Why Are Regional Property Markets Outperforming Capital Cities in 2025?

Regional property markets are outperforming capital cities across Australia right now, with dwelling values rising 3.3% over the three months to...

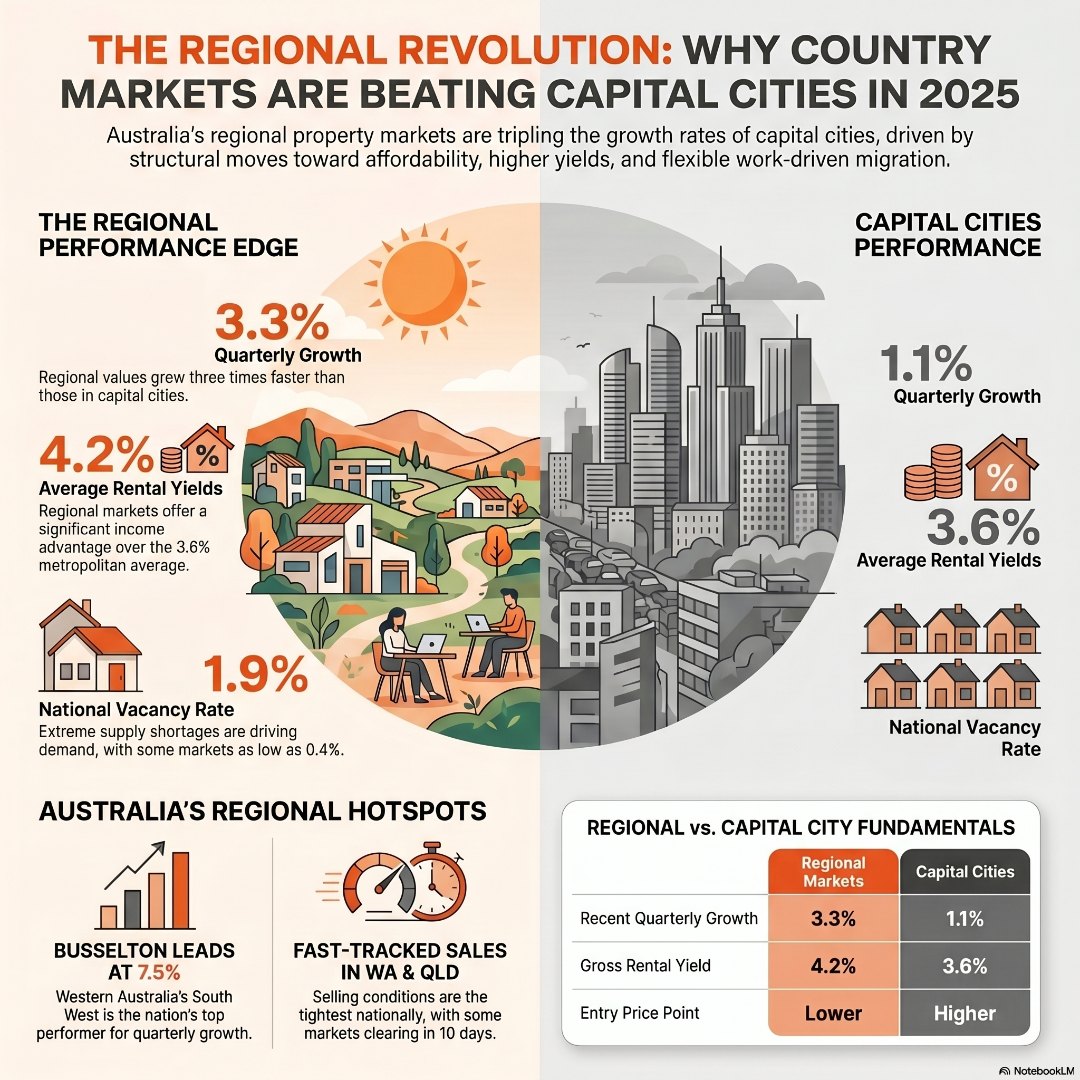

Regional property markets are outperforming capital cities across Australia right now, with dwelling values rising 3.3% over the three months to April compared with just 1.1% for the combined capitals. The gap is not a coincidence – it is being driven by a powerful combination of housing affordability pressures, accelerating internal migration, and tighter rental supply that is reshaping where buyers and investors are looking. Western Australia leads the charge nationally, but strong conditions are also evident across Queensland and Tasmania. Understanding which specific markets are moving, and why, is the difference between watching this opportunity pass or being positioned ahead of it.

If you have been following the property news and wondering whether the regional story is genuine or just media noise, the data is clear. Three in five of Australia’s 50 largest regional Significant Urban Areas recorded a slower pace of growth this quarter compared with the previous one. But here is the critical nuance: even with that easing, regional markets are outperforming the capitals by a significant margin.

The national market is losing momentum. Interest rates have weighed on borrowing appetite, and affordability fatigue has softened demand in the major cities. Yet regional Australia has absorbed those headwinds far better than Sydney, Melbourne, or Brisbane. Affordability remains the central reason. When buyers are priced out of capital city markets, or simply want more for their money, regional towns become a compelling alternative. That is not wishful thinking – it is movement confirmed by actual migration data and market clearance rates.

The sea change and tree change stories are not new. What has changed is the scale, the permanence, and the demographic profile of the people making those moves.

Flexible and remote working arrangements have given a growing number of Australian households genuine freedom over where they live. For many, that calculation now lands firmly outside the capital cities. Regional areas offer lower purchase prices, lower rents, and a pace of life that increasingly appeals to both young families and older Australians planning their next chapter.

Importantly, this internal migration Australia trend is translating into real demand pressure in specific markets. In Western Australia’s South West, the spillover effect from Perth is sending buyers into Busselton, Albany, Bunbury, and Geraldton. Busselton grew 7.5% for the quarter – despite having a median value that already sits above Greater Perth. This is not just an affordability story. It is a liveability story, and demand is tracking accordingly.

Queensland’s regional markets are experiencing a similar dynamic. Townsville, Maryborough, and Toowoomba are all recording strong conditions. Tasmania has also seen renewed momentum, driven by Burnie-Somerset and Launceston as buyers seek out lifestyle value and relative affordability.

For investors thinking about regional versus metropolitan property investment, this migration-driven demand creates a fundamentally different type of market driver – one that is structural rather than speculative.

The latest data paints a specific picture. Not all regional areas are equal, and the gap between top performers and laggards is wide.

Western Australia leads nationally:

Queensland performing strongly:

Tasmania showing renewed strength:

Areas showing weakness:

The contrast between WA’s south west and southern NSW is stark. Both are regional. Both are lifestyle markets. But the supply-demand dynamics are completely different, and that is what separates a sound investment from a poor one.

Capital growth is one side of the investment equation. The rental return is the other – and here too, regional markets have an edge.

Regional property rental yields across Australia sit at 4.2%, compared with 3.6% for the combined capital cities. That 0.6% difference may sound modest, but compounded over a multi-property portfolio and calculated against purchase prices that are often 30-50% lower than capital city equivalents, the actual dollar return is materially higher.

The vacancy story is equally compelling. The regional vacancy rate sits at just 1.9% nationally. In markets like Lismore, it has dropped to 0.4%. Geraldton and Albany are tracking around 1.0%. These are rental markets with almost no available stock. For investors who want to understand the importance of rental yield before committing capital, these numbers represent a genuine income advantage that capital cities are struggling to match.

Kalgoorlie-Boulder deserves a special mention. At 8.1% gross rental yield, it remains the highest-yielding major regional market in the country – a figure that reflects strong mining-driven rental demand against a purchase price base that has not yet caught up with that demand.

That 1.9% national vacancy figure is genuinely compelling – but I want to be honest with you, because I have made mistakes in regional markets myself and I would rather you learn from mine than repeat them. Years ago, I owned a property in Muswellbrook. On paper, the numbers stacked up. In reality, newer homes started hitting the rental market at the same price point, and tenants simply walked out of older stock to rent brand-new properties for identical weekly rent. My property sat vacant. The town’s economy was tied to one industry, and when conditions shifted, there was nowhere for demand to go. With hindsight, I probably would not have bought there. But that experience changed how I research regional markets permanently. Now I look hard at the demand driver before I look at the yield. Is it mining? Is it migration? Is it a regional hub with diverse employment, government services, and growing infrastructure? A vacancy rate of 0.4% in Lismore and 1.0% in Geraldton tells a very different story to a softening NSW coal town sitting at 4-5%. The number alone is not the answer. Understanding what is holding that number up – that is the work that separates a sound regional investment from a costly lesson.

| Factor | Regional | Capital City |

|---|---|---|

| Average gross rental yield | 4.2% | 3.6% |

| Recent quarterly growth | 3.3% | 1.1% |

| Average vacancy rate | 1.9% | Higher in most cities |

| Entry price point | Lower | Higher |

| Liquidity | Lower in smaller towns | Broader buyer pool |

| Lender restrictions | Some postcode limitations | Generally fewer |

Regional property investment Australia offers stronger cash flow and growth momentum right now. Capital cities offer greater liquidity and economic diversification. The right choice depends entirely on your personal borrowing position, cash flow needs, and risk tolerance.

A few questions worth working through before you act:

The current divergence between regional and capital city performance is real, data-backed, and being driven by structural forces – not a short-term spike. For investors with clear goals, sufficient borrowing capacity, and a data-driven approach to market selection, current conditions in select regional markets – particularly WA’s south west, coastal Queensland, and parts of Tasmania – represent a genuine opportunity. The combination of higher rental yields, tighter vacancy, and stronger capital growth compared with the major cities makes a compelling case. The critical qualifier is that regional investment rewards careful research over generalised optimism.

The Investors Choice Mortgages Hub is built for people who want that edge – real data, real brokers, and the kind of old-fashioned personalised service that actually picks up the phone when you call. Use the Suburb Snapshot tool to research specific regional markets, the Portfolio Profiler to map your next investment step, and speak with an expert who understands both the numbers and what they mean for your situation.

Regional markets are moving. The question is whether you have the right information to move with confidence.

Why are regional property markets outperforming capital cities in 2025?

Regional markets are outperforming because affordability is driving buyers away from expensive capital cities, internal migration is directing population growth into regional areas, and rental vacancy rates in top regional markets are exceptionally tight. Cotality data shows regional dwelling values rose 3.3% in the three months to April, compared with just 1.1% for the combined capitals – reflecting a clear and sustained divergence in market conditions.

Which regional areas have the highest property growth in Australia right now?

Western Australia’s south west is leading nationally. Busselton recorded 7.5% quarterly growth – the highest of any major regional area in the country – followed by Albany at 7.2%, Geraldton at 6.8%, and Bunbury at 5.8%. Regional WA as a whole grew 5.9% for the quarter. Strong conditions are also being recorded across Queensland (Townsville, Toowoomba) and Tasmania (Burnie-Somerset, Launceston).

Are rental yields better in regional areas or capital cities?

Regional areas currently offer higher gross rental yields on average, sitting at 4.2% compared with 3.6% across the combined capital cities. Kalgoorlie-Boulder leads all major regional markets at 8.1%. The regional vacancy rate of 1.9% nationally – and as low as 0.4% in Lismore – confirms that rental demand is strong and supply is constrained across many of the best-performing markets.

What are the risks of investing in regional property in Australia?

The main risks include significant variability between markets (not all regional areas are performing), lower liquidity in smaller towns, potential lender restrictions by postcode that can limit your LVR or loan options, and concentration risk if the local economy is tied to a single employer or industry. Conducting thorough due diligence on specific vacancy rates, infrastructure investment, population trends, and the local employment base is essential before committing.

Regional property markets are outperforming capital cities across Australia right now, with dwelling values rising 3.3% over the three months to...

Most commentary on Australian property prices zeroes in on one thing: interest rates. But reducing a complex, multi-trillion-dollar market to a...