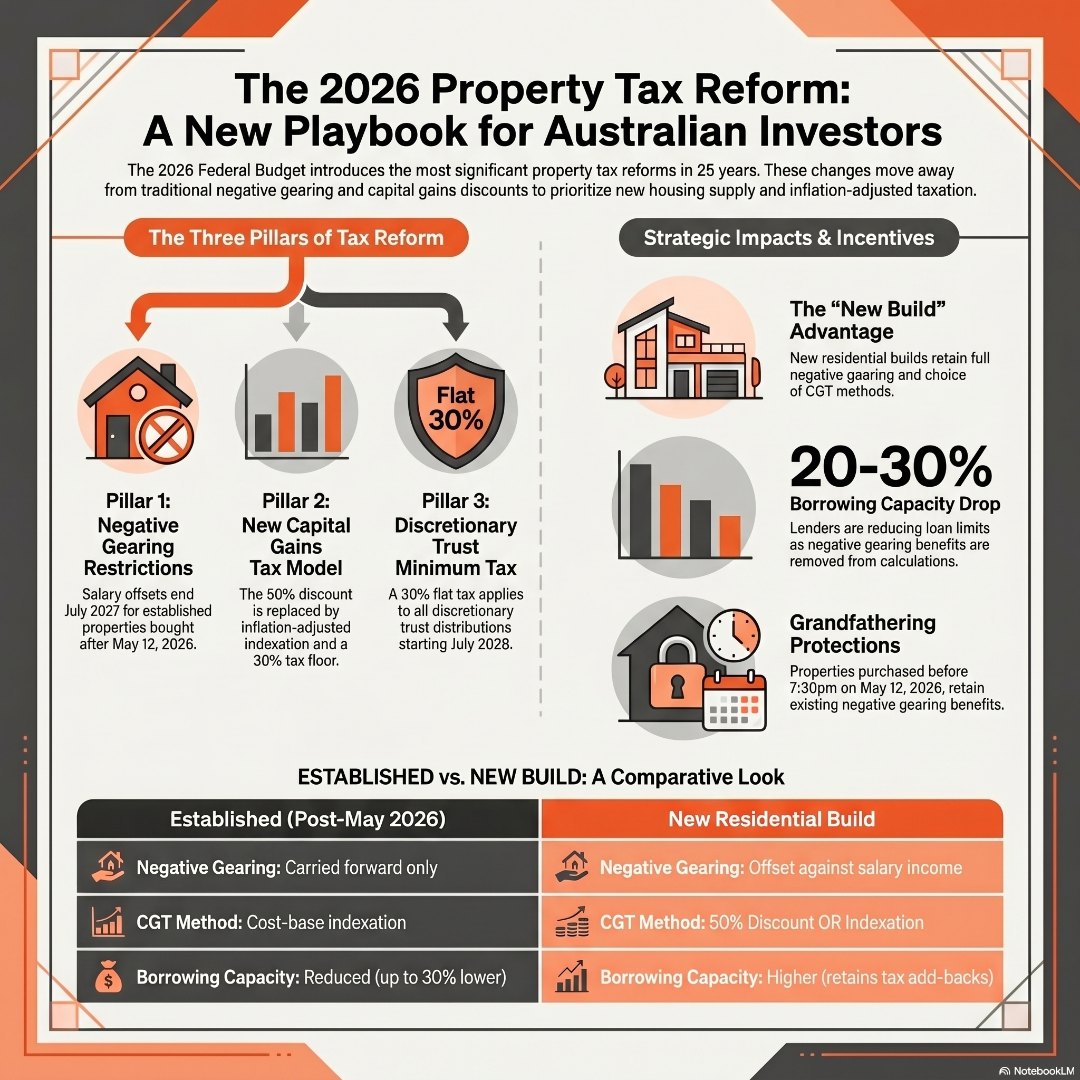

Under the new negative gearing changes 2026, this offset against salary income will no longer be available for established investment properties purchased after 7.30pm on 12 May 2026, starting from 1 July 2027. Those losses are not lost – they can be carried forward and offset against future income from the same property – but they cannot be immediately deducted against wages.

For an investor on a $120,000 salary running a $15,000 annual property loss, this is a meaningful change. Under the old rules, that loss reduces taxable income to $105,000. Under the new rules, that same loss must be deferred.

There are important carve-outs. Properties purchased before budget night are grandfathered – existing investors can continue to negatively gear those assets under current rules. New residential builds and certain government housing programs remain fully eligible for negative gearing against salary income regardless of purchase date. This is a deliberate incentive to keep new housing supply flowing.

Treasury projects that about half of negatively geared established properties are sold or start generating income within four to five years, and more than 75% turn over within ten years.

The second major change under this capital gains tax reform is the replacement of the 50% CGT discount with cost-base indexation for assets held more than 12 months, effective from 1 July 2027.

Here is the practical difference. Under the 50% discount model, if you buy an established property for $600,000 and sell it for $900,000, your taxable gain is $150,000 (50% of the $300,000 profit). Under cost-base indexation, the original purchase price is adjusted for inflation over the holding period – so if inflation increased by 20% over that time, your cost base rises to $720,000, and your taxable gain is $180,000.

In periods of moderate inflation, indexation typically produces a smaller discount than 50%. In periods of high inflation, it can produce a larger one – which is why the government has also introduced a 30% minimum tax on capital gains from 1 July 2027. This floor prevents investors from timing a property sale to coincide with a low-income year to minimise tax.

Importantly, these arrangements apply to gains realised after 1 July 2027 – even if the property was purchased before that date. Existing investors are not immune to the CGT changes when they eventually sell.

For new residential builds, investors retain the choice of either the 50% discount or cost-base indexation – giving maximum flexibility to choose whichever method produces the lower tax outcome. It is worth running the numbers with an accountant before choosing your structure.

[NOTE: The interaction between cost-base indexation and the 30% minimum tax floor for individual investors versus trusts should be confirmed with your tax adviser as ATO guidance is updated closer to 1 July 2027.]

Many property investors with multiple properties or higher-income households have historically held assets in discretionary trusts to distribute income among family members in lower tax brackets.

From 1 July 2028, a new 30% minimum tax on distributions from discretionary trusts will change that approach significantly. The tax applies to the trust’s income regardless of which beneficiary it is distributed to. Fixed trusts, superannuation funds, deceased estates, special disability trusts, charitable trusts, and farming income are excluded.

I have seen first-hand what happens when structure is treated as an afterthought. Years ago, when Money Magazine asked me to contribute to an article on positive and negative gearing, I shared something that has stayed with me ever since. A property investor I knew – a smart, hard-working person who had built a solid portfolio over decades – was approaching retirement and had held his properties inside a complicated trust and company structure. It had seemed clever at the time. But because the structure had never been properly reviewed as the rules evolved and his circumstances changed, he was staring down a capital gains tax bill he simply could not manoeuvre around. Worse, he could not access his equity efficiently to fund the retirement he had spent twenty years building towards. The properties were there. The wealth was there, on paper. But the structure had become a trap. That story came back to me the moment the 2026 budget changes were announced – because the new 30% minimum tax on discretionary trust distributions is exactly the kind of rule shift that punishes investors who set and forget their structure.

If you currently hold or plan to hold property in a discretionary family trust, a review is needed well before that 2028 date. Self-managed superannuation funds (SMSFs) remain outside the new regime and may represent an increasingly attractive structure for investors planning a long-term hold strategy, though SMSF property investment has its own rules that require specialist advice.

Beyond the tax mechanics, there is an immediate and practical consequence for anyone seeking finance to buy an investment property in 2026-27.

Lenders use rental income and negative gearing tax benefits as add-backs when calculating how much you can borrow. With negative gearing removed for established investment properties purchased after budget night, several lenders have already confirmed they will adjust serviceability calculations accordingly. Macquarie Bank announced changes to investment loan policy within weeks of the budget announcement, and other major lenders are expected to follow.

If you previously qualified to borrow $800,000 because your lender factored in the tax benefit of your rental loss against your salary, that calculation now changes. Early broker reports indicate some investors are seeing investment property borrowing capacity reductions of 20-30% for new established investment property purchases, depending on the lender and their income profile.

This is why understanding your investment loan strategy in a post-budget environment matters just as much as understanding the tax rules. Our guide to strategies to improve your borrowing capacity for property investment explains the specific moves investors can make before applying for finance.

If you are reviewing a property you already own, our article on negative gearing – time to re-evaluate your strategy is still highly relevant to whether carrying a loss makes sense for you today.

The window between now and 1 July 2027 is an important planning period – not a reason to panic. Here is a practical framework:

If you already own an established investment property: Your negative gearing is protected. Review what your after-tax position looks like when you eventually sell, given the CGT changes that will apply to gains made after 1 July 2027. Speak to your accountant about whether holding longer or restructuring your exit timeline makes sense.

If you are planning to buy an established investment property: Run a careful after-tax cash flow analysis under the new rules – specifically the loss-carry-forward model. Make sure the asset stacks up on its fundamentals, not on the assumption that the government will subsidise the loss. Consider whether a new residential build offers a better risk-adjusted outcome.

If you hold property in a discretionary trust: Consult a specialist tax adviser before 1 July 2028. Depending on your structure, there may be options to reconfigure distributions or transition to a different holding vehicle before the minimum tax applies.

If you are assessing your borrowing capacity: Get an updated assessment from a mortgage broker who understands the new lender policies. The numbers may look very different to what they did six months ago.

A well-built investment property portfolio strategy has always required adapting to changing conditions. The 2026 reforms are significant – but investors who understand the rules and adjust their approach accordingly will continue to build real wealth.

The 2026 Federal Budget has fundamentally changed the tax landscape for Australian property investors. Negative gearing for established investment properties purchased after budget night will end from 1 July 2027. The 50% CGT discount will be replaced by cost-base indexation with a 30% minimum tax floor. Discretionary trusts face a new 30% minimum tax from 1 July 2028. New residential builds retain the old tax advantages and represent a genuine strategic opportunity for investors willing to think ahead.

For investors who already own properties, the grandfathering provisions are protective – but they are not permanent shields when it comes to CGT on eventual sales. The right response is not to freeze, but to plan. Review your structure, reassess your borrowing position under the new lender criteria, and make sure every property in your portfolio is justifiable on its fundamentals – not just its tax breaks.

The rules have changed. Your strategy can too.

The Investors Choice Mortgages Hub is built exactly for this. Whether you are buying your first investment property, reassessing an existing portfolio, or reviewing how your loans are structured, the ICM Hub combines smart loan structuring tools, borrowing capacity calculators, and expert mortgage strategy guidance tailored to investors navigating real-world complexity. Explore the Investors Choice Mortgages Hub and get clear on what the new rules mean for your next move.

What are the negative gearing changes in Australia’s 2026 Federal Budget?

Investment properties purchased after 7.30pm on 12 May 2026 will no longer be able to offset losses against salary income from 1 July 2027. Losses must instead be carried forward and offset against future income from the same property. Properties bought before budget night retain full negative gearing under grandfathering provisions. New residential builds and some government housing programs are exempt from the change.

Is the 50% CGT discount being abolished in Australia?

The 50% CGT discount is being replaced by cost-base indexation for assets held more than 12 months, effective from 1 July 2027. Under indexation, only the inflation-adjusted portion of a gain is taxed – meaning the effective discount depends on inflation over the holding period. A 30% minimum tax on capital gains also applies from 1 July 2027 to prevent income-timing strategies. New residential builds may choose between the 50% discount or the new indexation model.

How do the 2026 budget tax changes affect my investment loan borrowing capacity?

Several lenders, including Macquarie Bank, have already removed negative gearing add-backs from serviceability calculations for new established investment property purchases. Early data suggests some investors are experiencing borrowing capacity reductions of 20-30% for post-budget established investment property loans. Consulting a mortgage broker for an updated assessment under current lender policies is strongly recommended before applying for finance.

Are properties in family trusts affected by the 2026 budget changes?

Discretionary trusts – including family trusts commonly used to hold investment properties – will face a new 30% minimum tax on distributions from 1 July 2028. Fixed trusts, superannuation funds, charitable trusts, and farming income are excluded. Investors currently using discretionary trust structures should review their arrangements with a specialist adviser well ahead of that date.

Disclaimer: These are generated via AI – please note that you need to do your own due diligence and read the report yourself to make your own...

Australia's property investors are facing a double headwind in 2026 - and the latest lending data confirms the retreat has already begun....